- Date:

- Read time:

- 3 mins

- Author:

- Sam Jochim

Economist

China’s annual National People’s Congress (NPC) always provides a good opportunity to gain insight into Beijing’s thinking on economic matters, including numeric goals for growth, inflation, and budget deficits. In this Macro Flash Note, Economist Sam Jochim assesses what can be expected from the Chinese economy this year following the latest NPC.

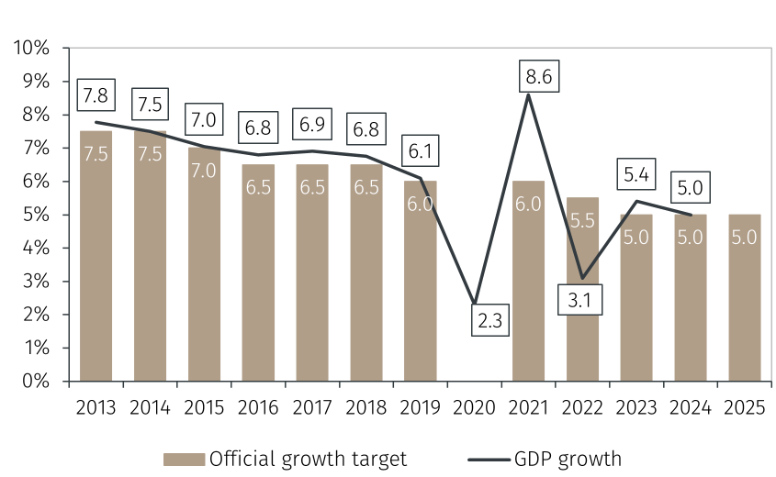

China’s National People’s Congress (NPC) convened on 05 March to deliberate on the 2025 government work report. The real GDP growth target for 2025 was set at “around 5%” (see Chart 1).1 This is the same target as for 2023 and 2024 but will be more difficult to achieve given the challenging external environment.

Chart 1. China’s GDP growth and official growth target (% change, year-on-year)

In 2024, China’s GDP grew 5%, in line with the government’s growth target. Net exports of goods and services accounted for around 30% of this, its largest share of GDP growth since 1997. Notably, this was driven by an increase in exports in Q4, particularly to the US.2 Purchasing Managers’ Index survey responses showed that, in part, the pickup in exports to the US reflected a frontloading of orders in anticipation of Trump’s tariffs.3

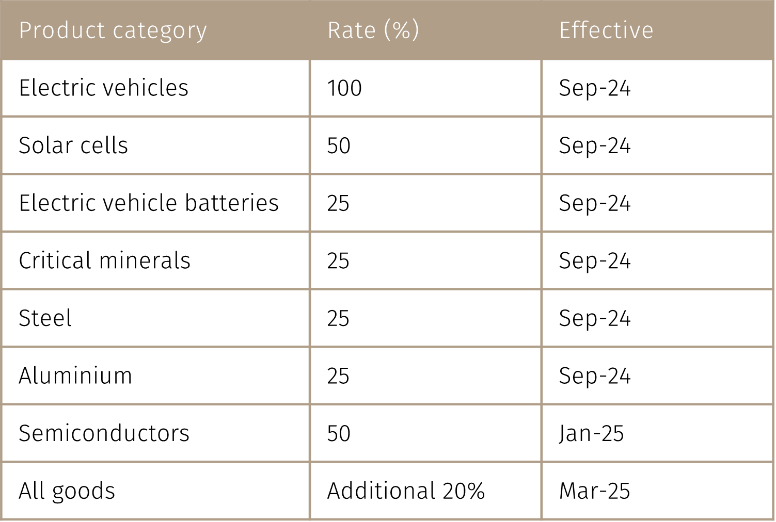

At the time of writing, Trump has placed an additional 20% tariff on Chinese goods exports to the US on top of those already in place (see Table 1). Beijing has responded with tariffs of its own on coal, liquified natural gas, and a range of agricultural machinery and goods.

Table 1. Summary of key US tariffs on Chinese exports

It is unclear what the overall impact of this will be and whether there will be further escalation. It is also possible that this is a precursor to Beijing and Washington negotiating to reduce trade restrictions. What is generally accepted though, is that US tariffs on Chinese goods, and vice versa, will be bad for Chinese GDP growth.

With the external environment acting as a headwind to growth in 2025, it is unsurprising that China has raised its fiscal stimulus targets for the year. The government work report announced a budget deficit target of 4% of GDP, up from 3% in 2024 and representing the highest level in around 30 years.

In addition, there will be RMB 1.3 trillion of ultra-long special treasury bonds issued in 2025, up from RMB 1 trillion in 2024.4 The local government special bond issuance target was raised from RMB 3.9 trillion in 2024 to RMB 4.4 trillion for this year. China’s government considers both to be off-budget debt and the government work report noted that the money raised will be used for construction investment, land acquisition, purchase of commodity housing stock, and settlement of overdue payments owed by local governments to enterprises.

The increase in special bond issuance amounts to around 0.5% of GDP and taken together with the 1% increase in the budget deficit implies additional fiscal stimulus for 2025 of around 1.5% of GDP. This is meaningful and it may not be coincidental that it roughly equates to the contribution of net exports to GDP growth in 2024.

