New Capital is part of EFG Asset Management. For more information visit: www.efg.com

Macro Flash Note

February FOMC Meeting

In this Macro Flash Note, Daniel Murray reviews the communications and decisions taken at the latest Federal Open Market Committee (FOMC) meeting.

As expected, the FOMC yesterday agreed to hike rates by 0.25%. This represents a slowdown relative to the pace of rate increases implemented through most of 2022. Accompanying the decision to hike rates was a sentence confirming the Fed’s intention to continue to shrink its balance sheet. All 12 FOMC members voted for the hike and for continued balance sheet shrinkage.1

This meeting did not include an updated Summary of Economic Projections (SEP) so there was no window on the Fed’s thinking with regards to the economy and the outlook for the fed funds rate. Instead, investors had to rely on the press conference hosted by FOMC Chair Powell to glean information. In that press conference, Powell adopted a hawkish tone, reiterating the need to keep policy tight until the data supports the view that inflation is fully under control. Powell stressed that he expects the fed funds rate to move higher and for the policy stance to remain restrictive “for some time”.

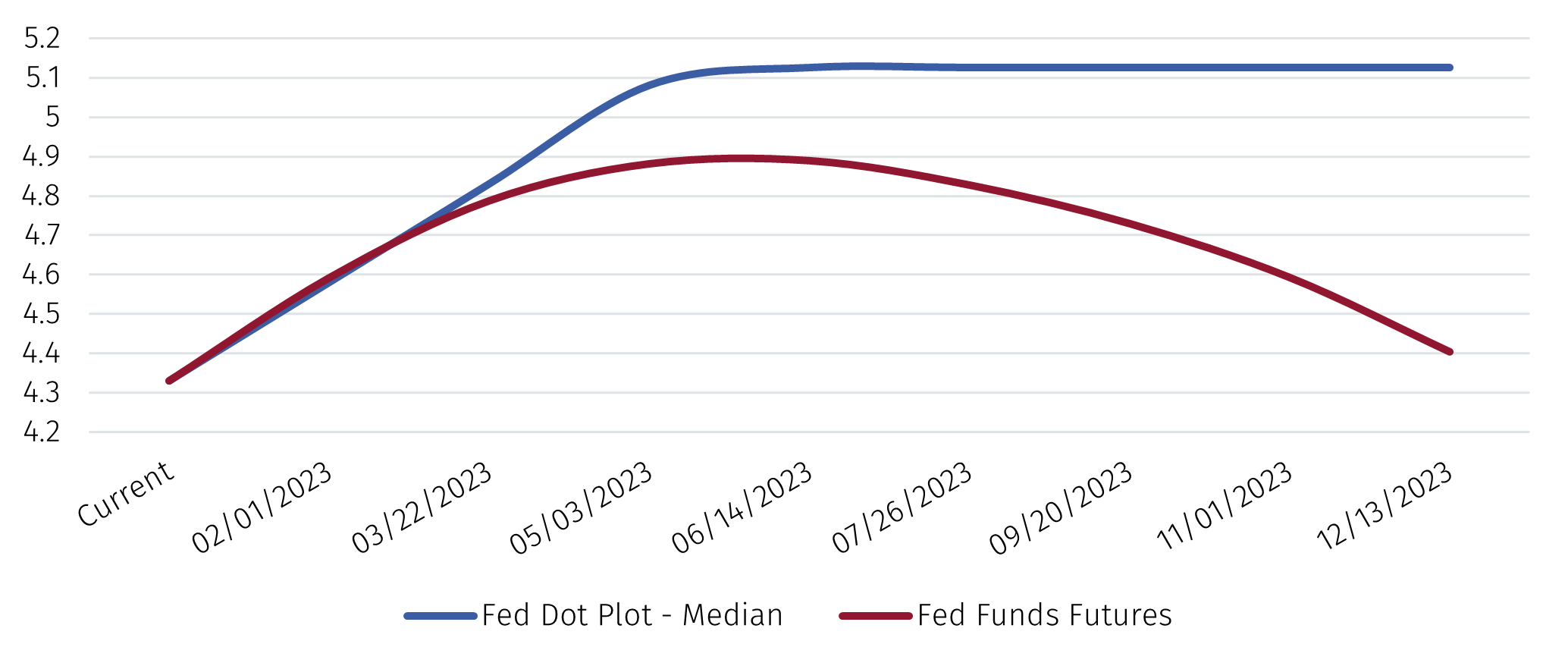

FOMC members, including Chair Powell, are incentivised to continue to talk tough even though there is a large gap between market expectations and the Fed’s own projections for the path of the fed funds rate, as encapsulated in the so-called Dot Plot (Chart 1). Whereas futures markets are pricing in a peak in the fed funds rate at under 5%, the most recent Dot Plot from December indicates that the median FOMC member thinks the fed funds rate will peak at a little over 5%. Moreover, the median FOMC member thinks the fed funds rate will remain unchanged throughout the year once its peak is reached whilst futures markets are pricing in cuts in the second half of the year.

Source: Federal Reserve, Bloomberg, EFG calculations. Data as of 02 February 2023.

Even if Chair Powell and other members of the FOMC privately have sympathy with the opinion expressed in futures markets – and there is no evidence that they do – there is an asymmetric payoff in making those views public. If the Fed adopts a less hawkish tone in its communications there is a risk financial market conditions loosen, providing a stimulus to the economy and offsetting the policy tightening at the short end of the curve. If the Fed relays a consistently hawkish message to markets that reinforces the view rates will stay higher for longer, the risk of market monetary conditions loosening is diminished. If the Fed subsequently needs to cut rates, for example because there is a significant slowdown in economic activity or inflation suddenly collapses, they can easily change their mind and justify earlier-than-expected stimulus. As long as they do this in a manner that is consistent with the data, their credibility will remain intact. In other words, the Fed can afford to overtighten and then cut if required to do so, for example if a recession ensues.

For the time being it is therefore rational to expect the Fed to continue to talk tough even if this differs from market expectations. With headline PCE inflation still at 5.0% and the 10-year Treasury yield at around 3.5% real interest rates are very low.2 Furthermore, the US labour market remains surprisingly tight. Until there is greater evidence that both inflation has slowed further towards target and the jobs market is suffering the Fed is unlikely to change tack. However, that may happen at a point in time sooner than indicated by the most recent Dot Plot.

1 The FOMC also reaffirmed its “Statement on Longer-Run Goals and Monetary Policy Strategy”.

2 Although interest rates on TIPS are in positive territory.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

What type of investor are you?

to view the content you have selected, please choose your country/region and then investor type from the menu:

![]()

You’re about to leave EFGAM website and enter into a 3rd party website

Third party website disclaimer

You are about to enter a third party website, which is owned and operated by an independent party over which EFGAM has no control ("3rd Party Website"). Any link you make to or from the 3rd Party Website will be at your own risk. Any use of the 3rd Party Website will be subject to and any information you provide will be governed by the terms of the 3rd Party Website, including those relating to confidentiality, data privacy and security.

EFGAM does not endorse or approve and makes no warranties, representations or undertakings relating to the content of the 3rd Party Website. EFGAM disclaims liability for any loss, damage and any other consequence resulting directly or indirectly from or relating to your access to the 3rd Party Website or any information that you may provide or any transaction conducted on or via the 3rd Party Web site or the failure of any information, goods or services posted or offered at the 3rd Party Website or any error, omission or misrepresentation on the 3rd Party Website or any computer virus arising from or system failure associated with the 3rd Party Website.

By clicking "Proceed", you confirm that you have read and agreed to the terms herein.