- Date:

- Read time:

- 10 mins

- Author:

- Joaquin Thul

Since the election of Donald Trump in November 2024 discussions between the US and Mexico have focused on three main areas: trade, migration and drug trafficking. Trump has announced tariffs on Mexican imports which are due to take effect in March. In this edition of InFocus, Economist Joaquin Thul discusses the proposed tariffs and the possible scenarios ahead.

As he did in his first term, President Trump has threatened to impose tariffs on US imports from various countries.1 In Mexico’s case, this threat has not been linked to migration or trade imbalances. Regarding the former, the US has increased deportations of illegal migrants and reinforced security at its southern border. As for the latter, both countries have a solid trade relationship as part of the United States-Mexico-Canada (USMCA) trade agreement.

Trump’s arguments have focused on drug trafficking. The Executive Order issued on 1 February imposed a tariff of 25% on all imported goods from Mexico on grounds of a national economic emergency.2 It alleged Mexican authorities failed to prevent drug trafficking organizations (DTOs) from transporting illicit drugs, or products to manufacture them, into the US. An identical Order was issued against Canada with the same allegations.

Following negotiations, a second Executive Order acknowledged the “immediate steps” taken by Mexico, delaying the imposition of these tariffs for one month, until 4 March 2025.3 Mexico agreed to deploy 10,000 National Guard agents to combat DTOs, particularly for the traffic of fentanyl. Canada’s Prime Minister took a similar measure. However, given the subjective nature of some of Trump’s arguments it is unclear what will be needed to satisfy his demands and avoid an escalation of trade tensions.

Tariffs as a negotiating tool

During his first term Trump introduced tariffs on imports of steel, aluminum, solar panels and specific goods from China and the EU. Some of these were maintained during the Biden administration. From the US perspective, tariffs have the advantage that they can be implemented by the President through an Executive Order, without the need for Congressional approval.

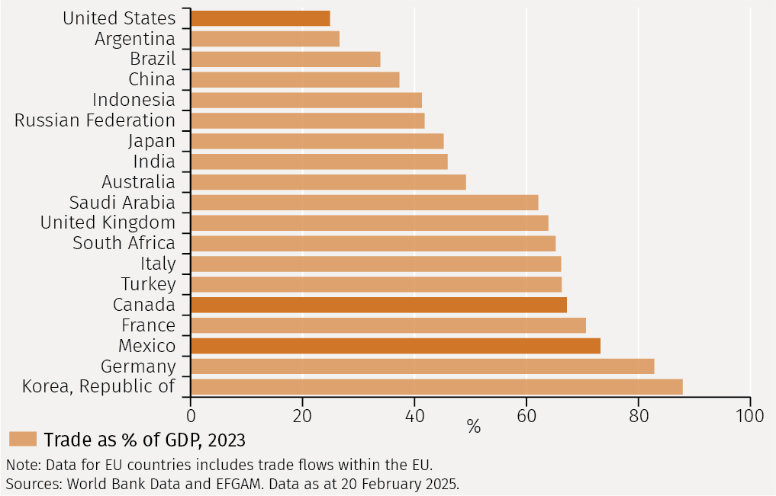

Mexico and Canada are highly dependent on trade, ranking among the top five by trade openness among G20 economies (see Figure 1). The US is the least open economy among the G20. Exports to the US represented around 80% of Mexican goods exports in 2023, and 75% of Canada’s goods exports. Therefore, both countries have incentives to concede to some of Trump’s demands and maintain preferential access to the US market.

Who pays for tariffs?

Tariffs imposed on US imports would be paid by American companies importing these goods. Importers will pass along the cost of tariffs to the American consumer, depending on their ability to do so.

American buyers could decide to buy less of these products or find a cheaper substitute in the domestic market, while Mexican or Canadian firms might choose to lower their export prices to avoid losing sales in the US. If firms are able to pass the cost of tariffs, in full or partially through a reduction of margins, to the American consumer it would boost US inflation.

American buyers could find a supplier in a country not targeted by tariffs, but costs of production and transport might make this too expensive. Firms might consider relocating to the US, however production costs might be higher and the relocation process could take years.

Therefore, we envisage three possible scenarios:

➡ Scenario 1: US imposes 25% tariff on all imports from Mexico and Canada, and an additional 10% tariff on China.

Although countries could retaliate, the importance of the US market as an export destination makes it is unlikely that Mexico will replicate US tariffs. An escalation of a trade war would represent the worst-case scenario for Mexico with a negative impact on activity and inflation.

