One of the themes in EFG’s Outlook 2025 is ‘BRICS grow in importance’.* The group is expanding, contributing more to GDP growth, and exercising a greater degree of co-operation. However, the potential for the BRICS to compete with the West is yet to be realised. In this edition of InFocus, Economist Sam Jochim discusses the BRICS importance for the global economy and the group's potential.

What is the BRICS?

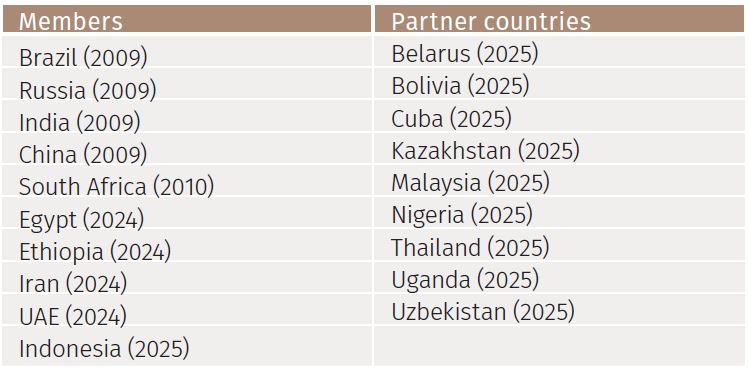

The BRICS bloc has expanded significantly since its inaugural summit in 2009, attended by founding members Brazil, Russia, India and China.2 In 2010, South Africa became the fifth member. The 2024 additions of Egypt, Ethiopia, Iran and the UAE saw the group expand to nine countries and in January 2025 Indonesia became the tenth BRICS member. The expanded group is sometimes referred to as the BRICS+.

There is no formal application process to join BRICS, but any country with ambitions to do so must receive the unanimous backing of all member states. For example, Pakistan’s application in 2023, and Venezuela’s in 2024, were blocked by India and Brazil, respectively.

The grouping is informal and has no founding treaty, no administrative office supporting it and no headquarters.3 Presidency rotates annually between the five initial BRICS members, though this process is under review since the bloc’s expansion in 2024. The BRICS presidency requires a country to set an agenda for the year and host a summit.

Russia’s presidency in 2024 culminated in a summit hosted in Kazan which saw BRICS members agree to create a new category of BRICS partner counties. Partner countries participate in BRICS summits but do not have voting rights or formal influence over the internal decisions and policies of BRICS. Nine countries became BRICS partners on 01 January 2025 (see Figure 1).

Figure 1. BRICS members and partner countries (joining year in brackets)

All BRICS members and partner countries agree to adhere to a set of guiding principles. The list of guiding principles is long, vague and often sees minor changes on a yearly basis depending on presidency but the main principles which appear consistently are listed below:4

• The BRICS spirit of mutual respect and understanding, equality, solidarity, openness and inclusiveness.

• The BRICS practice of full consultation and promoting concrete cooperation based on consensus.

• The BRICS vision of strengthening multilateralism, reforming the multilateral system and upholding international law.

Brazil took over the BRICS presidency for 2025 and set an agenda focusing on “Global South Cooperation”.5 While BRICS is an informal group with no official directive, a generally accepted objective highlighted by Brazil’s 2025 agenda is for the group to create an alternative to the Western-dominated system of global economic governance.6

Population and demographics

BRICS members currently account for around 48% of world population (see Figure 2). When BRICS was founded in 2009, its share of world population was around 42%. This growth reflects the addition of new members rather than population growth in the founding member countries. In ten years, if the membership is unchanged, the BRICS share of world population is projected to decline to 46% and by 2050 it is expected to fall to 44%.

Including partner countries, the BRICS bloc accounts for 54% of world population. This is expected to decline to 53% in 2035 and 50% in 2050. Interestingly, most of this decline represents the fact that China’s population is projected to fall by around 152 million persons—or 10.7%—over the next twenty-five years. If China is excluded from the analysis, BRICS members and partners currently account for around 37% of world population and this is not expected to change over the next 25 years.

