- Date:

- Author:

- Daniel Murray and Sam Jochim

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The potential costs and benefits to society of the broad adoption of artificial intelligence (AI) have been widely discussed. Some of the most interesting questions relate to the impact of AI on productivity and GDP growth. In this edition of InFocus, Global Head of Research Daniel Murray and Economist Sam Jochim discuss these issues.

Productivity trends

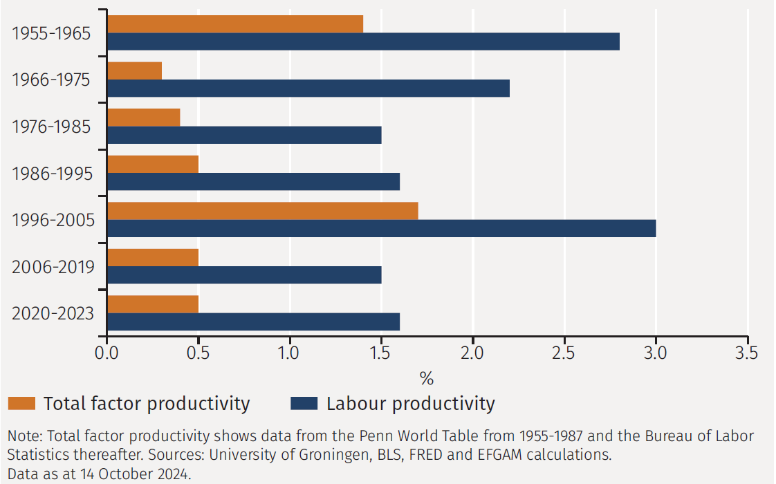

Changes in productivity trends are important because they feed directly through to GDP growth. For any given number of employed people, the volume of output depends on how many hours they work and how much they produce per hour, also known as productivity. The possibility that AI will increase trend productivity growth is therefore worthy of further investigation. It is helpful to start by reviewing how productivity trends have evolved over the past few decades.1 To avoid the potential confusing effects of Covid, the analysis stops in 2019, although we show data for the post-Covid period in Figure 1 for illustration purposes.

Figure 1 shows that labour productivity growth was strong from 1955-1965 before declining in the following two decades and then slowly increasing in the decade thereafter. Productivity then jumped for a decade between 1996 and 2005, but has plummeted since then. Over the period from 1955-2005, annualised GDP growth was 3.4% per annum, with growth in labour force participation and in the working age population offsetting periods in which productivity growth was weaker (see Figure 2).

Slowing productivity growth from 2006-2019 was compounded by declines in the labour force participation rate and the growth rate of the working age population, such that from 2006 to 2019, annualised GDP growth was just 1.9% per annum.2

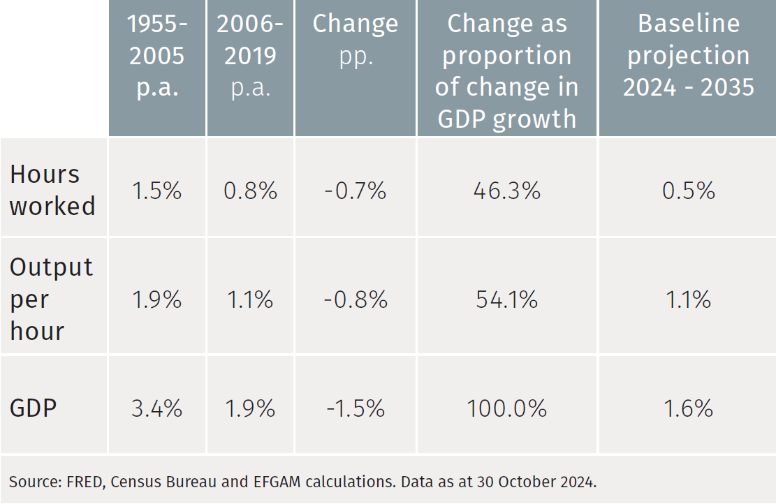

Comparing the 1955-2005 period with 2006-2019, we estimate that over half of the slowdown in GDP growth can be accounted for by a decline in productivity growth (see Figure 3). The remainder of the slowdown in GDP growth was due to a decline in hours worked resulting from falling population growth and a reduction in labour force participation.

Population trends are slow moving, so we can predict with a reasonable degree of accuracy how the demographic profile will evolve over coming years. We assume that from 2024-2035:

➡ (1) Labour productivity growth matches the rate exhibited in the 2006-2019 period.

➡ (2) The participation rate is unchanged from its current level.

➡ (3) Population growth behaves as projected by the US Census Bureau.3

This then produces an estimated annualised GDP growth rate of 1.6% per annum, as shown in the Baseline 2024- 2035 projection in Figure 3. It could be argued that this is a generous estimate as it assumes unchanged productivity and participation, which have both been in declining trends over the past 20 years. Regardless, a growth rate of around 1.6% is weak in a historical context and would have important implications for financial markets: lower growth would likely be a challenge for equity markets but also result in lower government bond yields.

Given that the weak demographic trends are well set and difficult to influence, the main ways in which GDP growth can be augmented are:

➡ An increase in hours worked

➡ An increased in the participation rate

➡ An increase in productivity growth4

In the rest of this report, we focus on the last item and in particular the potential impact of AI on productivity.

Estimates of the impact of AI on productivity

Historically, productivity gains have been driven by the manufacturing sector, to which the application of technology has clear and direct benefits. For example, if the introduction of a machine into the manufacturing process results in a reduction in the number of people required to produce the same output, this has a directly measurable impact on productivity. However, it has been much more difficult to reap and measure productivity gains in services, which are normally more labour intensive. One of the ways in which AI is particularly exciting is because it has the potential to boost productivity in services.

