- Date:

- Read time:

- 10 mins

- Author:

- Joaquin Thul

Argentina’s economy has been in the spotlight over the last year given the Milei administration’s success in controlling inflation, reducing the fiscal deficit, and attempting to deregulate the economy. In this edition of InFocus, Economist Joaquin Thul looks at the results of the first stage of the stabilisation plan and what to expect in 2025.

During his first year in office, Argentina’s President Javier Milei has seen a rise in popularity, due to his success in reducing headline inflation, cutting the fiscal deficit, and in taking important steps towards deregulating the economy.

Milei considers himself an anarcho-capitalist, a political philosophy associated with the Austrian school of liberal economists, which claims that many government institutions are unnecessary and can be replaced by private ones. Despite campaigning for a full dollarisation of the economy and closing the central bank, his efforts to stabilise the Argentinean economy have followed a more orthodox approach.

The first stage of the stabilisation plan was initiated in December 2023 and has four main pillars: (1) A monetary adjustment, (2) a fiscal adjustment, (3) rebuilding the central bank’s balance sheet, and (4) a tax amnesty for capital repatriation and investment promotion.

1. Monetary adjustment

The stabilisation plan involved a sharp devaluation of the official exchange rate by over 50%, the liberalisation of some controlled prices and raising the prices of public utilities, which increased by an annualised rate of 500% in the first three months of the Milei administration.

The surge in prices contributed to a reduction in liquidity, reflected in a contraction of the monetary base of 35% in real terms in the first four months of 2024. This amplified the deceleration in activity and lowered inflationary pressures.

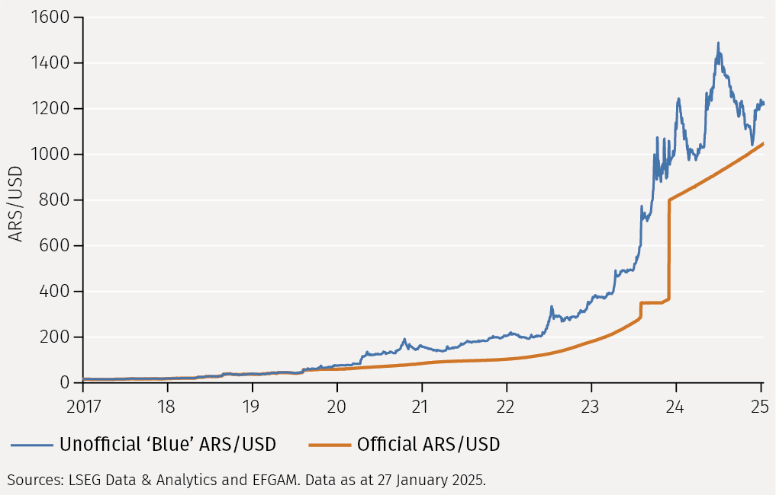

Rather than allowing the peso to float freely, a crawling peg of the peso to the US dollar was adopted, with a pre-announced devaluation of the exchange rate of 2% per month. As a result, the gap between the official and the parallel exchange rate, known as the “blue dollar”, has narrowed (see Figure 1).

2. Fiscal adjustment

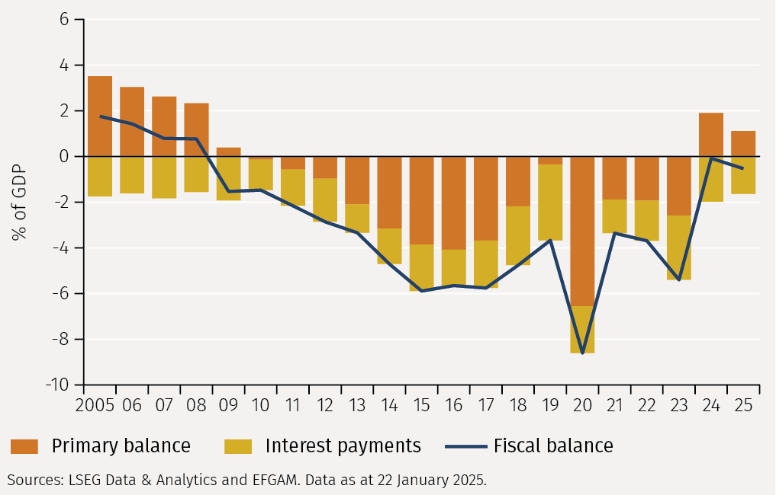

The combination of the currency devaluation, high inflation, and tighter fiscal policy led to a decline of over 30% in real primary spending in early 2024, diluting the value of the central bank’s (BCRA) nominal liabilities. The fiscal consolidation reduced primary spending by almost 5% of GDP (see Figure 2) through cuts to investment and transfers to the provinces, reducing public sector wages, eliminating subsidies, and slashing pensions. Instead of cutting expenditures, the fiscal consolidation should now focus on boosting revenues by growing the economy.

