New Capital is part of EFG Asset Management. For more information visit: www.efg.com

Investment Insights

Global Growth Outlook

The World Bank and OECD recently updated their economic growth projections, with most economies suffering downgrades.1 2 In this Macro Flash Note, Sam Jochim summarises the changes and looks at the risk of further downgrades in projected growth.

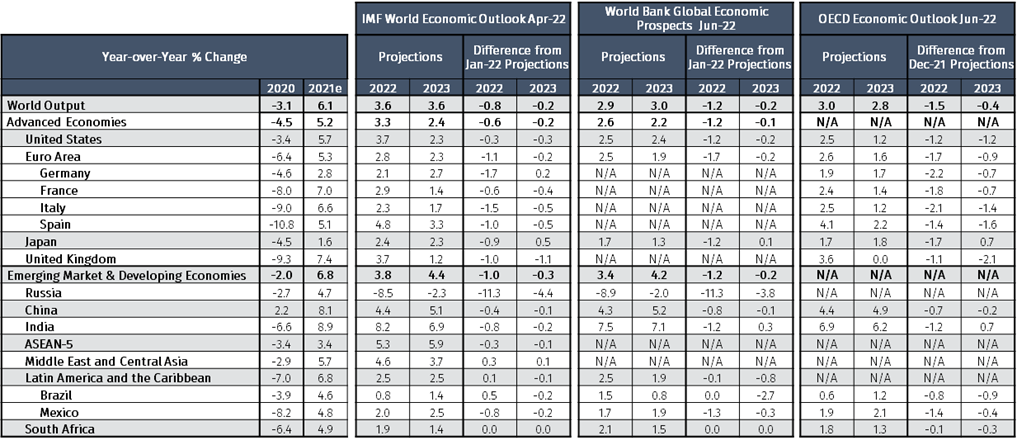

Following a strong recovery from the pandemic in 2021 (see Table 1), the growth outlook appeared to be broadly favourable for 2022 and 2023. Taking the December 2021 projection from the OECD and the January 2022 projections from the IMF and World Bank, annual global growth was expected between 4.1% and 4.5% in 2022.3 4 5 Since then, in its April 2022 World Economic Outlook, the IMF downgraded 2022 global growth projection by 0.8 percentage points to 3.6% - as discussed in a previous Macro Flash Note.6 The World Bank and OECD have now followed suit, downgrading their respective global growth forecasts for 2022 to around 3%.

Source: IMF, World Bank, OECD and EFGAM calculations. Data as at 20 June 2022.

The World Bank and OECD explain the downgrades to growth projections with two main factors. Firstly, Russia’s invasion of Ukraine, and secondly, China’s zero-Covid policy. The negative spillovers resulting from these shocks to the global economy are exacerbating pre-existing strains which emerged throughout the pandemic and during the recovery.

Perhaps the most important channel through which Russia’s invasion of Ukraine is impacting global growth is higher commodity prices. This has pushed inflation to a level higher than previously expected, leading to a faster pace of monetary tightening than had previously been accounted for in both the World Bank and OECD forecasts.

In a similar vein, China’s zero-Covid policy is also dampening the global growth outlook. Lockdowns in the first half of 2022, aimed at curbing Covid outbreaks, have resulted in key manufacturing cities and ports having subdued output. Combined with the war in Ukraine, which has made parts of the Black Sea inaccessible, this has heightened supply chain bottlenecks.

One of the most notable points from both the World Bank and OECD’s updated growth projections is the lack of upgrades to the outlook for 2023. Given the negative shocks impacting this year’s projections, a rebound may have been expected. Instead, growth is expected to remain around 3% in 2023. The underwhelming projected response by the global economy to the negative shocks in 2022 is a result of two main factors. The World Bank and OECD share the view that there will be a further unwinding of fiscal and monetary support which was provided during the pandemic. Furthermore, both organisations also factor in the lingering effects of the war into their projections. This is particularly true for the OECD, which incorporates an EU embargo of seaborne oil imports from Russia into its 2023 projections.