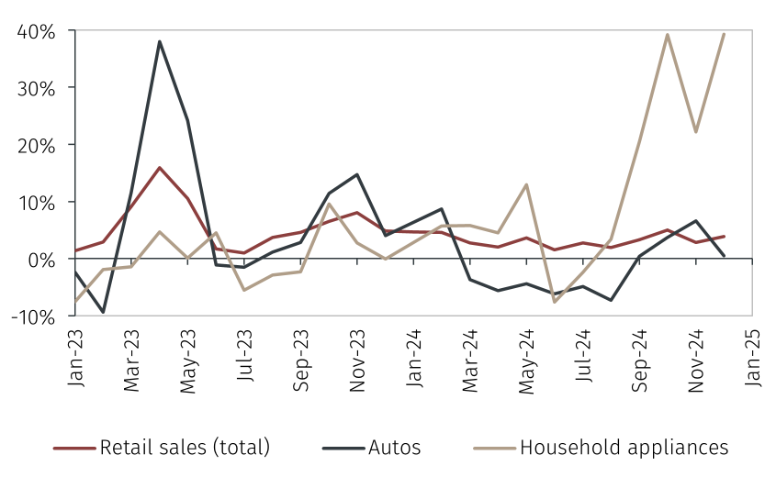

Given the more challenging external environment, it is a welcome development that stimulating domestic demand was listed as the top priority for 2025 in the government work report. The main policy aiming to achieve this will be an expansion of the goods trade-in scheme, which came into effect in September 2024. This scheme allows consumers to trade-in autos, durable goods, and technology such as smart phones in order to purchase new goods at subsidised prices. To-date, it has been successful in boosting demand for household appliances but less successful for autos (see Chart 2).

Chart 2. Chinese retail sales (% change, year-on-year)

However, the fact that RMB 300 billion of ultra-long special treasury bonds will be used to fund this scheme is somewhat underwhelming, given that RMB 150 billion was used for this purpose in the final four months of 2024. The government’s expenditure-per-month on the scheme will therefore decline in 2025 in the absence of any additional stimulus announcements.

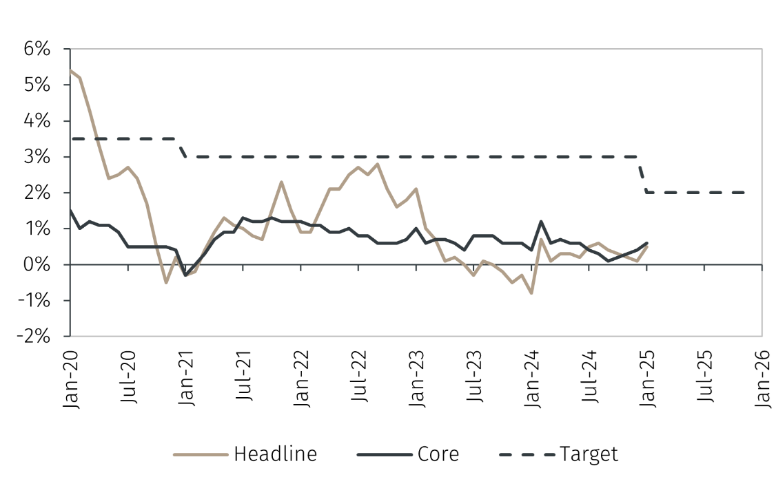

Monetary policy easing is likely to provide further support to the economy this year. The inflation target was lowered from 3% to 2% at the NPC, its lowest level in over twenty years. Rather than signalling that Beijing has a desire for lower inflation, this represents an acknowledgement that inflation has been below target since mid-2020 and the 3% target is unlikely to be attainable in the near-term and should therefore be moved lower to be more realistic. (See Chart 3).

Chart 3. China’s CPI inflation and inflation target (% change, year-on-year)

Broad-based monetary policy easing took place at the start of October 2024 to address structurally low inflation.5 However, the impact was modest and low inflation means that real borrowing rates in China remain relatively restrictive. Further monetary policy easing should therefore be expected in 2025.

In summary, China’s NPC outlined a steady increase in fiscal stimulus relative to 2024 to support domestic demand amid a more challenging external environment. The GDP growth target was left unchanged but will be harder to achieve. That Beijing places high importance on doing so means that if the economy is not on track to grow 5% this year, it is likely that further incremental stimulus may be announced, as was the case in 2024. The reduction in the inflation target represents an acknowledgement that 3% inflation for 2025 is unrealistic rather than a desire for lower inflation, and further monetary easing, albeit modest, is likely.

1 http://www.npc.gov.cn/jzzqw/jzzq/c34155/202503/W020250305326603076336.pdf

2 Chinese exports rose 10.0% year-on-year on average in Q4 2024, above the 4.6% year-on-year average in the first three quarters of the year. Exports to the US rose 10.6% year-on-year on average in Q4 2024, above the 1.8% year-on-year average in the first three quarters of the year.

3 https://www.pmi.spglobal.com/Public/Home/PressRelease/3516d9096c574bee9ded33a3cd219e28

4 Ultra-long special treasury bonds are bonds with tenors of 20, 30 or 50 years, issued by China’s central government “to consolidate growth momentum from a long-term perspective”. https://english.www.gov.cn/policies/policywatch/202405/21/content_WS664c1213c6d0868f4e8e74da.html

5 https://www.efginternational.com/uk/insights/2024/chinas_shifting_policy_stance.html

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.