- Date:

- Read time:

- 10 mins

Welcome to the May edition of InView: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

April was a rollercoaster month for financial markets, triggered by President Trump’s tariff announcements on what he dubbed Liberation Day on 2 April. The MSCI ACWI index rose 1.0% over the month as a whole, which might lead to the erroneous conclusion that it was a relatively quiet month. However, the tariff announcement on 2 April was followed by a decline of more than 11% in the index over four days that was halted only by the announcement of a 90-day US tariff pause. Subsequent backtracking by Trump on certain sectoral tariffs, such as on technology and automotives, together with optimism regarding trade negotiations with some countries like India, South Korea and Japan helped global stock markets recover.

Nonetheless, events of the past few weeks will have lasting consequences on markets and geopolitics. In particular, the role of the dollar as a global reserve currency is being seriously questioned due to the unpredictability of the US administration’s actions and the difficulty in understanding what its strategy is. The decline in the dollar’s trade-weighted exchange rate of more than 4% over the month, which brought the year-to-date decline to over 8%, is perhaps the start of a trend.

While the local currency performance of many major stock indices has been similar, one consequence of the US dollar’s decline is that the US market has significantly underperformed its peers when expressed in the same currency. Furthermore, emerging markets have risen more than developed ones, consistent with the historical observation that they benefit from a weaker greenback.

Another asset that has benefited from tariff uncertainty and the weakness of the US dollar has been gold, the price of which set another record by touching USD 3,500 per ounce. Gold’s safe-haven characteristics at the same time as some central banks are seeking to diversify their currency reserves suggest that demand for gold will remain high in the near future.

In this highly uncertain environment, many companies have suspended earnings guidance for the next few quarters. Our preference in this context is to reduce active risk in portfolios and maintain positions close to strategic benchmarks. This paid off in April, not only due to the equity market recovery in the second half of the month but also due to bond volatility, which saw yields initially fall then rise sharply before finishing the month little changed. A slight overweight in alternative investments is advisable as a diversifying element in portfolios and as an asset class that can better take advantage of idiosyncratic opportunities that arise in phases of high market volatility.

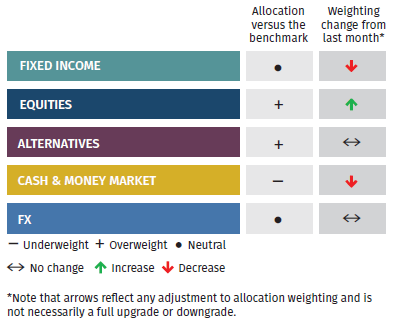

Asset Allocation

Global Allocation

It appears that we are likely past peak-tariff pain with President Trump walking back on certain tariffs and looking to strike deals with some countries. Despite this there remains a large degree of volatility and as such we don’t believe that it is currently the right time to make any major changes to our broad allocation. Instead, changes have come about from a slight level of market drift. Within equities, the allocation has drifted up just above the neutral level, and for now we are waiting on a valuation signal plus a catalyst to become more bullish. Meanwhile the marginal overweight to fixed income has eroded with drift and is now back in line with the neutral allocation. Alternatives exposure remains unchanged while cash levels are being taken down a fraction in a slight rebalancing.

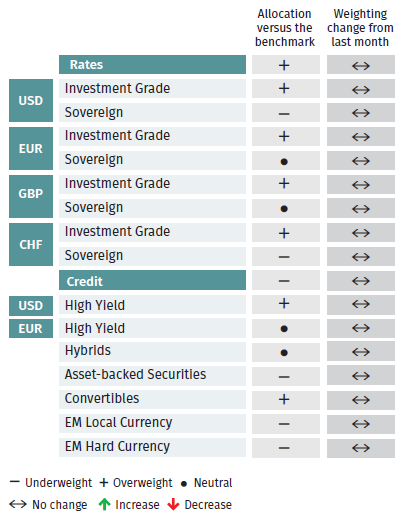

Fixed Income

No changes are being made within our fixed income allocation this month. Previously the euro high yield allocation was increased to neutral on the back of better economic conditions in the region. US high yield remains overweight. Owing to the widening in investment grade spreads as a result of US recession fears, last month we increased our allocation to US investment grade credit, taking it further overweight. Meanwhile the euro-denominated IG overweight was reduced given the big movement in government bonds previously. Within sovereigns, we hold a neutral position for USD as our target on the US 10-year was achieved. There is little carry in Swiss sovereigns, so CHF sovereigns are underweight. Duration is maintained slightly below the benchmark.