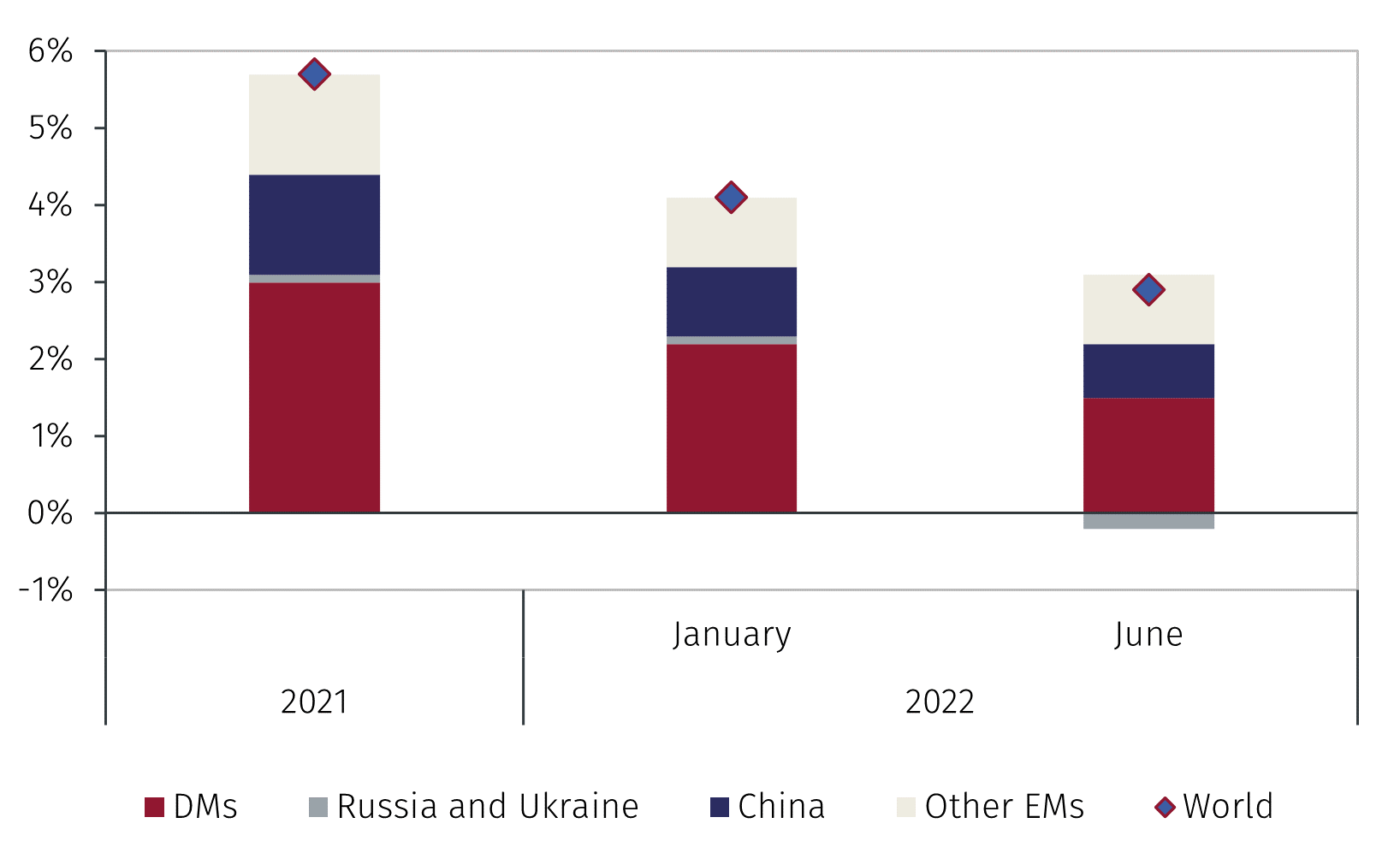

Figure 1 illustrates the World Bank’s projected impact of the war on global growth. Compared to January’s forecasts in which Russia and Ukraine contributed to global growth, they are now projected to detract from it. According to the World Bank, emerging markets such as Brazil and South Africa are still expected to grow by the same amount as in the January projections.