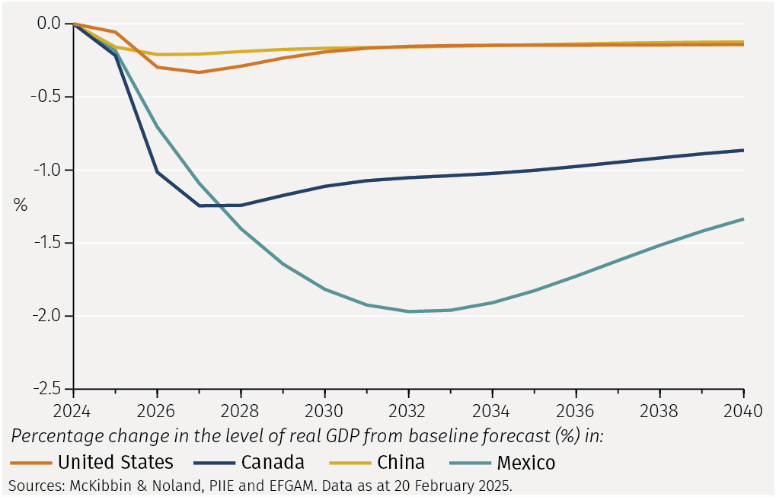

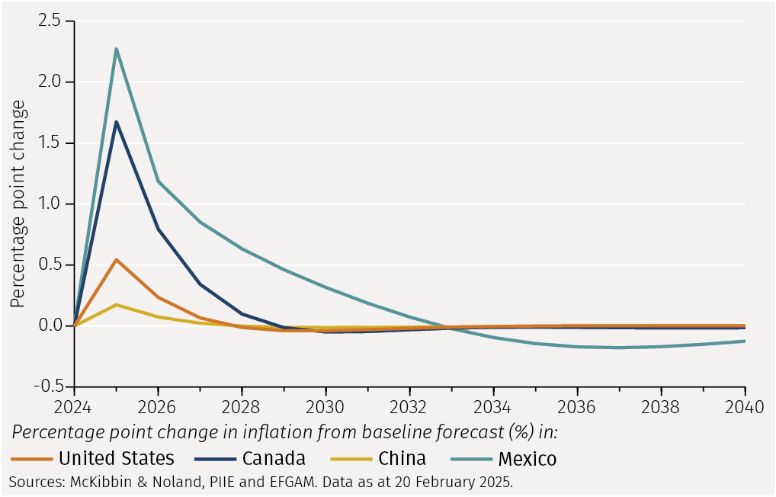

McKibbin and Noland of the Peterson Institute for International Economics (PIIE) estimate that this scenario would reduce Mexico’s GDP by about two percentage points relative to the baseline scenario, causing a long-lasting damage to the economy (see Figure 2).4 Additionally, Mexico’s inflation would increase by over two percentage points over the baseline (see Figure 3).

➡ Scenario 2: US imposes product-specific tariffs on Mexico and Canada, while escalating a trade war with China.

On 11 February an Executive Order by President Trump announced tariffs on steel and aluminum imports from Argentina, Australia, Canada, Mexico, the EU, and UK from 12 March, based on risks to US national security.5

Product-specific tariffs have been common between the US and Mexico in recent years, despite them having a free-trade agreement since 1994. President George W. Bush raised tariffs on select steel products in 2002 and President Trump imposed tariffs on steel and aluminum imports in 2018. In the latter case, Mexico’s retaliation focused on imposing tariffs on food imports from the US.6

This could be a route President Sheinbaum could follow if the tariff threats materialise in 2025, given the negative impact these could have in specific US industries and particularly in rural states which have been strong supporters of Trump. Although food imports from the US represent just over 1% of Mexico’s imports, Mexico represents the largest destination of US pork exports, close to 40% as of 2023.

➡ Scenario 3: Mexico’s actions satisfy Trump’s demands, and no tariffs are imposed.

This would represent the best-case scenario for Mexico, as trade would continue as normal, while governments focus on joint actions to tackle issues such as illegal migration and fighting DTOs. In recent years, Mexico has been one of the countries benefitting the most from US nearshoring efforts, establishing itself as an attractive destination for US industries that require lower manufacturing costs and short transport time into the US. Since 1999, over 44% of Mexico’s foreign direct investment has come from the US.

However, if a country can easily avoid trade tariffs, then their use as a negotiating tool would lose value. So, we would expect the US to follow through with some of them.

Therefore, Scenario 2 appears the most likely. Some trade friction would be expected, without affecting all trade between US and Mexico. That would allow both sides to claim some victory to their electorates.

It is important to remember that the USMCA will be reviewed in 2026. These discussions could also bring forward the negotiations of the new terms of the agreement.

There are still plenty of negative headlines around Mexico and the potential impact from trade tariffs. We believe a deal will be forged to minimise the negative effects on both economies. Both have historically maintained close economic, social, and political links, and it is in their interest to maintain that in the future. Sheinbaum’s government appears to be more pragmatic than some of her predecessors. Therefore, she should negotiate with Trump to continue benefiting from having close links with one of the fastest growing economies.

1 The list includes China, Mexico, Canada, Argentina, Brazil, Colombia, South Korea, Japan, South Africa, the European Union and the United Kingdom, among others.

2 https://tinyurl.com/59s6z3vp

3 https://tinyurl.com/274s6mfh

4 https://tinyurl.com/2s3t24se

5 https://tinyurl.com/2dz4maet

6 https://tinyurl.com/zcs5ayan

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.