- Date:

- Read time:

- 3 mins

- Author:

- Samira Rahman

The April 2025 edition of the International Monetary Fund’s (IMF) World Economic Outlook presents a global economy entering a period of slower expansion, shaped by heightened policy uncertainty and persistent structural headwinds. In this Macro Flash Note, Samira Rahman summarises the latest report.

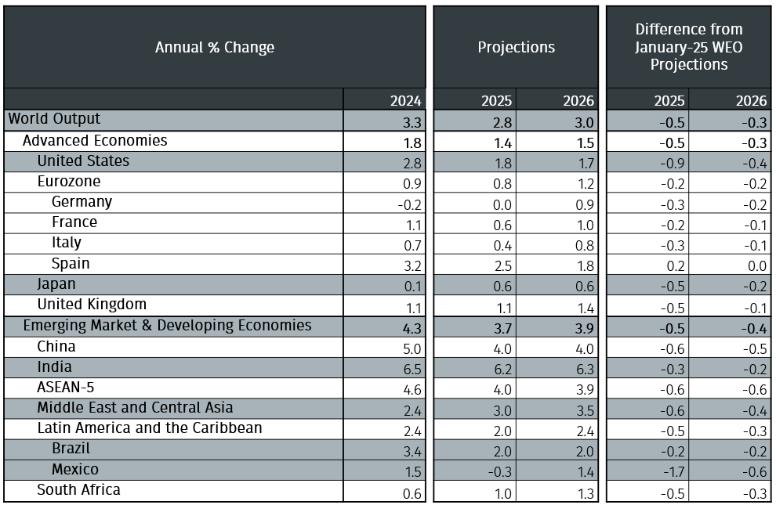

According to the IMF, global growth will slow from 3.3% in 2024 to 2.8% in 2025, reflecting a weak carryover from late 2024 and the impact of renewed trade tensions (see Table 1). While the IMF does not foresee a global recession, it notes that downside risks to the baseline forecast have intensified.

Table 1. IMF’s World Economic Outlook real GDP growth projections (% change, year-on-year)

IMF Growth Forecasts

The IMF’s reference scenario was finalised using information available until 14 April 2025 and incorporates key developments in US trade policy. On 2 April, the US imposed sweeping new tariffs on imports, triggering significant declines in global equity markets and sharp rises in bond yields. On 9 April, a pause was announced, with additional carve-outs for key sectors announced in the following days. According to the IMF, this policy sequence affected sentiment and risk pricing across economies and is reflected in the updated baseline projections.

In its analysis, the IMF estimates that global growth would have been projected at 3.2% in 2025 had trade tensions not escalated. The revised projection of 2.8% reflects both the direct effects of the changes to trade policy and the broader drag from policy uncertainty. In the US, GDP growth is expected to slow to 1.8%, down from 2.8% in 2024. In the view of the IMF, roughly 0.4% of this decline is due to tariff impacts and associated market disruptions.

In the eurozone, the IMF projects GDP growth to average 0.8% in 2025. Domestic demand remains subdued, while industrial activity continues to be constrained by energy price volatility and ongoing competitiveness concerns. Regional divergences persist, with Spain cited as a positive outlier, supported by resilient services and stronger-than-expected employment. The United Kingdom is forecast to grow by 1.1% though high inflation and housing affordability remain pressing challenges.

In emerging markets, the IMF expects China to grow by 4.0% in 2025. The outlook is burdened by weak household consumption, property sector weakness, and the adverse impact of trade policy developments. India, by contrast, is projected to maintain strong growth at 6.5%, underpinned by infrastructure investment and digital expansion. Southeast Asia is also highlighted as a relative bright spot, benefitting from trade reorientation and regional supply chain shifts. Latin America and Sub-Saharan Africa are expected to face more modest outcomes, reflecting debt vulnerabilities and low productivity.

Risks to the Outlook

The IMF outlines a range of risks to its baseline forecast, noting that the global economy entered 2025 with less momentum than previously expected. According to the report, data from Q4 2024 and early indicators for this year point to softer-than-expected activity, particularly in retail sales and manufacturing. This loss of momentum, when combined with policy shocks, raises the likelihood that global growth could underperform relative to current projections.

In its discussion of downside scenarios, the IMF points to trade fragmentation as a central concern. Further escalation of protectionist trade policies, particularly involving the US and China, could lead to reduced investment, lower productivity, and more persistent inflationary pressures. The IMF also highlights a broader deterioration in the perceived coherence and predictability of policy, which it describes as “epistemic uncertainty.” According to the IMF, this environment of uncertainty has negatively impacted confidence and long-term decision-making by firms.

Financial vulnerabilities are also underscored as a downside risk to global growth. In the view of the IMF, equity markets remain vulnerable to sharp corrections, especially in countries with elevated valuations and rising interest rates. Equally, borrowing costs have increased in many emerging markets, particularly those with dollar-denominated or short-maturity debt. The Fund warns that this combination could lead to corporate or sovereign stress, especially if inflation proves more persistent or capital flows reverse suddenly.

In its model-based risk scenarios, the IMF estimates that global growth could fall below 2.0% in 2025 with a 30% probability, should downside risks materialise. In that same scenario, the probability that global inflation exceeds 5.0% is estimated at 31%.

Although risks are tilted to the downside, the Fund also describes a set of upside risks to global growth. These include improved labour supply through higher participation and better migrant integration, stronger-than-expected productivity gains from digital and artificial intelligence adoption, and a stabilisation in global geopolitical tensions. According to the Fund, a shift toward greater international cooperation in trade policy could also help support confidence and reduce price pressures.

Conclusion

The IMF’s April 2025 World Economic Outlook describes a global economy losing momentum under the combined effects of elevated trade tensions, weakening demand, and structural challenges. The 2.8% baseline forecast for global GDP growth reflects not only recent developments in policy and financial markets, but also the IMF’s view that global resilience is being tested by increasingly complex and overlapping risks.

According to the report, the global policy environment remains a key factor in determining whether the world economy avoids a deeper slowdown. In its view, targeted reforms, transparent and consistent policy frameworks, and stronger multilateral coordination will be essential to rebuilding confidence and lifting medium-term growth.

The IMF concludes that the global economy remains adaptable, but the window for a smooth adjustment is narrowing. Without credible and coordinated policy efforts, the risks of fragmentation and stagnation may continue to rise.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.