3. Restoration of the central bank’s balance sheet

A significant change was the end of monetary financing of the public sector’s deficit and the central bank’s quasi-fiscal deficit, which at the end of 2023 was approximately 6% of GDP.1 Through that channel, interest-bearing liabilities from the BCRA, known as LELIQ, were exchanged for Treasury notes, thereby financing government spending. This move reduced one automatic source of monetary expansion.

4. Tax amnesty and investment promotion

The government provided a tax amnesty for individuals and companies that wanted to regularise undeclared assets held both domestically and abroad, by paying a reduced tax rate. Bank deposits increased by approximately USD 18 billion in the first year because of this amnesty.

In July 2024 a new regime for promotion of large investments was introduced.2 This aims to provide legal stability for long-term investments in Argentina by offering tax, customs, and currency exchange incentives.3 It applies to investments of a minimum of USD 200 million in areas such as forestry, tourism, infrastructure, mining, technology, and energy. The scheme has a target of increasing foreign investment by USD 50 billion in the coming years. As of January 2025, eight investment proposals, primarily in the renewable energy, oil and gas and mining sectors, were submitted under this regime.

Recovery in activity

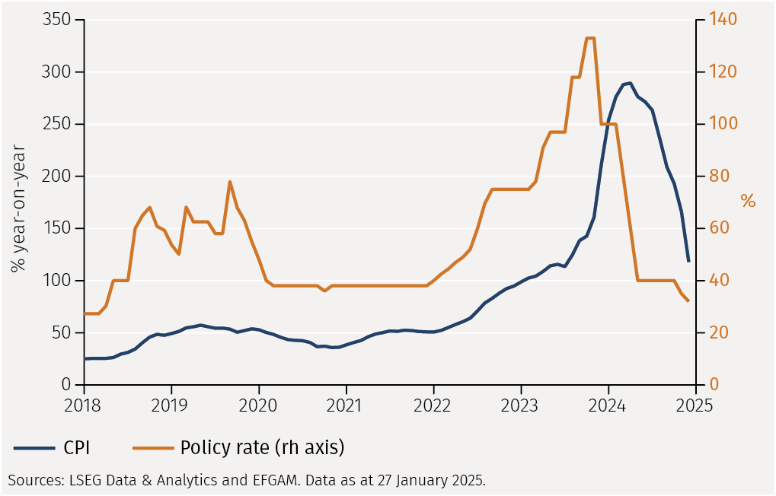

All these measures have helped to kickstart the economy, which was on the verge of a deep economic crisis. Inflation dropped from 25% month-on-month (MoM) in December 2023 to 2.9% MoM in December 2024, while annual inflation decelerated to just under 120% in 2024 after peaking at almost 290% in April (see Figure 3).

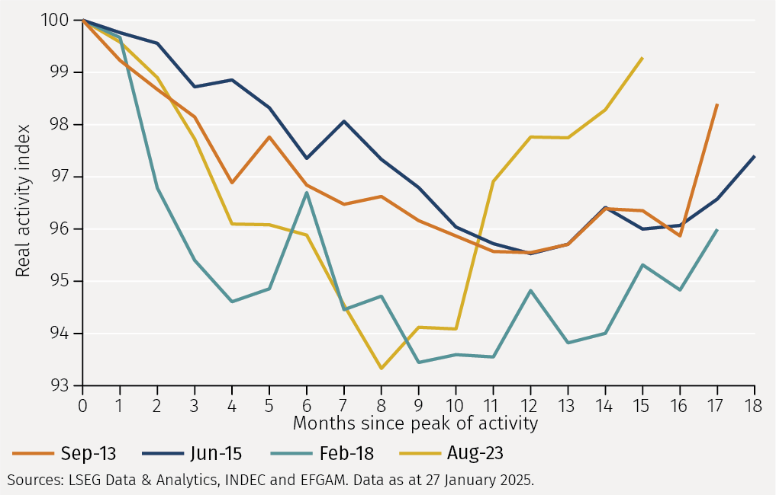

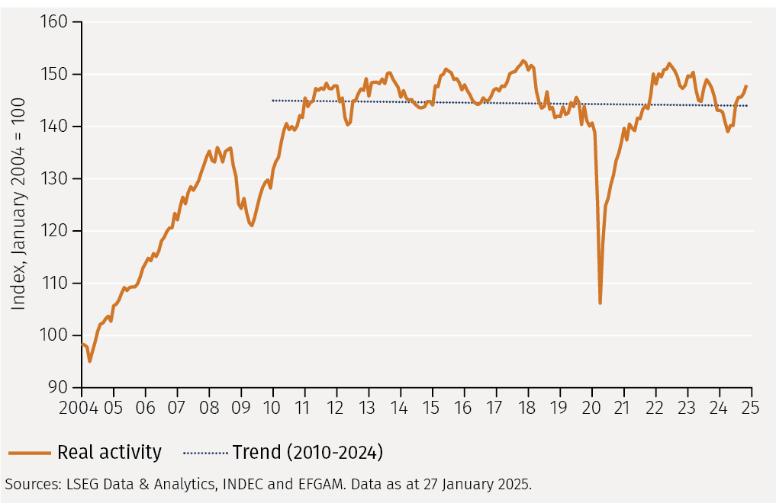

Furthermore, GDP growth had picked-up by the end of 2024. The monthly activity indicator rose 0.1% in November 2024 in comparison to the same period in 2023. The speed of the recovery from the recent recession has already outpaced previous recessions (see Figure 4).