In total, the BRICS population, including all member and partner countries, is expected to grow by 10% over the next twenty-five years. While this is below the 17.7% increase in world population expected over the same period, it is significantly above the 2.1% population growth projected for the G7 countries.7 Notably, African BRICS countries have the highest population growth rates over the next twenty-five years, with Uganda and Ethiopia both expected to see growth above 60% and Nigeria expected to see growth in excess of 50%.

When analysing demographics, it is also important to look at the age profile of a country’s population, as it is an important driver of economic growth. In this measure, the BRICS boasts a more attractive profile than the G7.

The median age of each BRICS country varies significantly. In 2025, the highest estimated median age belongs to Russia at 40.3 years and the lowest to Ethiopia at 19.1 years. This gives a range of 21.2 years. By 2050, this range is expected to widen to 27.5 years, with China overtaking Russia to have the highest median age at 52.1 years and Ethiopia’s median age rising slightly to 24.6 years.

Including partner countries brings down the age profile of the BRICS bloc, though not significantly (see Figure 3). The average median age in 2025 for BRICS members and partners is 30.8 years and by 2050 it is projected to rise to 37.0 years. Uganda and Nigeria have similar age profiles to Ethiopia, highlighting that one of the key contributions of the African BRICS countries is improving the demographic profile of the BRICS group.

The average median age in the G7 exceeds that of the BRICS, at 43.6 years in 2025 and 46.7 years in 2050. The strong demographic profile of BRICS relative to the G7 is one of the reasons we feel optimistic about the group’s future and the role it could play on the global economic stage.

GDP and GDP growth

The BRICS importance to the world economy is underlined by its share of world gross domestic product (GDP). In 2024, BRICS member countries are estimated to have accounted for 28% of world GDP.8 With the induction of Indonesia, that is expected to become 30% in 2025, a level which is projected to be maintained for the next five years according to IMF forecasts (see Figure 4).9 Including partner countries adds around 2% to the BRICS’ share of world GDP. The contribution of China is sizeable, with the world’s second largest economy accounting for around two-thirds of BRICS GDP.

While the BRICS outshines the G7 in terms of population and demographic profiles, the dynamic is reversed when looking at the level of GDP. However, this could soon change given the respective growth trajectories of the two groups. BRICS comprises emerging market economies, meaning its members tend to exhibit higher GDP growth rates than those of the G7 economies, which are developed economies.

From 2010 to 2023, the G7 and BRICS accounted for 32% and 42% of world GDP growth respectively. Furthermore, with the 2025 expansion of the BRICS, the group is forecast to account for 58% of GDP growth from 2024 to 2029, while the G7’s share of GDP growth is expected to decline to around 25%. Thus, while the G7 dwarfs the BRICS in terms of current GDP, the growth trajectory is one in which the overall size of the BRICS economy could soon overtake that of the G7. Indeed, if GDP is measured in purchasing power parity instead of 2015 USD then the level of BRICS GDP overtook that of the G7 in 2018.10

Trade dynamics

One of the themes of 2025 has been the rise in trade tensions. As highlighted in the EFG Outlook 2025, we believe that trade between the BRICS can take on an even more important role against this backdrop.

Looking at the current BRICS member countries’ trade in 2023 compared to 2013 is revealing. In 2013, around 15.0% of exports from BRICS member countries went to other BRICS members. There was a wide range within the data, with Iran and China’s

exports to BRICS members accounting for 56.2% and 10.3% respectively of their total exports (see Figure 5). Notably, only China exported more to the US than it did to the BRICS.

Figure 5. Exports as a share of total exports in 2013

In 2023, around 21.4% of BRICS members’ exports went to other BRICS members. The increase relative to 2013 in intra- BRICS trade was broad-based, with only India, Egypt and Iran exporting less to other BRICS members as a share of total exports (see Figure 6). The most significant increase was for Russia, which likely represents the impact of sanctions due to the war in Ukraine and the consequential decline in trade with the West.