Source: World Bank. Data as at 20 June 2022

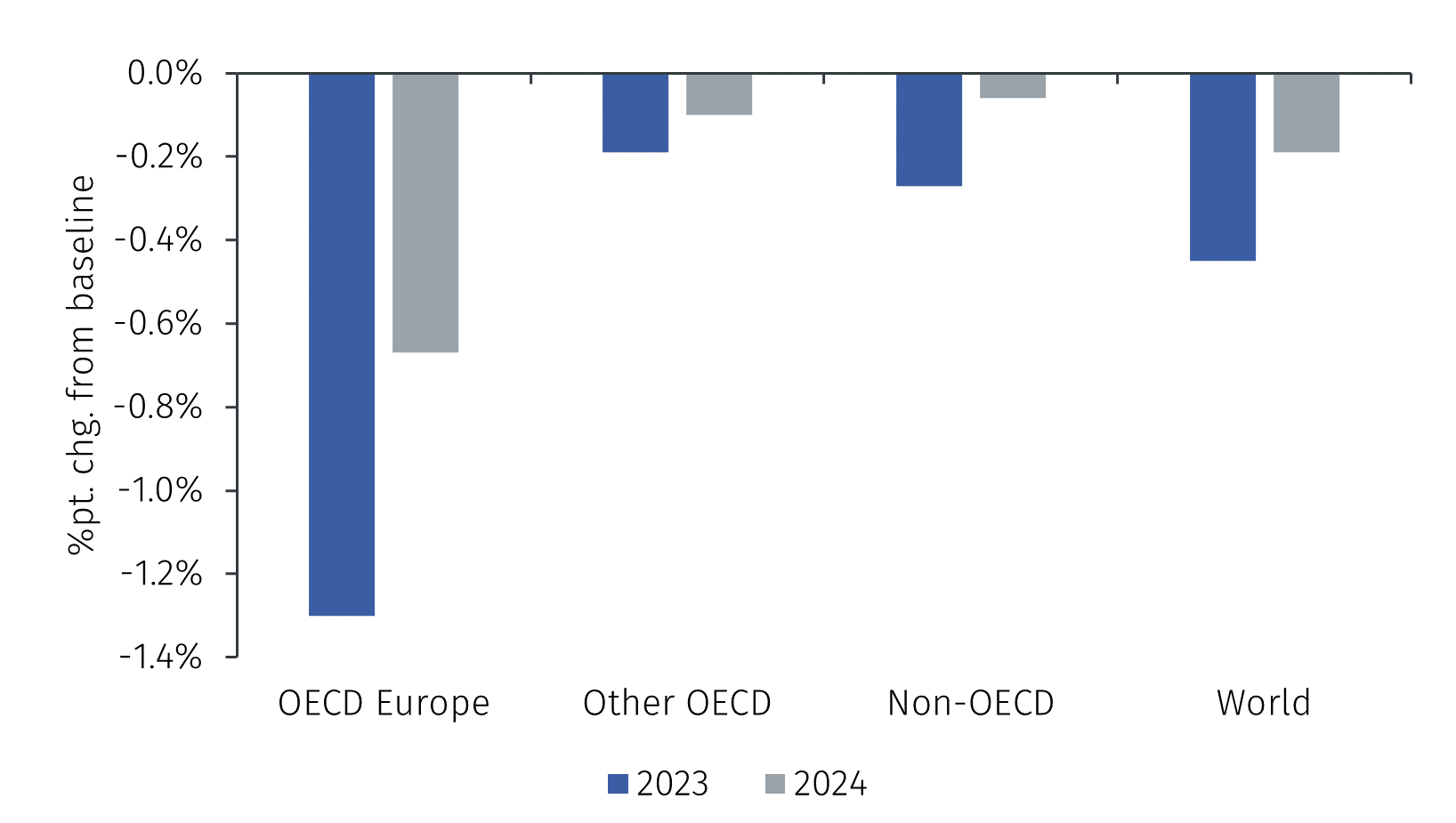

Both organisations also highlighted an elevated level of downside risk to the outlook. These could materialise in the form of a new wave of Covid leading to further lockdowns in China, an escalation of the war in Ukraine, or sanctions on Russia becoming more extreme. The OECD performed a scenario analysis of a complete European embargo on Russian gas, with the projected impact on growth in 2022 and 2023 shown in Figure 2.

Source: OECD. Data as at 20 June 2022.

