- Date:

- Read time:

- 2 mins

- Author:

- Joaquin Thul

Economist

President Trump announced tariffs of 50% on US imports from Brazil. The imposition of these tariffs is not related to trade, immigration, drugs or an economic threat to the US. The additional duties are to help Brazil’s former President, and Trump’s close friend, Jair Bolsonaro. In this Macro Flash Note, Economist Joaquin Thul discusses why these tariffs are unlikely to cause a major concern for Brazil for the time being.

On 01 August 2025, the US imposed an additional 40% tariff on top of the 10% announced on Liberation Day on products imported from Brazil. This brought the stated tariff on US imports from Brazil to 50%, the highest among all US trading partners, see Chart 1.

However, the tariffs on Brazilian goods are not related to trade imbalances, immigration issues, drug trafficking or aimed at tackling an economic threat to the US. The US had a small trade surplus, close to USD 3 billion as of 2023, with Brazil. Brazilian migrants are unlikely to represent a large share of US illegal workers, nor are they responsible for traffic of fentanyl across the US borders. In this case, according to the Executive Order issued by President Trump, the additional tariffs are a reaction to:

1. actions from the Brazilian Government and the Supreme Court of Justice to regulate US social media platform accounts and censor content from accounts which was deemed illegal by Brazilian authorities.

2. actions from Brazilian authorities to persecute former President Jair Bolsonaro, a close friend of Donald Trump. The former Brazilian President is facing trial over an alleged coup attempt after losing the 2022 Presidential election.

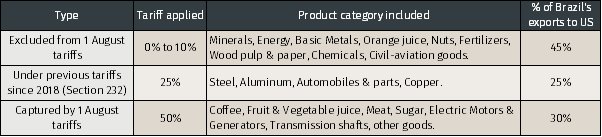

Although the tariff rate seems elevated, the Executive Order issued on 30 July includes a comprehensive list of over 690 products which are excluded from these tariffs and will continue to face either zero or the 10% baseline duty announced on 2 April. These represent close to 45% of total Brazilian exports to the US and include minerals, energy products, basic metals, orange juice, nuts, fertilizers, wood pulp and paper, some chemicals and civil-aviation goods.

Other goods such as steel, aluminum, automobile and parts, and copper will continue to face the 25% duty or respective quotas under Section 232 of the US Trade Expansion Act, since 2018.

Thus, the new tariffs will affect only about one third of Brazil’s exports to the US, including coffee, meat and sugar, among others.

Table 1: List of Brazil exports to the US affected by tariffs

Brazil’s top five exports to the US, which include crude petroleum, iron and steel, aircrafts and parts and wood pulp and paper, represent around 50% of its goods trade with the US. These products are exempt from the latest tariff update and that was seen positively by investors and the corporate sector in Brazil.

Brazilian markets fell 8% following the announcement of 10% tariffs on 02 April, with the Brazilian real losing close to 6% against the US dollar, see Chart 2. Following Trump’s letter to President Lula Da Silva on 09 July, announcing the 40% additional tariffs seeking justice for his friend Bolsonaro, equities sold off by 5%, while the real depreciated by 3% against the dollar.

However, Brazilian markets recovered after the scope of the new tariffs was clarified. Brazilian equities rose by 2% and the real appreciated against the dollar by about 2%. This signals that investors do not expect a large negative impact on the Brazilian economy from the increased import duties or that a political agreement solution could be reached to moderate them significantly.

Nevertheless, the additional tariffs could potentially become a headwind to economic growth if they were extended to other products. Although these are not trade related, their apparently subjective nature means it is unclear what would help convince President Trump to reduce them. Brazilian authorities have announced they will not allow foreign governments to interfere in their judicial system.

Minutes from the last meeting of Monetary Policy Committee of the Brazilian Central Bank (BCB) reflect it believes tariffs will have “significant sectoral impacts”.3 However, the aggregate effects on economic growth will depend on the negotiations outcome. For the time being, the BCB decided to leave the Selic rate unchanged at 15% as inflation remains elevated.

To conclude, the recent announcement of a 50% tariff on US imports from Brazil represent an important change in trade policy between the two countries. However, they will only affect a third of Brazilian exports to the US and their impact is expected to be muted. Although the nature of these tariffs is merely political, which raises the prospects of a negotiated solution, the possibility of this issue becoming an ideological problem that drags over time cannot be ruled out either.

Overall, tariffs will hurt Brazilian GDP growth in the medium term, if only moderately, unless an agreement is reached, or Brazil increases trade with other countries. This was the case following US tariffs on steel and aluminum during the first Trump Administration. Back then, Brazil increased trade with other partners, including China, to offset the reduced demand from the US. A similar path could follow this time too.

1https://www.whitehouse.gov/presidential-actions/2025/07/addressing-threats-to-the-us/

2The move from the Brazilian authorities aiming to regulate the use of social media and the spread of illegal content through various platforms has been positively received by international organisations such as Reporters Without Borders. https://rsf.org/en/brazil-supreme-court-increases-social-media-platforms-responsibility-welcome-decision

3https://www.bcb.gov.br/en/publications/copomminutes

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.