- Date:

- Read time:

- 10 mins

Welcome to the December edition of InView:

Monthly Global House View. In this publication we

consider significant developments in the world’s

markets, and discuss our key convictions and

themes for the coming months.

The election of Donald Trump as US President and the Republican Party clean sweep of the House of Representatives and the Senate triggered a strong rally in global equities. The performance, which took the MSCI All Countries World Index to a new record, was driven mainly by the US market, which saw the S&P 500 index rise 5.7%, while most other markets have fallen or been rangebound since the US election day.

This reflects the expectation that the policies of the new US administration, including the imposition of tariffs on exports to the US, tax cuts, and a fight against illegal immigration, will favour growth in the US economy at the expense of its trading partners. A side effect of Trump's announced policies was an increase in inflation expectations in the US and upward revisions to expectations regarding the path of the Federal Reserve's monetary policy.

The initial rise in US Treasury yields was reversed after the appointment of Scott Bessent as Treasury Secretary, which markets believe will help to temper some of Trump’s more extreme policies. In the final trading days of November, US government bonds have recovered and yields have fallen below their level on election day.

In most other major economies, the revision of monetary policy expectations has been less pronounced than in the US and, in some instances, has even moved in a more dovish direction. This has resulted in a widening of some government yield spreads over US government bonds and boosted the US dollar against other currencies, in particular the euro.

The single currency and European assets were burdened by the threat of US tariffs, increased political uncertainty in Germany and France, and the weakness of the Chinese economy. However, the German general elections in February could produce an improved growth outlook thanks to a more expansionary fiscal policy and structural reforms under a new government. Furthermore, the expectation of further stimulus in China leaves room for a recovery in demand in 2025, which will benefit the European economy given strong trading links between the two.

The outlook for the coming weeks remains favourable for equity markets, in our view, partly due to momentum associated with the Trump trade and partly due to seasonal factors. However, it is more uncertain for government bonds. We confirm the preference for an overweight in equities, focused on the US, continental Europe and emerging Asia. Among fixed income assets, we suggest a reduction in the overweight on government bonds in favour of a reduced underweight on high yield bonds to reduce the duration of the portfolio while profiting from attractive yields and building confidence in the soft landing narrative.

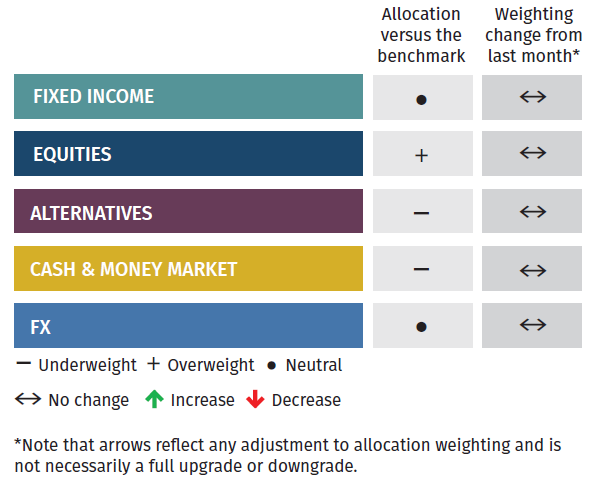

Asset Allocation

Global Allocation

Based on a balanced mandate, the matrix below shows our 6-12 month view on investment strategy. Given that we held an ad hoc asset allocation meeting immediately after the US election in which we made some sizeable adjustments, no additional changes are needed to our broad asset allocation. Our overweight to equities is maintained, fixed income is held at a neutral position, while alternatives and cash are underweight. There is a high level of optimism from investors about the incoming Trump administration, the potential for the Department of Government Efficiency to make significant improvements and some of the more market-friendly appointments such as Scott Bessent as Treasury Secretary. However, this could be a case of “buy the rumour and sell the fact” and it may be appropriate to scale down risk post-Trump inauguration once the honeymoon period ends.