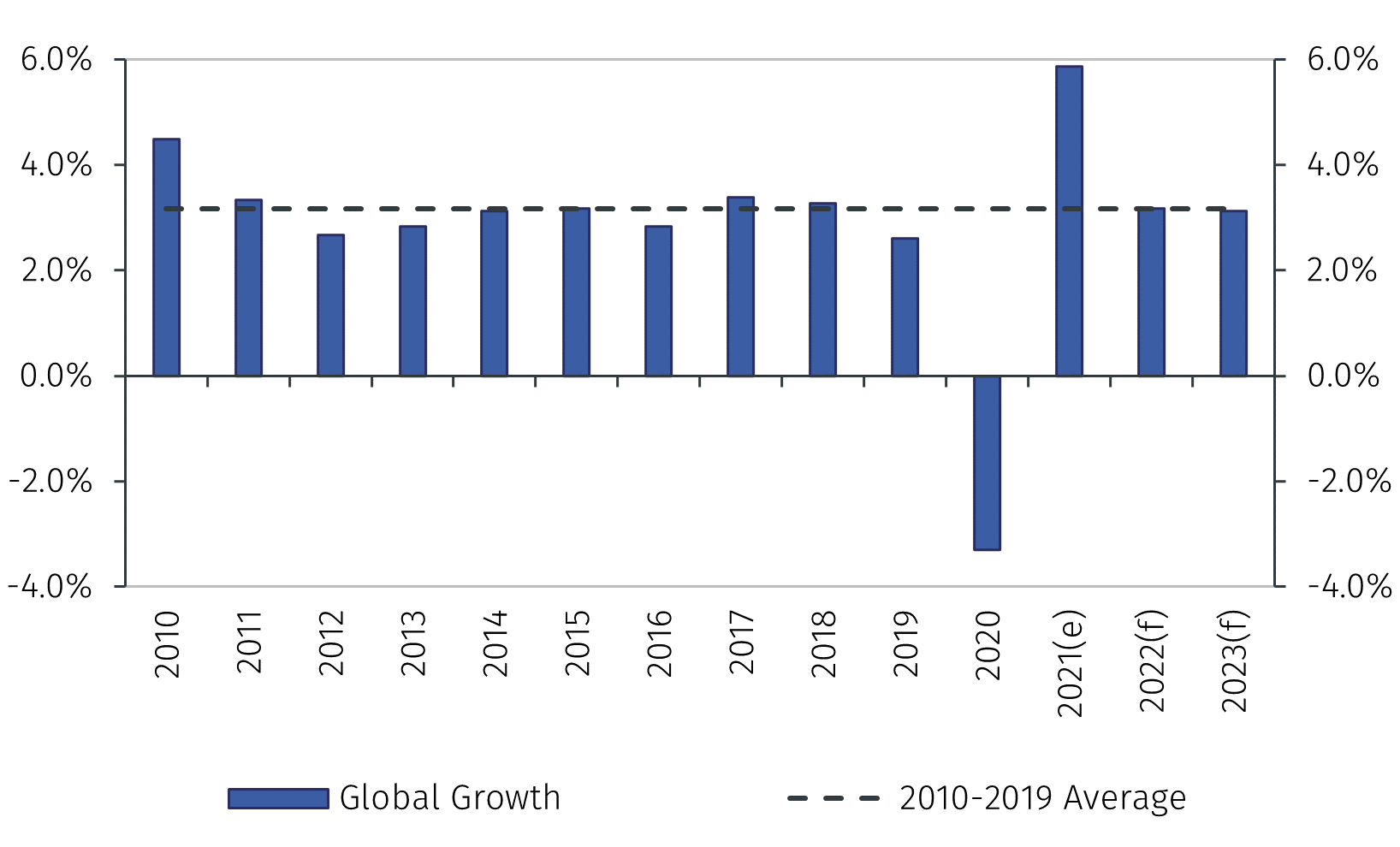

Given the consistency of the World Bank and OECD in their downgrades to growth projections, it is important to provide some context to the outlook. In the case that there are no further downgrades to growth throughout the year and the projections are realised at the end of the forecasting period, global growth would be broadly in line with its post-GFC and pre-Covid average (see Figure 3). This highlights the fact that although growth projections have been downgraded, they have come from a starting point which was above average.

Source: IMF, OECD, World Bank and EFGAM calculations. Data as at 20 June 2022.

In summary, both the World Bank and OECD have downgraded growth projections for many economies due to the impacts of the war in Ukraine and lockdowns in China. Despite this, growth is expected to remain broadly in line with its long-run average. There are significant risks to the outlook, however, which could see a further slowdown in the global economy compared to the level currently expected.

1 https://openknowledge.worldbank.org/bitstream/handle/10986/37224/Global-Economic-Prospects-June-2022-Global-Outlook.pdf

2 https://www.oecd-ilibrary.org/sites/62d0ca31-en/1/3/1/index.html?itemId=/content/publication/62d0ca31-en&_csp_=0cf9a35c204747c5f82f56787b31b42b&itemIGO=oecd&itemContentType=book

3 https://www.oecd-ilibrary.org/sites/66c5ac2c-en/index.html?itemId=/content/publication/66c5ac2c-en

4 https://www.imf.org/en/Publications/WEO/Issues/2022/01/25/world-economic-outlook-update-january-2022

5 https://openknowledge.worldbank.org/bitstream/handle/10986/36519/9781464817601.pdf

6 IMF: war sets back the global recovery (April 2022)

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London, W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

What type of investor are you?

to view the content you have selected, please choose your country/region and then investor type from the menu:

![]()

You’re about to leave EFGAM website and enter into a 3rd party website

Third party website disclaimer

You are about to enter a third party website, which is owned and operated by an independent party over which EFGAM has no control ("3rd Party Website"). Any link you make to or from the 3rd Party Website will be at your own risk. Any use of the 3rd Party Website will be subject to and any information you provide will be governed by the terms of the 3rd Party Website, including those relating to confidentiality, data privacy and security.

EFGAM does not endorse or approve and makes no warranties, representations or undertakings relating to the content of the 3rd Party Website. EFGAM disclaims liability for any loss, damage and any other consequence resulting directly or indirectly from or relating to your access to the 3rd Party Website or any information that you may provide or any transaction conducted on or via the 3rd Party Web site or the failure of any information, goods or services posted or offered at the 3rd Party Website or any error, omission or misrepresentation on the 3rd Party Website or any computer virus arising from or system failure associated with the 3rd Party Website.

By clicking "Proceed", you confirm that you have read and agreed to the terms herein.