- Date:

- Read time:

- 10 mins

- Author:

- GianLuigi Mandruzzato and Damian Burkhardt

Senior Economist and Senior Portfolio Manager

The ‘America First’ policies introduced by the Trump administration have triggered a rethink of global capital allocation. In this edition of InFocus, Senior Portfolio Manager Damian Burkhardt and Senior Economist GianLuigi Mandruzzato look at the merits of Swiss assets within this strategic shift.

The ‘America First’ trade policies being pursued by the US administration have resulted in a sharp increase in economic uncertainty. Investors have become wary of the potential adverse consequences of Trump’s polices on the US economy, resulting in renewed assessment of the merits of strategically pivoting away from US assets.1

In this context, we believe that Swiss assets – including equities and the franc – stand high among the beneficiaries of capital outflows from the US. The country’s inherent stability and resilience offer a compelling alternative to US policy unpredictability for global investors as they reconsider their willingness to be exposed to US assets. This is evident in the reduced holdings of US Treasuries by non-US residents since the beginning of the year (see Figure 1).

The US economy has long faced challenges related to its durable and widening budget and trade deficits. These twin deficits create a dependency on foreign capital, rendering the US economy susceptible to fluctuations in investor sentiment. Heightened trade tensions and the adoption of protectionist policies risk exacerbating these vulnerabilities. Disruptions to global trade flows would be expected to lead also to reduced foreign portfolio and direct investment in the US, casting a shadow over the US economic outlook.

Beyond the surge in global market volatility, Trump’s new trade policies may also represent a catalyst for global investors reconsidering their strategic asset allocation. The imposition of tariffs, aimed at revitalising US domestic manufacturing and reducing the trade deficit, has triggered retaliatory measures from China, escalating the spectre of a trade war between the two largest world economies. Although the worst-case scenario seems to have been avoided, these tensions risk impacting negatively US corporate earnings and erode investor confidence, prompting a comprehensive reallocation of global capital away from US markets.

Non-US investors, corporates and individuals will also reconsider their holdings of US assets and allocation of capital to the US because of section 899 of the One Big Beautiful Bill Act that the US Senate is considering after already having been passed by the House of Representatives. The new provision would impose increased retaliatory US federal income and withholding taxes on the income of foreign persons in jurisdictions that have adopted “unfair foreign taxes” according to the US administration. The increased tax rates would also apply to their holdings of US assets, including government and corporate bonds and equities.

Switzerland’s safe haven assets should come back in focus

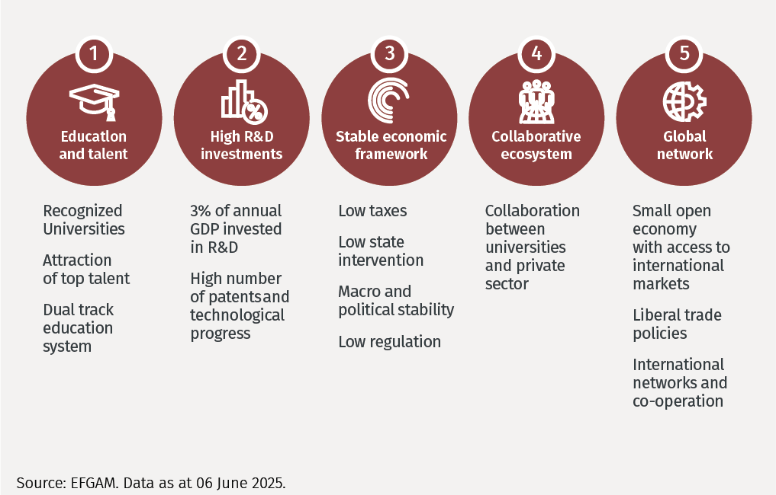

When looking to reallocate capital away from the US, in our view Switzerland provides an attractive alternative as investors favour countries with strong institutions, a solid legal framework and a structurally resilient economy. Switzerland performs exceptionally well across all these structural success factors (see Figure 2), which helps the country maintain its appeal as a unique investment destination.

