- Date:

- Read time:

- 5 mins

- Author:

- Stefan Gerlach

Chief Economist

In this Macro Flash Note, EFG Bank Chief Economist Stefan Gerlach uses the Taylor Rule to examine how the Federal Reserve might respond to the economic consequences of the Trump administration’s recently announced tariffs. The analysis suggests the Fed would cut interest rates by 100 basis points only if there is a significant deterioration in economic activity, which financial markets appear to be pricing in.

Recent developments in US trade policy — particularly the announcement of sweeping new tariffs by the Trump administration on what has been referred to as “Liberation Day” — raise questions about the likely response of the Federal Reserve. The effects on inflation and economic activity are unclear, as they will also depend on whether and how foreign countries choose to retaliate. To analyse the Fed’s potential policy choices, one ideally needs a fully articulated macroeconomic model. In the absence of that, this note uses a simple Taylor Rule to offer a first rough assessment of how the central bank might react.

The Taylor Rule Framework

Originally proposed by John Taylor in 1993, the rule was merely intended to summarise how the Federal Reserve had set interest rates in the late 1980s and early 1990s.1 It has since become a standard reference in monetary policy analysis. According to the original specification, the interest rate is determined by four main elements:

1. The Equilibrium Real Interest Rate: Taylor assumed this rate to be 2%. More recent estimates suggest it may be lower. For the purposes of this exercise, a value of 0.75% is used, which is consistent with recent estimates from staff economists at the Federal Reserve Bank of New York.2

2. Inflation: The rule uses the four-quarter change in the GDP deflator, a measure of the prices of domestically produced goods and services. This is relevant because it excludes all imported goods and services and may therefore be less sensitive to tariff-induced price changes than the consumer price index.

3. The Inflation Gap: The difference between actual inflation and the inflation target, assumed to be 2%, is assigned a response coefficient of 0.5. A one percentage point increase in inflation thus has two effects on interest rates: it raises interest rates one-for-one as mentioned above, and by an additional 0.5% as inflation rises relative to target.

4. The Output Gap: The deviation of real GDP from potential GDP is also given a coefficient of 0.5. A one percentage point shortfall in output relative to potential leads to a 0.5 percentage point reduction in the interest rate.

Current Conditions

Based on recent data, the output gap in the fourth quarter of 2024 was approximately 1.9%, and the four-quarter change in the GDP deflator was 2.3%. Since these data series used in the rule may not be familiar to all readers, they are shown in the chart below.

Chair Jerome Powell has recently indicated that the newly announced tariffs are likely to place upward pressure on inflation while weighing on economic activity. The Taylor Rule offers a way to think about the implications of such a combination.

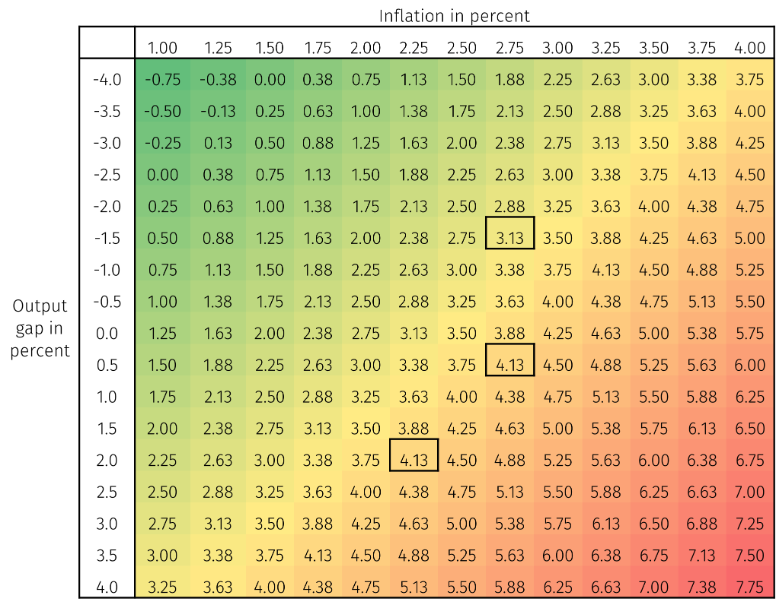

The table below shows the policy rate implied by the Taylor Rule for various combinations of inflation and output gaps. Assuming an equilibrium real interest rate of 0.75% and the 2024Q4 values of inflation and the output gap, the implied policy rate is 4.15%.

Table 1. Taylor Rule implied policy rate

This is slightly below the current federal funds target range of 4.25% to 4.50% and is consistent with the view that in the absence of new trade restrictions, the Fed would have continued to normalise monetary policy by cutting interest rates by 0.25% at its next meeting.

Potential Effects of the Tariffs

To see how the tariffs may impact monetary policy, suppose inflation increases to 2.75%, while the output gap narrows from 1.9% to 0.5%. Under these conditions, the implied policy rate changes little from the earlier estimate. The upward pressure from inflation is broadly offset by the weaker output, and the rule suggests that the Federal Reserve might maintain its current stance.

Market expectations, however, appear more pessimistic. Interest rate futures suggest that four rate cuts are anticipated by the end of 20253. A scenario consistent with such expectations might involve a decline in the output gap to -1.0% while inflation rises to 2.75%.4

Summing up

The Taylor Rule is a simple framework and does not capture interest rate setting by the Fed fully. Nevertheless, it is informative. The results above suggest that significant monetary easing would be consistent with the rule only if economic activity deteriorates substantially, via declining investment, reduced confidence, financial volatility, or retaliatory trade actions by foreign governments.

If the effect of the tariffs is limited to a modest rise in inflation and a small reduction in the output gap, the Taylor Rule does not suggest a sharp change in monetary policy.

Looking ahead, further developments in trade policy, inflation, and economic activity will determine the appropriate policy path. As always, interest rate setting by the Federal Reserve will depend on the evolution of the data.

1 See https://web.stanford.edu/~johntayl/Papers/Discretion.PDF

2 See https://www.newyorkfed.org/research/policy/rstar

3 See https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

4 Given that the output gap was 1.9% in 2024Q4 and the CBO’s estimate of trend growth is 2.3%, real GDP would need to fall by 0.6% between 2024Q4 and 2025Q4 for the output gap to reach -1%. That would not be unusual in a recession: in the 140 quarters between 1990Q1-2024Q4 four-quarter GDP growth was below -0.6% in eight quarters or 6% of the time.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.