- Date:

- Read time:

- 5 mins

- Author:

- GianLuigi Mandruzzato

Senior Economist

On 12 December the Swiss National Bank (SNB) is widely expected to cut the policy rate again. The issues for markets are the size of the December rate cut and how low rates will go in 2025. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato argues the trough SNB policy rate will likely be higher than markets anticipate.

With the SNB largely anticipated to cut rates on 12 December, investors seem split between another standard 25 basis points (bps) move and an aggressive 50 bps reduction. According to our calculations, the futures contracts on short-term interest rates attach a probability of around 50% to a cut of 50 bps. Beyond December, markets anticipate the policy rate to be reduced to zero by September 2025 at the latest.

This scenario reflects that inflation declined faster than the SNB expected – annual inflation fell to 0.7% on average in October-November – and the anticipation that it will be close to zero or negative in the first half of 2025. Many commentators argue that the SNB should aggressively reduce the policy rate to keep it close to zero in real terms, i.e. adjusted for the current rate of inflation. This is the level that the central bank estimates as neutral.

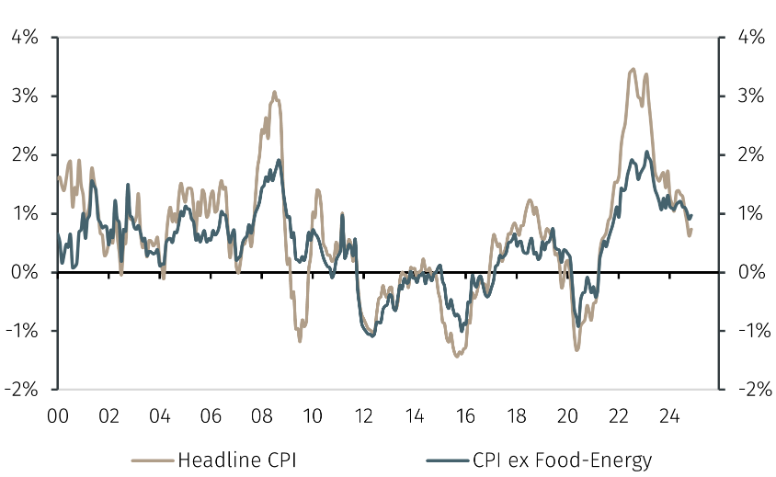

This conclusion overlooks other relevant factors the SNB considers when determining the appropriate level of the policy rate. First, the recent inflation decline was primarily due to energy and food prices, which are little influenced by monetary policy. According to our calculations, excluding food and energy prices, Swiss inflation has stabilised around 1% year-on-year (YoY), exactly in the middle of the SNB's target range (see Chart 1).

Chart 1. Swiss headline and core inflation

Food and energy prices, and the exit from the annual inflation calculation of the January 2024 increase in the VAT rate, are at the root of the expected decline in inflation in 2025H1. However, food and energy prices are historically volatile and if they were to rise again, the decline in inflation would be transitory.

If, to keep real rates close to zero, the SNB aggressively cut rates in December and early 2025 as markets anticipate, it could, for the same reason, be forced to raise them quickly in 2025H2. Policy rate volatility could be seen as the result of a policy error and undermine the central bank’s credibility.

Other elements add further support to a gradual approach to monetary policy easing by the SNB. Swiss gross domestic product (GDP) growth averaged 0.5% quarter-on-quarter over the last three quarters, above potential and the central bank’s expectations. For 2024Q4, the purchasing managers index (PMI) and KOF surveys point to solid growth supported by domestic demand and the services sector. The job market is healthy and, despite an increased unemployment rate, non-farm payrolls rose 1.2% YoY in 2024Q3. Furthermore, the SNB has been cutting rates since March and next year the economy will benefit fully from past monetary easing.

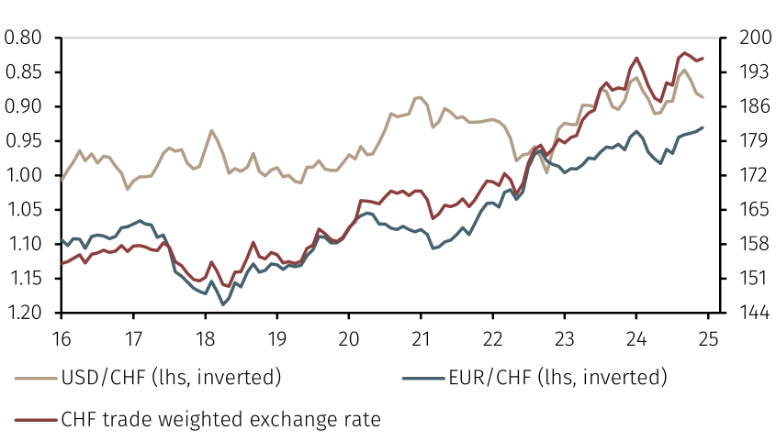

Finally, the risk of importing deflation due to a strong franc has decreased. Reflecting the franc’s decline against the US dollar, the trade-weighted exchange rate fell from late September, and its annual rate of appreciation slowed to 1% in December, the lowest since late 2021.

Chart 2. Swiss franc exchange rates

To conclude, a forward-looking approach to interest rate recalibration should advise the SNB to avoid responding in full to a decline in inflation that may prove transitory. While an aggressive interest rate cut at the December meeting cannot be ruled out entirely, we think the SNB will opt for another 25 bps move, reducing the policy rate to 0.75%.

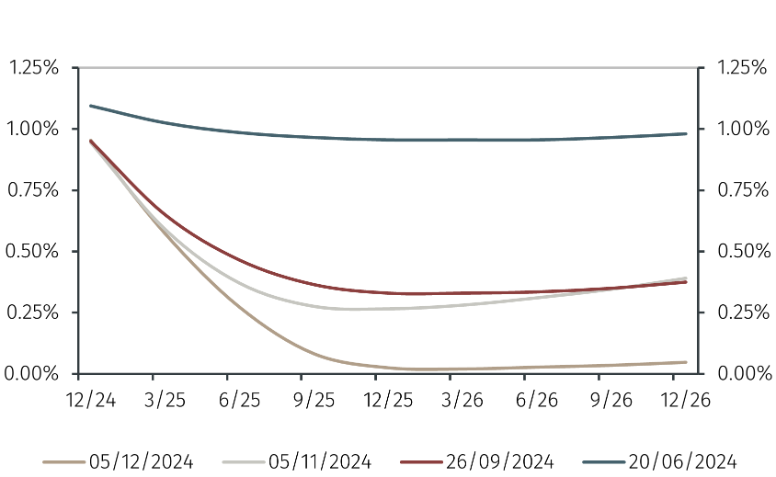

A gradual adjustment of monetary policy looks appropriate also considering that the other major central banks are reducing interest rates cautiously. In 2025, absent any negative shocks to the economy, the SNB policy rate will likely bottom at 0.50% in March and remain unchanged until 2026, a somewhat higher profile than currently priced into futures contracts on Swiss short-term interest rate (see Chart 3).

Chart 3. Swiss 3-month interbank rate implied in futures contracts

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.