- Date:

- Author:

- GianLuigi Mandruzzato

Senior Economist

The European Central Bank (ECB) is expected by markets to cut interest rates by 25 basis points in December, bringing the deposit facility rate to 3%. Monetary policy remains restrictive as inflation falls near to 2% and gross domestic product (GDP) growth risks are tilted to the downside. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the outlook for the eurozone policy rate and concludes that the trough could be lower than markets discount.

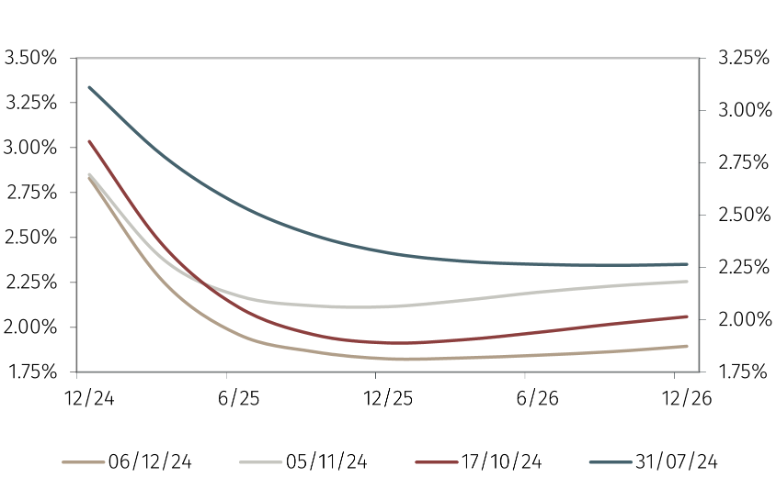

It is widely anticipated that on 12 December the ECB Governing Council will reduce the deposit facility rate (DFR) by 25 basis points, bringing it to 3%. It is also apparent that monetary policy easing will continue in 2025 reflecting the forecast that inflation returns to the ECB’s 2% target and that GDP growth remains below potential. Short-term interest rate futures anticipate that the ECB will cut the DFR towards 1.75% by the end of next year (see Chart 1).

Chart 1. Eurozone 3-month interbank rate implied in futures contracts

It is interesting to assess what the minimum level of interest rates could be in this monetary policy cycle. Two elements are crucial to answering this question: the level of the neutral real policy interest rate, i.e. the one at which monetary policy neither restricts nor stimulates economic growth, and the inflation and growth expectations for the next few quarters.

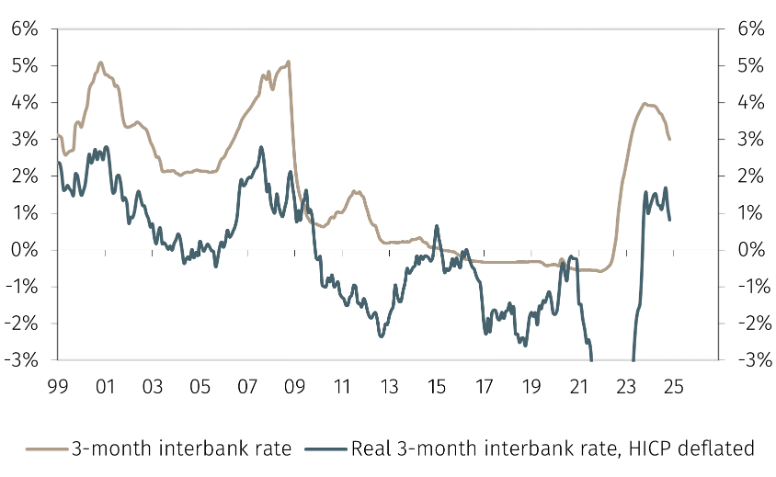

The neutral real rate is not observable and we must rely on an estimate of its value. Opinions expressed by members of the ECB Governing Council point to a range between 0 and 0.5%. If inflation in the eurozone were to settle at the 2% target and GDP were to grow in line with potential, the DFR should be between 2% and 2.5%. Currently, the real interest rate in the eurozone is 0.8%, a level that is still restrictive although less so than in the recent past (see Chart 2).

Chart 2. Eurozone nominal and real short-term rates

However, inflation in the eurozone has been running at a pace below 2% for several months. Annualised quarterly changes in both headline and core inflation, which excludes energy and food prices, point to the possibility of inflation falling towards 1.5% in the first half of next year. The decline could be even more pronounced if, as suggested by business surveys, increases in services prices slow more than in recent months.

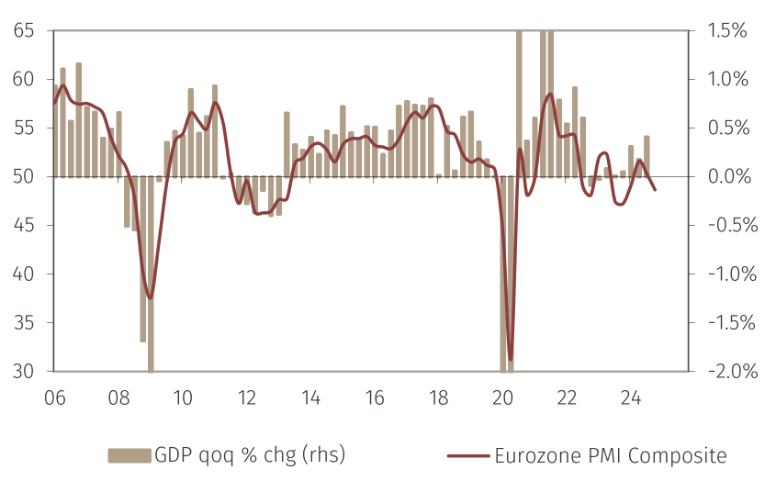

If so, a DFR level of 1.75% would be at the high end of the neutral range if not still moderately restrictive. The monetary policy stance would be excessively punitive for growth. The eurozone economy has disappointed since late 2022 and consensus among analysts is for GDP growth of around 1% in 2025, below potential for the third consecutive year (see Chart 3). Risks to this forecast remain on the downside due to political uncertainty in Germany and France - although the German elections could improve the medium-term growth outlook - the ongoing weakness of the Chinese economy, and the threat of tariffs by President-elect Trump.

Chart 3. Purchasing Managers’ Index composite and GDP growth

Weak growth suggests that monetary policy should be expansionary to avoid inflation falling significantly below the central bank's target. The real rate should therefore be negative.

If the data confirms this scenario and the ECB acknowledges the case for expansionary monetary policy, the DFR should probably be cut to at least 1.25%, around 50 basis points lower than what markets are pricing in.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.