- Date:

- Author:

- Sam Jochim

Economist

At its meeting on 24 January, the Bank of Japan (BoJ) Policy Board raised its policy interest rate by 25 basis points to 0.5%. In this Macro Flash Note, Economist Sam Jochim explains the reasons behind the decision and discusses the policy outlook for 2025.

At its December 2024 meeting, the BoJ left monetary policy unchanged, citing uncertainties regarding the outlook for wages, prices and overseas economies. The Bank’s decision to raise interest rates in January 2025 therefore reflected a greater degree of certainty regarding the outlook for these factors.

Regarding wages, Governor Ueda gave an interview in the week preceding the January Policy Board meeting in which he placed emphasis on the positive discussions held with the BoJ’s regional branch managers. A document published alongside the BoJ’s January decision noted that firms have “expressed the view that they will continue to raise wages steadily, following the solid wage increases last year”.1

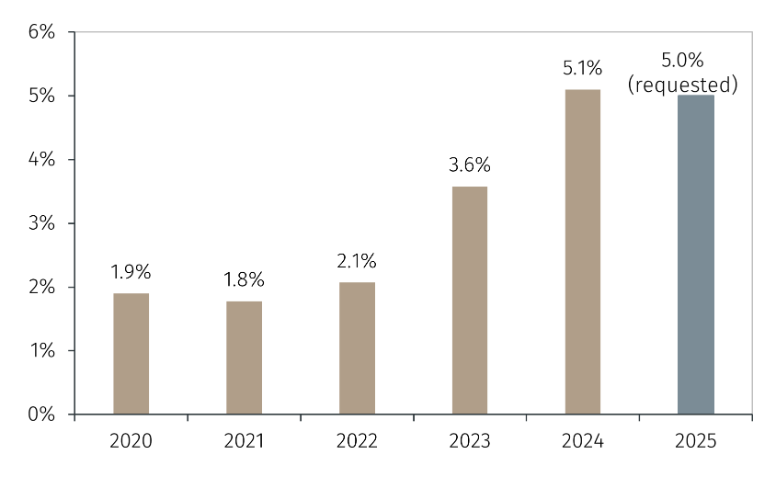

Last year saw the largest agreed wage increases in 33 years in Japan during the Shunto, a key factor in the BoJ exiting its negative interest rate policy in March.2 A similar outcome has been sought by labour union representatives this year and the BoJ has evidently gained confidence it will be achieved (see Chart 1).

Chart 1. Shunto results (wage increase, %)

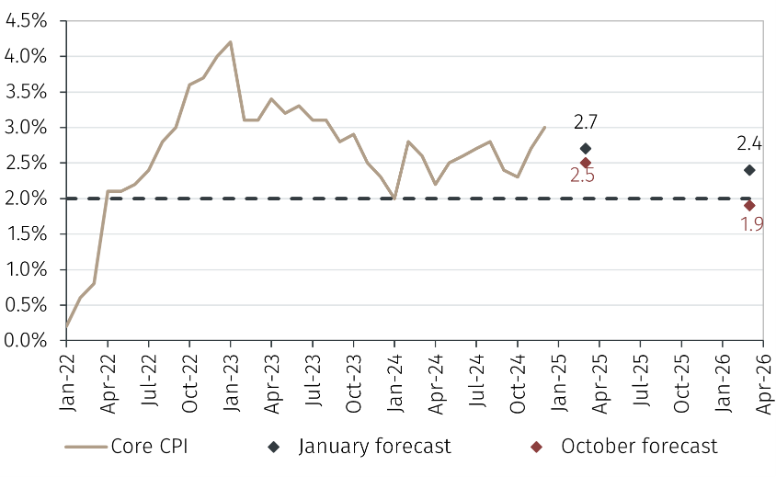

The BoJ has also become more confident in the inflation outlook in Japan. In its post-meeting decision document, the Bank stated that “with wages continuing to rise, underlying CPI inflation has been increasing gradually toward 2 percent”.3 The Policy Board expects inflation to average 2.7% in fiscal year (FY) 2024 before declining to 2.4% in FY 2025.4 Both forecasts are above those made in October 2024 (see Chart 2).

Chart 2. Japanese core consumer price index (CPI) inflation and BoJ forecasts (% change, year-on-year)

The remaining factor that the BoJ highlighted in its December 2024 meeting regarded policy abroad. The Bank emphasised significant uncertainty about US economic policies and how they could impact the global economy. In its view, the risks to prices stemming from this uncertainty are skewed to the upside for FY 2024 and 2025, helping explain why the Policy Board deemed it appropriate to raise interest rates in January.

In terms of the outlook for monetary policy in Japan in 2025, it is notable that January’s policy decision represented the first interest rate increase since July 2024, thereby maintaining a cautious approach to policymaking. The BoJ is reticent to shock financial markets after doing so in July and is therefore likely to give guidance on policy decisions ahead of meetings.

The BoJ has placed emphasis on the fact that real interest rates remain “significantly negative” and that financial conditions are therefore accommodative. If economic conditions materialise broadly in line with the BoJ’s expectations, it is reasonable to expect more policy rate increases in 2025.

BoJ staff have estimated a range for the neutral real policy rate of between -1% and 0.5%.5 Assuming inflation is 2% gives a nominal policy rate between 1% and 2.5%. While such a range is large, the lower bound provides a good guide as to where rates could reach this year. Markets expect one more 25 basis point rate hike in 2025 and while this is not an unrealistic scenario, there are risks that the BoJ is more hawkish than markets currently expect. In summary, the BoJ raised its policy rate at its January meeting due to greater certainty regarding the outlook for wages and prices and its assessment that risks to prices stemming from policy uncertainty abroad are skewed to the upside. While the pace of policy normalisation will remain gradual, further interest rate increases should be expected in 2025 and it is possible the BoJ has a more hawkish policy-bias than markets are currently expecting.

1 https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2025/k250124b.pdf

2 Shunto is a Japanese term which refers to the annual Spring wage negotiations between labour unions and many large employers in Japan.

3 The Bank of Japan has a mandate to achieve price stability and has set the price stability target at 2% in terms of the year-on-year change in the consumer price index.

4 https://www.boj.or.jp/en/mopo/outlook/gor2501a.pdf

5 https://www.boj.or.jp/en/research/wps_rev/wps_2024/data/wp24e12.pdf

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.