- Date:

- Read time:

- 2 mins

- Author:

- Investment Solutions

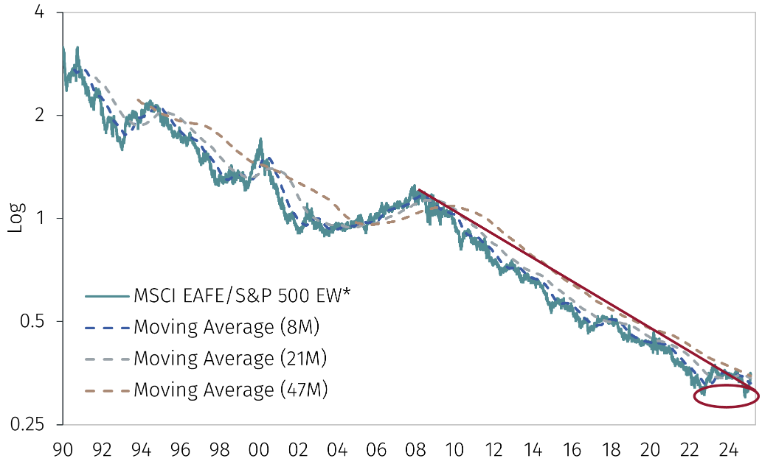

Relative to US equities, global equities have been in a downward trend since 2008

Investment Solutions

Relative to US equities (shown here by the S&P 500 Equal Weight Index), global equities (shown here by the MSCI EAFE Index) have been in a downward trend since 2008. In March 2025, however, that trend broke. This provides good support from a technical perspective for a positive view on global equities relative to US equities.

MSCI EAFE Index’s relative strength vs. the S&P 500 Equal Weight Index

*MSCI EAFE/S&P 500 EW line represents the MSCI Europe Australasia and Far East index divided by the S&P 500 equal weights index. Past performance is not an indication of future returns Source: FactSet and EFGAM calculations. Data as at 12 March 2025.

The breakout we are currently witnessing could have important implications for investors. Survey data from Bank of America shows investors hold a greater overweight allocation to US equities than to other regions.

In addition, global equity valuations relative to their own history appear more attractive than in the US. While valuations taken in solitude do not provide a meaningful signal, the fact that analysts are revising down earnings expectations for US equities and revising up earnings expectations outside the US for 2025 and 2026 make us optimistic about the prospects for a change in leadership.

To summarise, the breakout of the MSCI EAFE Index/S&P 500 Equal Weight Index from its 17-year downward trend, provides a strong argument from a technical perspective to favour global equities over US equities. The additional evidence gleaned from positioning, valuations and earnings fundamentals data give us even greater conviction on this call.

MARKETING COMMUNICATION For professional clients, qualified investors and accredited investors only. The value of investments and the income derived from them can fall as well as rise, your capital is at risk. Note: Past performance is not a guide to the future. Returns may increase or decrease as a result of currency fluctuations.

Performance contribution is gross of fees, all other performance shown is net of fees and expenses. Please refer to the Prospectus for further information on this Fund and prior to any subscription. All data sourced New Capital, EFGAM, Bloomberg, as at title date, unless otherwise stated.

Issued in the UK by EFG Asset Management (UK) Limited which is authorised and regulated by the Financial Conduct Authority (FCA Registration No. 536771). Registered No: 7389736. Registered address: Park House, 116 Park Street, London W1K 6AP. Telephone: +44 (0)20 7491 9111. This document is a marketing communication and does not constitute an offer to sell, solicit or buy any investment product or service, and is not intended to be a final representation of the terms and conditions of any product or service. The investments mentioned in this document may not be suitable for all recipients and you should seek professional advice if you are in doubt. Clients should obtain legal/taxation advice suitable to their particular circumstances.

This document may not be reproduced or disclosed (in whole or in part) to any other person without our prior written permission. Although information in this document has been obtained from sources believed to be reliable, EFGAM does not represent or warrant its accuracy, and such information may be incomplete or condensed. All estimates and opinions in this document constitute our judgment as of the date of the document and may be subject to change without notice.

EFGAM will not be responsible for the consequences of reliance upon any opinion or statement contained herein, and expressly disclaims any liability, including incidental or consequential damages, arising from any errors or omissions. Performance results shown are net of applicable fees and expenses.

Any information quoted relating to the New Capital UCITS Fund plc is merely a brief summary of key aspects of the Fund. More complete information on the fund can be found in the prospectus, the simplified prospectus or key investor information document, and the most recent audited annual report and the most recent semi-annual report.

These documents constitute the sole binding basis for the purchase of fund units. Copies of these documents are available free of charge in the United Kingdom at EFG Asset Management (UK) Limited ("EFGAM"), Park House, 116 Park Street, London W1 K 6AP, United Kingdom. Copies of these documents are available free of charge in Germany at the offices of the German information agent, HSBC Trinka us & Burkhardt AG, Konigsallee 21/23, 40212 Dusseldorf, Germany. Copies of these documents are available free of charge in France from the French centralizing agent, Societe Generale, 29, boulevard Haussmann - 75009 Paris, France.

Copies of these documents are available free of charge from the Swiss Representative: CACEIS (Switzerland) SA, Route de Signy 35, CH-1260 Nyon, Switzerland. Paying Agent: EFG Bank SA. 24 Quai du Seujet, CH-1211, Geneva 2, Switzerland. Copies of these documents are available free of charge in Luxembourg at the offices of the Luxembourg paying agent, HSBC Securities Services (Luxembourg) S.A., 16 boulevard d'Avranches, L-1160 Luxembourg, R.C.S. Luxembourg, B28531. Copies of these documents are available in the local languages as per the above and from www.newcapitalfunds.com. A summary of investor rights is available at: https://www.efgam.com/newcapitalfunds/Summary-Investor-Rights.html.

Country of origin of the collective investment scheme: Ireland

Investment products may be subject to investment risks, involving but not limited to, currency exchange and market risks, fluctuations in value, liquidity risk and, where applicable, possible loss of principal invested.