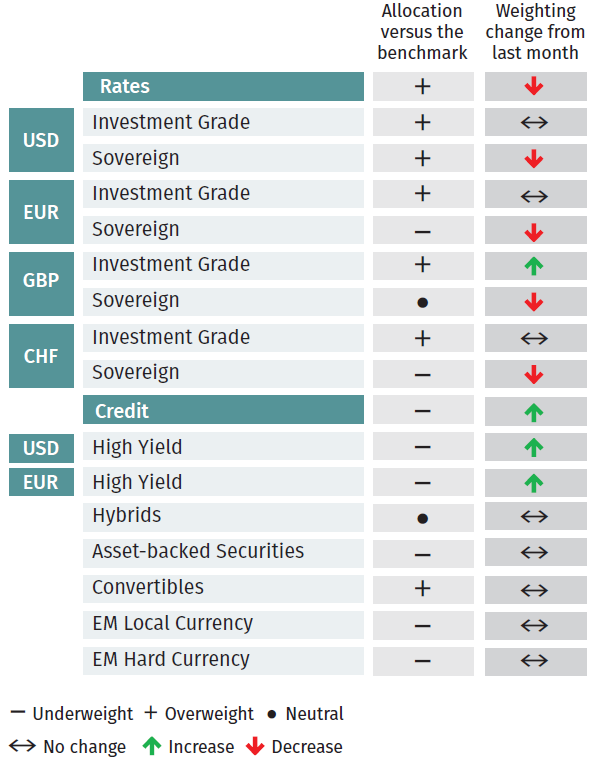

Fixed Income

USD sovereign bond exposure is being cut although we retain an overweight allocation. We expect that the Trump presidency will likely result in higher risk premia as we move into January 2025 although we are still in wait-and-see mode. A cut in duration should also be implemented in euro-based portfolios, with the euro curve influenced by the US treasury market and also starting to price in additional rate cuts. In the UK, the reduction proposed in sovereigns is larger given the influence from the US together with the additional domestic impact from the recent Autumn Budget. With Trump coming in and pro-growth policy likely to be enacted, the risks of significant spread widening has reduced, providing a more positive environment for high yield bonds. We are adding to both USD and EUR high yield but remain underweight. This has the potential to lower portfolio duration.

Equities

No changes are being made to the equity sub-asset allocation, having added to US exposure in the aftermath of the election. Despite the increase we still hold an underweight position versus the benchmark. While there are improved macro and risk factors in the US, we see little scope to move past the neutral level due to the sizeable weight of the US within the MSCI World Index benchmark. There is a possibility that European equities may close the gap with US equities in the coming months so we maintain our slight overweight to the region. Our valuation model points to European and UK equities becoming cheaper. Japanese equities have also got cheaper in recent weeks, moving to a more neutral zone, although it still looks to soon to begin closing our underweight position. The picture in Latin America looks challenging relative to the rest of the world but we hold a neutral allocation given how little it accounts for in the overall portfolio.

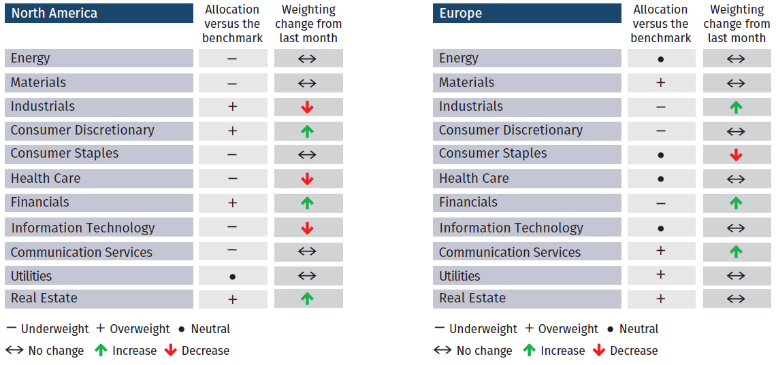

Equity Sectors

Equity Sector Views

UK

Following the outcome of the US election and an increasingly more resilient US macro recovery outlook, we have increased our exposure to internationally focused UK industrial names which are likely to benefit from this outlook, many of which will also benefit from the recent strengthening of the US dollar.

We continue to see an opportunity for the outperformance of UK midcaps over the coming quarters, reversing a multi-year period of underperformance through high inflation and interest rates as both of these factors normalise. Information Technology has been a sector where we have initiated several new positions recently that fit this theme, and where we have found specialist UK companies trading on attractive valuations backed by strong structural growth tailwinds.

This year we have also increased our weighting towards consumer discretionary given our more constructive outlook for improving real incomes for consumers. Our exposure is balanced between internationally focused Hotel & Leisure businesses as well as domestic UK recovery geared names, such as housebuilders, which will be supported by both falling rates and the new Labour government who aim to reform the planning permission system to boost economic growth.

US

We increased the portfolio cyclicality following the US election results. The election outcome lessened unpredictability while Trump’s policies are expected to deliver benefits to US companies in the upcoming months. Specifically, we are overweight in industrials, consumer discretionary and financials. Following the nomination of Robert Kennedy Junior as health secretary, we are downgrading our allocation into consumer staples and healthcare, owing to question marks on how aggressive his policies may be. We are underweight to defensive “bond proxy” stocks. Rising inflation expectations could result in interest rates staying high for an extended period. This scenario could put additional downward pressure on the valuation of defensive stocks.

Europe

In recent weeks we have added to cyclical sectors such as financials and industrials although both remain underweight. These trades should be funded by a reduction in healthcare and consumer staples. Our focus has been on adding capital to small and mid-caps versus the mega caps in the region.

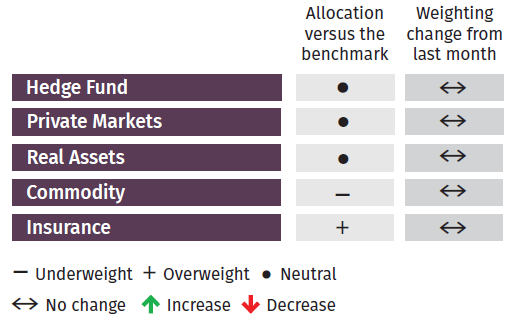

Alternatives

Last month we slightly increased our alternatives exposure, focusing on hedge funds and commodities. We expect that hedge funds could be poised to exploit more opportunities in a Trump regime. Meanwhile in our view Trump may be bearish for the oil price but better for the broader industrial and soft commodities. Insurance positioning remains overweight versus the benchmark, with our exposure being a useful portfolio component given its uncorrelated nature.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.