Figure 6. Exports as a share of total exports in 2023

It is also notable that seven of the ten BRICS countries exported more to the US as a percentage of their total exports in 2023 than they did in 2013. While China now exports more to the BRICS bloc than it does to the US, India has moved in the other direction. With a great level of uncertainty surrounding US trade policy, there is a strong possibility that the BRICS seek more trade with each other to offset the impact of tariffs. This is highlighted by the fact that trade is one of the top priorities on Brazil’s BRICS agenda for 2025.

Trade matters more for some BRICS members than for others. The UAE, for example, exports goods and services amounting to more than 100% of its GDP (see Figure 7). While this is an outlier within the BRICS group due to the UAE economy’s reliance on oil exports, there are other economies such as South Africa which remain particularly sensitive to trade disruptions.

Beyond agreements at BRICS summits to bolster trade within the group, there are clear ways in which BRICS can offset disruptions stemming from increased trade tensions with the US. All BRICS members have higher average tariff rates than the G7 countries (see Figure 8). A reduction in trade barriers not only serves to boost trade but will also remove market inefficiencies and boost productivity.

But it is not just tariffs that impact trade. Quotas, hidden administrative restraints and controls on exchange rates and the movement of capital also matter. The ‘Economic Freedom of the World’ report from 2024 looks at freedom to trade internationally and assigns a score, with a higher score indicating more freedom to trade internationally.11

Here, the BRICS fare worse than the G7 (see Figure 9). This is also the case when looking at the overall economic freedom index which, in addition to freedom to trade internationally, considers size of government, legal system and property rights, sound money, and regulation. Once more, a higher score indicates a higher degree of economic freedom.

Thus, structural reforms which aim to improve freedom to trade internationally, and overall economic freedom, would mark positive steps towards supporting a greater degree of trade between the BRICS and limiting reliance on membership in an informal grouping. Nonetheless, the potential for intra- BRICS trade growth represents an exciting opportunity.

Conclusions

In conclusion, the BRICS bloc has expanded significantly since its inaugural summit in 2009 and now represents over 50% of the world’s population when including partner countries. The demographic profile is attractive relative to the G7 and is particularly boosted by the African BRICS members, highlighting that each member and partner country has something unique to bring to the table.

While BRICS’ GDP is lower than that of the G7, the growth trajectory is steeper, in part reflecting the fact that BRICS countries are emerging market economies which naturally tend to grow faster than developed economies due to their lower base.

Trade between BRICS countries has been on the rise over the last ten years but is still relatively low as a percentage of total trade. Brazil’s 2025 BRICS agenda focuses on “Global South Cooperation” and trade forms a key part of this. The potential for intra-BRICS trade to continue to grow and act as a buffer against elevated trade tensions with the West is particularly of note and could be boosted by structural reforms aiming to improve freedom to trade internationally and overall economic freedom.

Taken together, these factors provide a deeper insight into why we think the BRICS group will gain increased global significance in the years to come, as highlighted in EFG’s Outlook 2025.

*https://www.efginternational.com/uk/insights/2024/2025_outlook.html

2 The term BRIC was initially used by British economist Jim O’Neill in 2001 in a Goldman Sachs report discussing how the weight of Brazil, Russia, India and China in world GDP would grow over the next ten years.

3 https://commonslibrary.parliament.uk/research-briefings/cbp-10136/

4 https://tinyurl.com/2rva5rjc

5 https://tinyurl.com/mnucvbk

6 https://tinyurl.com/4hyhxdje

7 The G7 consists of Canada, France, Germany, Italy, Japan, the UK and the US.

8 Based on GDP in 2015 USD.

9 The IMF does not provide estimates for GDP growth for Cuba and so we assume Cuba’s GDP grows by its median growth rate from 2010 to 2023 of 1.8%.

10 https://tinyurl.com/3kt74a5b

11 https://tinyurl.com/2e6t5z6h

** The freedom to trade internationally and economic freedom indices take a score between 0 and 10, with 10 indicating better conditions and 0 indicating worse conditions.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.