- Date:

- Author:

- Martin Haycock

Client Portfolio Manager

A brief introduction to convertible bonds

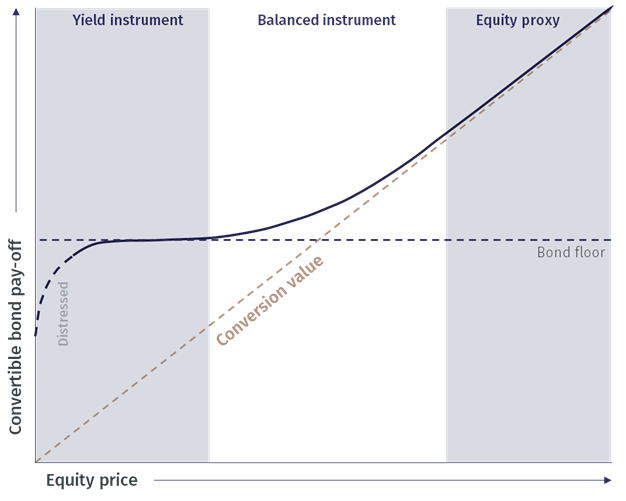

A convertible bond (“CB”) is a corporate bond with a valuable embedded option to convert the bond into a fixed number of shares of the underlying company, typically those of the issuer. This means investors can benefit not only from exposure to the upside potential of the underlying share price rising but also the potential downside protection offered by the bond component if the underlying share price were to fall.

What can convertible bonds offer to investors?

This makes convertible bonds a rather unique asset class for investors. They combine - in one instrument - features of both bonds and equities. Convertibles provide the same capital preservation potential and security of any other corporate bond, ranking alongside senior bonds in the capital structure. This means convertibles are subject to the same risk of default by the issuing company as with a straight bond. Convertible bonds typically pay a fixed coupon (the valuable conversion option meaning this is lower than on equivalent straight bonds) with total return coming primarily from the performance of the underlying stock price, meaning equity risk is an important element absent from a regular corporate bond.

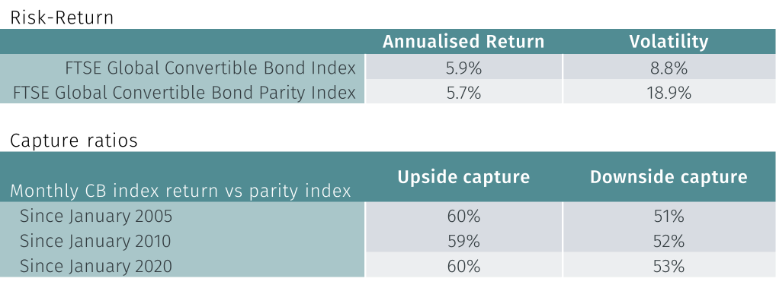

When the underlying stock prices rise, a convertible bond will capture a solid proportion of this upside. If the underlying stock price falls, the price of the convertible bond is still likely to fall, but the bond component means that drawdowns are typically lower than holding the stock directly. This combination is known as convexity; returns to the upside are typically greater than losses to the downside. This is confirmed through empirical observation: over the past 20 years convertibles have captured 60% of the monthly upside returns of their underlying shares, while participating in a much lower 51% in monthly downside returns.

Figure 1. Convertible bond payoff

Source: New Capital. For illustration purposes only.

How have convertibles performed in different market cycles?

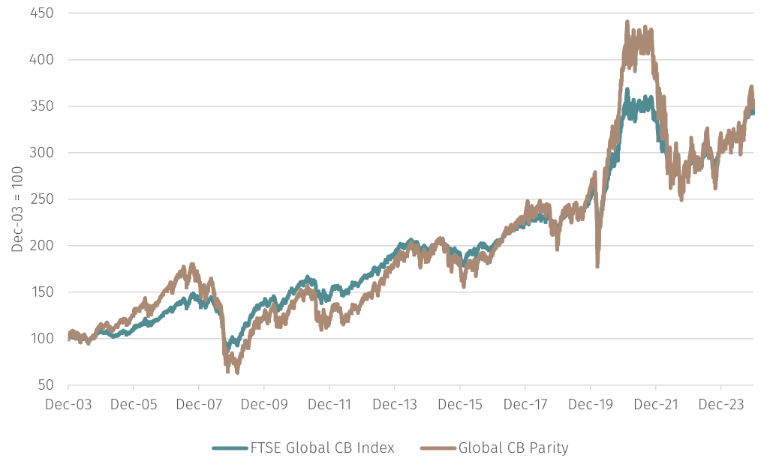

These asymmetric risk-return characteristics have held over numerous market cycles. Over the past 20 years, the FTSE Global Convertible Bond Index has delivered the same return as a portfolio of equities made up of the issuers of the index constituents. Furthermore, the volatility of these returns is less than half that of the equivalent equities, making for a smoother ride for investors, not least owing to much lower drawdowns in weaker markets. On a pure “apples-to-apples” basis, convertible bonds have exhibited superior risk-return characteristics than comparable equities, dampening equity volatility and reducing the impact of market cycles.

Figure 2. Convertible bond asset class performance*

Equity like performance with less than half the volatility, supporting risk-return optimisation in a portfolio over a 20+ year time period.

Past performance is not a guarantee of future performance. Returns may increase or decrease as a result of currency fluctuations.

*Sources: FTSE Convertible Indices, MSCI, Russell Investments. Chart and asymmetry capture data shown from end-2003 to 31-Dec-24. Index composition data as of 31 December 2024. Note: “Parity” convertible indices show the return of an equivalent equity portfolio made up of the underlying equities of convertible index members. This allows an ‘apples to apples’ comparison of convertible bond asset class performance.

Convertibles provide diversification

Not only are convertible bonds unique in terms of their risk-return characteristics, but they also offer exposure to a diverse universe of issuers. An active primary market makes for a dynamic global universe. Issuers span a range of sectors, often within secular growth themes, and feature companies of both investment grade and high yield credit qualities.

Convertible bond issuers are mostly of mid- to large equity capitalisation in size, while there is limited overlap in terms of names with either large cap (MSCI World) or mid-cap (Russell 2000) equity indices. This reflects the widespread use of convertibles as a financing tool for growth companies on their journey to become the leaders of tomorrow. Previous issuers of convertibles earlier in their growth trajectory include Nvidia, Tesla, Microsoft, Apple and Amazon.

Key takeaways/Summary

Convertible bonds offer a unique combination of both bonds and equities in a single instrument. They have been shown to exhibit convexity with historically greater upside equity market capture than downside. They have delivered returns in line with those of a comparable basket of equities, but with less than half the volatility. The fascinating asset class with its unique set of growth issuers is often overlooked and is worthy of closer inspection.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.