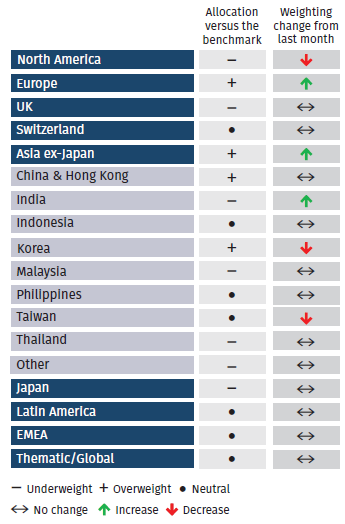

Equities

The main move within our equities positioning was a slight adjustment to US equities, taking into account the market drift. Given the drift lower due to market movements, we used this as an opportunity to add back some US exposure, helped by improving sentiment around tariffs, although this move still represents an underweight versus the benchmark. To balance out this move, minor adjustments were made to Europe and Asia ex-Japan. The EFGAM Valuation model has become marginally cheaper over the month, but broadly remains in neutral territory. The UK and Europe appear slightly cheaper, with Europe seeing a meaningful move in earnings expectations, whereas the US has been sequentially lower earnings expectations due to significant uncertainty regarding trade policy.

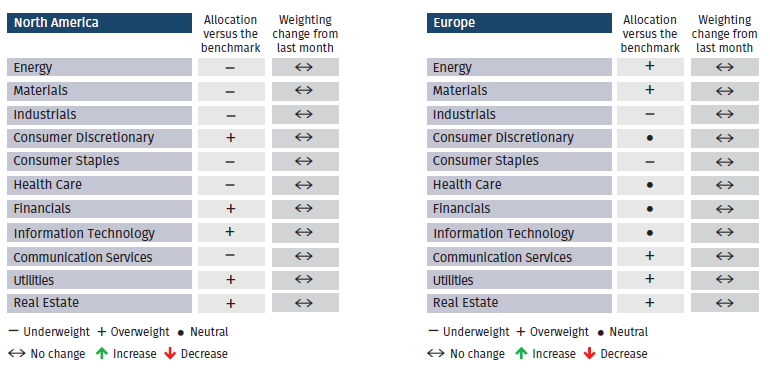

Equity Sectors

Equity Sector Views

UK

Given increasing risks from geopolitics, inflationary pressures, and slowing economic growth, we have increased our exposure to defensive industrial names (including aerospace and defence), with the sector remaining our largest overweight.

We believe that the UK is likely to experience rising inflationary pressures from April when higher national wages and employer payroll taxes come in to play, and that this will likely lead to higher-for-longer rates. We have increased our weighting in banks this year as a result, with financials now moving up to our second largest sector overweight.

We continue to see an opportunity for the outperformance of UK midcaps over the coming quarters, reversing a multi-year period of underperformance through high inflation and interest rates, as both of these factors normalise. Information technology has been a sector in which we have found specialist UK companies trading on attractive valuations in our view backed by strong structural growth tailwinds.

US

With Trump’s tariffs creating uncertainty, we previously reduced our overweight industrials position to neutral. This month we are upgrading information technology to a marginal overweight due to artificial intelligence trends still holding firm overall. It should be noted that we had tempered our overweight move over fears that the Department of Government Efficiency could slow down areas like software. To fund this move we had reduced our consumer discretionary overweight. Financials were also slightly reduced but continue to be overweight, with the reduction coming from non-bank financials.

Europe

We recently conducted a full review of European sector allocations which had prompted several changes. Amongst those changes we had further added to financials, taking it to neutral, focusing primarily on European banks. This reflected better fundamentals, deregulation and cyclical conditions. This was balanced out by a reduction to healthcare exposure, moving from overweight to now neutral. Industrials and consumer staples are the areas where we are more cautious on relative to the benchmark.

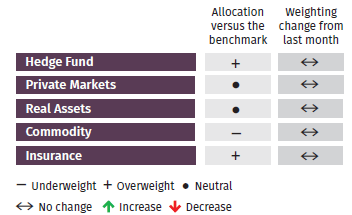

Alternatives

Last month we increased our allocation to hedge funds, taking it from neutral to overweight. Within hedge funds there is preference for CTA (commodity trading adviser) trend following strategies and discretionary macro. While increasing hedge funds, to maintain the broad risk contribution of the portfolio, our commodities and insurance allocations were previously reduced. The insurance allocation remains overweight while commodities are underweight, with oil still looking weak and gold accounting for our only exposure.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.