The IMF expects real GDP contracted in 2024 by almost 3% and forecasts a bounce back in growth of close to 5% in 2025.4 However, the long-term trend of real activity seems to have stagnated, if not slightly declined, since 2010 (see Figure 5).

It is easy to understand the excitement around Milei’s successes. However, the first stage of the stabilisation plan came at a cost of an increase in the unemployment rate, which edged over 7%, and a decline in real incomes that led to a rise in poverty levels. Official estimates show poverty levels surpassed 50% of the population in the first half of 2024, before starting to decline in the second half of 2024.

What’s next for Milei?

Milei’s economic objectives for 2025 are likely to focus on (A) removing capital controls, (B) returning to international debt markets, and (C) gaining support in the midterm elections. Success in all these areas would be the most optimistic scenario for Argentina.

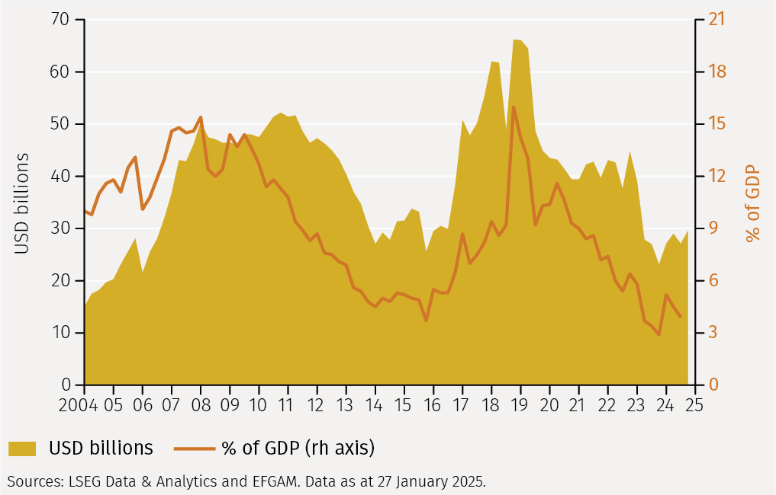

A. To lift capital controls and allow the peso to float the government needs to rebuild international reserves. Estimates show that Argentina should aim to grow the stock of gross international reserves to around USD 45-48 billion over the next three years, from USD 29 billion as at end 2024 (see Figure 6).5 Pre-announced devaluations can be problematic for commodity-exporting emerging economies during periods of strong US economic growth and a strong dollar, and when there is elevated geopolitical risk, which can disrupt commodity prices and create shocks to the terms of trade for commodity exporters. These conditions are clearly present in the current environment.

B. Argentina will need to roll over USD 14 billion in debt this year, one of the biggest headwinds for 2025. Their past debt renegotiations have not been easy, but Milei’s honeymoon with markets continues as investors sense a different tone from the government. Although Argentinean bond spreads over US Treasuries have narrowed from 2,500bps to 1,000bps, they remain high relative to other emerging economies. Investments in Argentina are still very risky and should be assessed appropriately.

C. Midterm elections scheduled for October 2025 represent the next hurdle for Milei. Dependent on the level of popular support, these will determine whether his government can continue to implement the proposed reforms. Even in the more optimistic scenarios, Milei will still need to form alliances to pass legislation.

Conclusion

Overall, Milei’s first year in charge has been a combination of a return to orthodox economic policies, some positive economic results, and question marks over the mediumterm impact of the tough austerity measures that have been implemented. Argentina’s improved relations with the IMF will be beneficial for the next stage of the stabilisation plan, although officials have reiterated the need to remove capital controls before discussing new funding. However, they have commended the Milei administration for the progress made at rebuilding the economy. Investors are right to highlight Milei’s recent success but should be aware of the challenges ahead to further reduce inflation to sustainable levels, remove capital controls and boost economic growth. For the time being, risks and uncertainty associated with investments in Argentina remain high.

1 Quasi-fiscal spending refers to operations that result in a net transfer of public resources to the private sector through nonbudget channels (Manual of Fiscal Transparency, IMF 2001).

2 https://tinyurl.com/2s3t24se

3 For example, the corporation tax will be capped at 25% for some of these investment projects, as opposed to the current maximum of 35%.

4 IMF World Economic Outlook Update, January 2025.

5 https://tinyurl.com/ycbwxnhm

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.