Figure 2. Switzerland's structural strengths

Amid all the debate in the US about policies that could devalue the dollar in order to revive its manufacturing base,2 Switzerland is a prime example that defies that logic. The strength of the Swiss franc has not compromised its global competitiveness. In fact, Switzerland combines one of the world’s strongest currencies with a robust manufacturing sector. This is reinforced by its top ranking in the latest IMD World Competitiveness Report in June 2025, where it was recognised as the most competitive country globally – demonstrating both its stability and dynamism. Switzerland’s safe-haven status reflects its unparalleled political and economic resilience, as illustrated by low unemployment rates, a flexible job market, a pro-business environment with low tax rates and little government intervention.

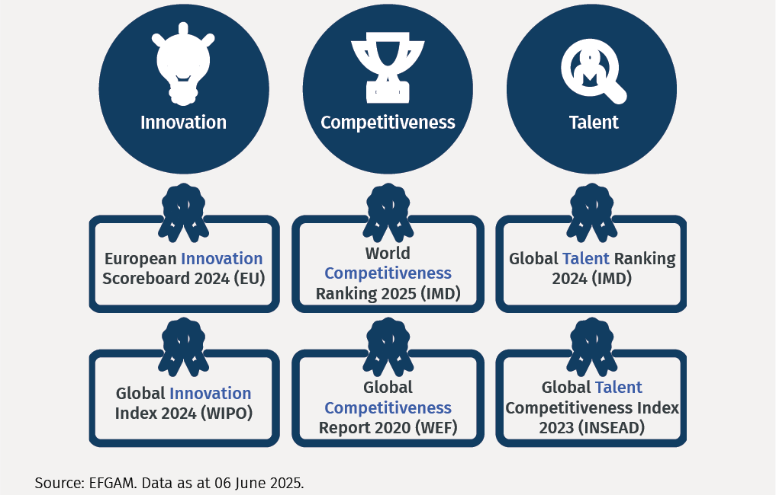

In addition, as a high-wage, high-cost economy without natural resources, continued innovation is key to Switzerland’s economic model. This is particularly evident in Switzerland’s position as one of the top spenders worldwide on Research & Development and being Number 1 innovation leader globally for 14 consecutive years.3 In today’s global knowledge-economy – in which competitive advantage is created by intellectual capital and patents rather than tangible resources underground – having one of the most skilled labour forces underpins Switzerland’s leadership across key industries, including finance, medical technology, pharmaceutical and precision manufacturing (see Figure 3).

Figure 3. Switzerland's innovation, competitiveness and talent

As a result, the equities of Swiss companies operating in this supportive business environment offer a compelling case for global portfolio diversification.

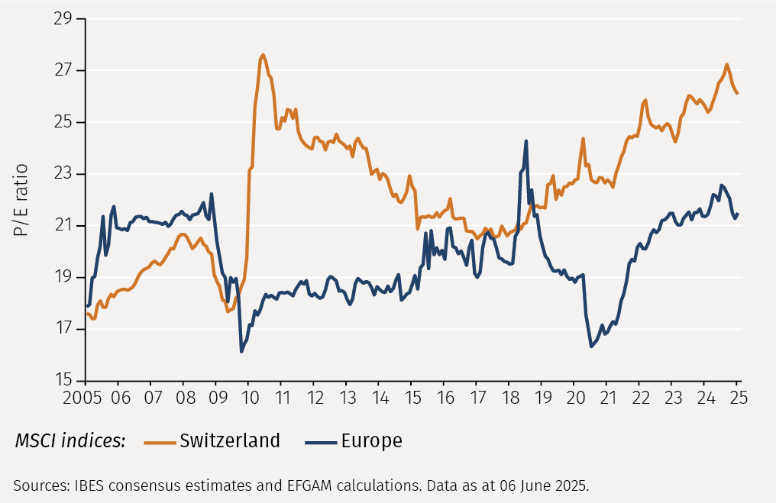

Swiss equities provide access to high-quality and highly innovative companies. The innovative nature of many Swiss companies is a hidden performance driver that drives sustained pricing power and value creation as measured by the forward return on equity compared to European peers (see Figure 4).

