- Date:

- Read time:

- 2 mins

- Author:

- Haya Kamal

Macro Team

The International Monetary Fund (IMF) released its July World Economic Outlook (WEO) update and has edged global growth forecasts higher from the April 2025 WEO. In this Macro Flash Note, Haya Kamal summarises the latest report.

IMF growth forecasts

The IMF forecasts global real GDP growth of 3.0% and 3.1% respectively for 2025 and 2026.1 This reflects lower effective US tariff rates compared to what was announced in April; strong front-loading of imports and business investment in anticipation of tariffs; an overall improvement in financial conditions due to a weaker US dollar; and fiscal expansion in some jurisdictions.

As highlighted in the April 2025 WEO, uncertainty remains high. This is despite the US effective tariff rate coming down by over 7 percentage points. Nonetheless, tariff levels remain elevated, and the IMF assumes this to be the case through the remainder of 2025 and all of 2026.

Overall, global financial conditions have eased. Most US equity markets have rebounded in the second quarter and erased the 02 April tariff fallout losses. Other global equity markets have rallied, mainly due to the releases of economic data that were frequently providing positive surprises. Notably, the US dollar has depreciated by around 11% against other major currencies through the first half of 2025.2

For advanced economies, implied policy rate paths have flattened. In emerging market (EM) economies, the weaker US dollar has created space for monetary policy easing.

Global growth

In the first quarter, global growth was 0.3 percentage points above the IMF’s April WEO projections. This is largely due to a boost in private investment and international trade.

In the US, real GDP declined by an annualised rate of 0.5% quarter-on-quarter (QoQ) in the first quarter; its first quarterly contraction in three years. Meanwhile in the euro area, GDP accelerated to an annualised rate of 2.5% QoQ, largely due to net exports and investment. China reported strong GDP growth in the first quarter, which exceeded expectations at an annualised rate of 6.0%. This strong growth was mainly attributable to exports.

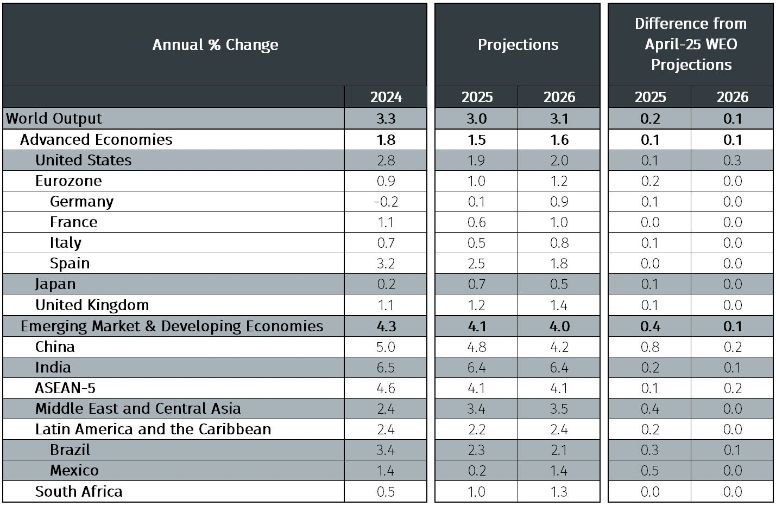

Table 1. IMF's WEO real GDP growth projections (% change, year-on-year)

Looking ahead, the IMF expects global growth to slow. Despite the upward revisions to global growth projections in relation to April, the forecasts for 2025 and 2026 remain below the 3.3% achieved in 2024 and the pre-pandemic historical average of 3.7%.

In advanced economies, growth is forecast at 1.5% in 2025 and 1.6% in 2026. In the euro area, growth was revised upward to 1.0% in 2025 and 1.2% in 2026. Although it represents less than 5% of total euro area GDP, this revision was driven by Ireland’s strong GDP outturn in the first quarter. The IMF increased its 2025 growth forecast for EM economies from 3.7% to 4.1%. This is mostly due to China, which saw the largest upward revision in the July WEO update, increasing by 0.8 percentage points to 4.8% in 2025.

Moreover, the IMF’s projection for world trade volume has been revised upward by 0.9 percentage points for 2025, but 0.6 percentage points downward for 2026. This further reflects front-loading impacts that are expected to slow down in the medium term.

Risks to the outlook

The IMF views risks to the outlook as tilted downwards, as was the case in the April WEO. Tariffs, front-loading, escalation of geopolitical tensions and fiscal vulnerabilities are highlighted.

The WEO highlights that a rebound in effective tariff rates could lead to weaker global growth. A situation where negotiations breakdown and tariff rates are much higher than they are today could result in an escalation of protectionist measures. Correspondingly, increased levels of uncertainty could weigh more heavily on economic activity, especially if deadlines for additional tariffs expire without substantial or permanent agreements.

The IMF also views the potential inflationary impact of additional tariffs or other non-tariff measures as a downside risk to growth. Here, non-tariff measures targeting critical inputs could lead to dislocations in global supply chains. To defuse trade tensions, the IMF notes that bilateral trade negotiations should address the root cause of trade imbalances that motivated the introduction of tariffs in the first place.

Front-loading has supported economic activity throughout the first half of 2025. However, the IMF points out that this raises the potential for negative shocks to be amplified. For example, firms may face increased holding costs and potential losses from obsolescence.

Furthermore, the IMF notes that if geopolitical tensions escalate, particularly in the Middle East or Ukraine, this will introduce further supply shocks and would likely disrupt global supply chains, pushing commodity prices up. This could also create complex trade-offs for central banks, in an environment where trade is already serving as an underlying challenge.

Lastly, as part of its revised WEO, the IMF highlights risks related to fiscal vulnerabilities in both EM and advanced economies. Several countries, including France and the US, are projected to run large fiscal deficits. This could result in higher term premiums and, in some cases, tighten global financial conditions, leading to lower growth.

On the upside, positive trade negotiations tied with predictable frameworks and tariff declines could support global growth in the view of the IMF. If agreements as such are reached, uncertainty would significantly reduce and foster policy predictability, facilitating investment and other business decisions.

Conclusion

To conclude, the importance of restoring confidence, predictability and sustainability remains a key priority according to the IMF. Pierre-Olivier Gourinchas, Chief Economist at the IMF, noted that “the world economy is still hurting and it’s going to continue hurting with tariffs at that level, even though it’s not as bad as it could have been”.3 Even with slight upward revisions to growth projections, the IMF makes clear that downside risks continue to dominate the outlook.

1https://www.imf.org/en/Publications/WEO/Issues/2025/07/29/world-economic-outlook-update-july-2025

3https://www.imf.org/en/Publications/WEO/Issues/2025/07/29/world-economic-outlook-update-july-2025

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.