Figure 4. 12-month forward price-to-earnings ratio

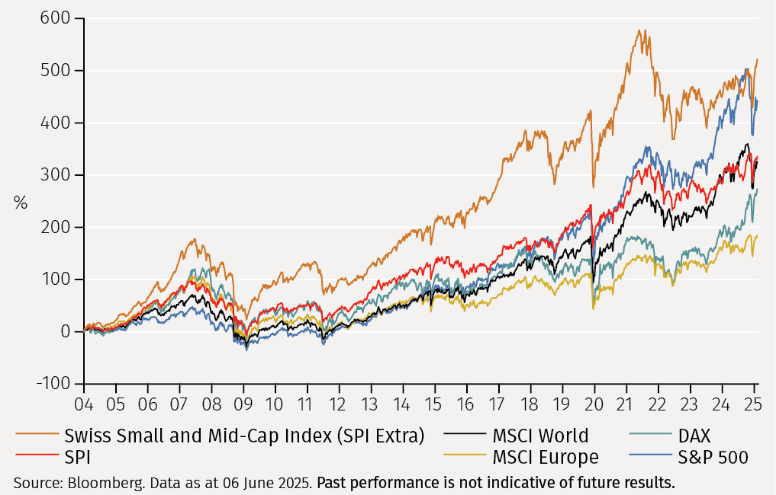

This is a factor that contributes to the attractiveness of Swiss equities - in particular Swiss Small & Mid-Caps – and which is reflected in Swiss equities being one of the best performing asset classes globally over the last 20 years (see Figure 5).

Figure 5. Total returns 2004-2025 YTD

In addition, the Swiss equity market offers substantial exposure to defensive sectors such as healthcare and consumer staples, resulting in less volatile returns during periods of market turbulence.

Furthermore, the safe-haven status of the Swiss franc could enhance the attractiveness of Swiss assets. During times of global economic uncertainty, investors gravitate towards the franc, driving up its value and reinforcing its reputation as a reliable store of wealth. This is underpinned by low government debt, high government effectiveness, reliable rule of law, stable governments, and the nation’s long history of neutrality.

This is reflected in the historical returns of US and Swiss equities. The correlation of Swiss equity returns to US equity returns in local currency terms over the last 35 years is lower than, but close to, unity, pointing to a moderate increase in portfolio diversification from additional exposure to Swiss equities (see Figure 6).4

Notably, the correlation decreases meaningfully when the returns of Swiss equities are expressed in US dollar terms, signalling a magnified diversification benefit as the Swiss franc safe haven status takes effect (see Figure 7).

Despite the rally this year, the Swiss franc remains undervalued vis-à-vis the US dollar on a Purchasing Power Parity basis (see Figure 8). The Swiss franc has steadily appreciated over the years, resulting in it being the world’s strongest currency since the end of the Bretton Woods system in 1972. Switzerland’s large external trade surplus highlights that the strength of the Swiss franc has not undermined the country’s competitiveness.

In contrast, the strength of the Swiss franc has acted as a catalyst for Swiss companies to innovate and remain competitive in global markets. Indeed, many commentators have noted that despite the steady rise of the franc, Switzerland boasts a very strong manufacturing base, raising doubts about the effectiveness of the US administration’s strategy of devaluing the dollar to boost the US industrial sector.5

Conclusions

The ‘America First’ policies pursued by the US administration are unsettling the global economy, fostering a reallocation of global capital to reduce exposure to US related risks.

The inherent stability of the Swiss economy, the nation’s prudent fiscal policies and resilient financial sector make Swiss assets a compelling alternative for investors seeking refuge from market volatility and the unpredictability of US policy.

These characteristics underpin both the Swiss franc and Swiss corporates, which benefit from leading market positions in niches driven by a high degree of innovation, high-quality characteristics and being embedded in a stable political and pro-business environment that attracts talent. We believe that this combination makes Swiss equities attractive both as a portfolio diversifier and as a contributor to returns in an increasingly uncertain world.

1See ‘Big investors shift away from US markets’, Financial Times, 05 June 2025. https://www.ft.com/content/019a275c-ab14-4ac3-8a7e-68758dd234a8

2Politico (April 2025): https://www.politico.com/news/2024/04/15/devaluing-dollar-trump-trade-war-00152009

3Global Innovation Index 2024 (World Intellectual Property Organization) https://www.wipo.int/en/web/global-innovation-index

4Correlation, ranging from -1 to 1, is a measure of how closely the returns on a pair of assets move together. When the correlation between the returns of two assets is 1, they are perfectly and positively correlated, meaning they move together in the same direction.

5 See ‘The world’s strongest currency is also super-competitive’, Financial Times, 02 June 2026. https://tinyurl.com/3vv4akvx

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.