With this in mind, there are many studies discussing the benefits of AI for individual firms. However, there is not yet sufficient data available to ascertain the technology’s impact on productivity at the macroeconomic level.5 Furthermore, the microeconomic studies that are available are likely to suffer from selection error, overestimating the impact of AI due to sampling bias.

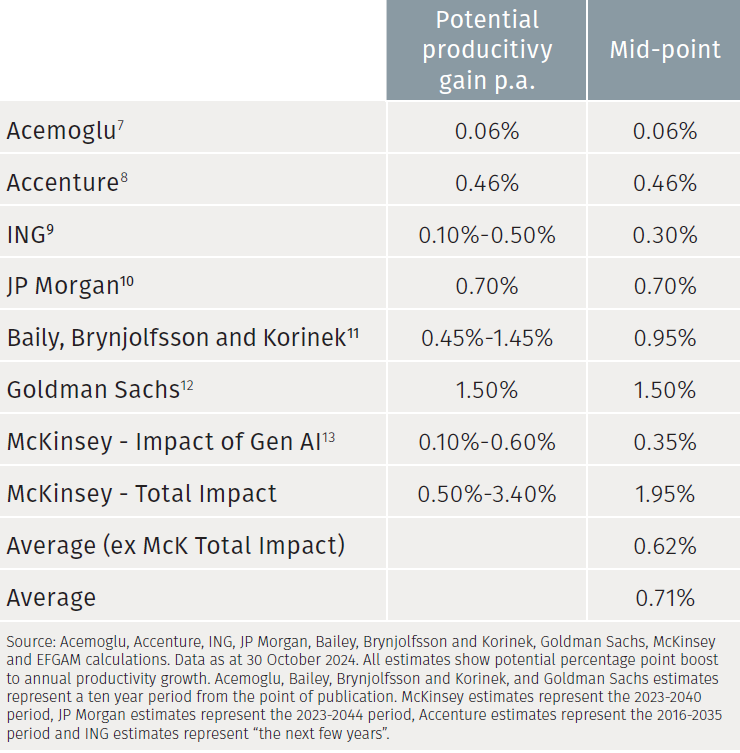

To try to gauge the potential range of reasonable outcomes, we have found it instructive to compile a meta-study of some of the credible macroeconomic estimates that have been made. These are summarised below in Figure 4.6

Note that the McKinsey report includes two estimates of the impact of AI on productivity, one that looks at the full impact of all evolving technologies, the other that looks solely at the impact of Generative AI. The range of estimates in Figure 4 appears wide, although it is skewed by the 3.4 percentage point per annum boost to productivity given by the upper bound of the larger McKinsey estimate. Excluding that outlier produces a much narrower range from around 0.1% at the bottom end to 1.5% at the upper end. The simple average of the range of estimates is about 0.6% to 0.7%.

Applying these estimates to the data in Figure 3 produces forecast annualised GDP growth over the next 10 years of between 1.7% to 3.1% with a central projection of 2.3% (based on the average estimated impact of AI on annualised productivity growth). This central estimate looks reasonable in the context of recent growth trends, suggesting a relatively modest but potentially important uplift to GDP growth over coming years. For example, moving from the Baseline to the Average forecast would result in GDP being about 7% higher in 10 years’ time; moving from the Baseline to the Upper projection sees GDP about 16% higher than in the Baseline. GDP growth would be enhanced further if there is an increase in the labour force participation rate.

Summary

In summary, AI has the potential to offset demographic headwinds to GDP growth by boosting productivity. The possibility that benefits are focused in the services sector is particularly promising and is in contrast with previous productivity enhancing technological advancements. While the potential economic impact of AI on productivity and GDP growth is exciting, the range of possible outcomes is wide and depends on many factors. Although the outcome is currently somewhat intangible, our best guess is that AI is likely to represent an evolution for productivity and GDP growth, rather than a revolution.

1 Productivity could refer to either total factor productivity or labour productivity. Total factor productivity is a measure of an economy’s ability to generate output from inputs but is difficult to measure as it is difficult to ascertain accurate estimates of capital stock. Labour productivity also has the advantage of translating directly thorugh into thinking about GDP growth and so for this note we focus on labour productivity.

2 Gordon, R. (2018), Why Has Economic Growth Slowed When Innovation Appears to be Accelerating? NBER Working Paper No. 24554. Available at https://www. nber.org/system/files/working_papers/w24554/w24554.pdf. Gordon uses 1970 to 2016 as a sample and compares years with similar unemployment rates to account for business cycle effects.

3 The Census Bureau estimates 0.53% annualised growth in the size of the population aged 16+ in the US from 2025 to 2035.

4 Spence, M. (2024) AI’s Promise for the Global Economy. Available at http://tiny.cc/ex9tzz

5 Aghion, P. (2024), The Growth & Employment Effects of AI. Federal Reserve Bank of San Francisco, 8 April 2024. Available at http://tiny.cc/ix9tzz

6 The estimates in Figure 4 generally refer to potential labour productivity gains but those of Acemoglu, Baily, Brynjolfsson and Korinek, and Goldman Sachs refer to potential total factor productivity gains. Labour productivity is a function of total factor productivity and any gains to the latter translate proportionately to the former for a fixed capital to labour ratio

7 Acemoglu, D. (2024), The Simple Macroeconomics of AI. NBER Working Paper No. 32487. Available at http://tiny.cc/qy9tzz

8 http://tiny.cc/ky9tzz Accenture estimate a 35% increase in US productivity relative to the baseline by 2035. Since the report was published in 2016, we take productivity in 2015 as the baseline to calculate the estimated impact of AI on productivity in percentage points.

9 http://tiny.cc/ty9tzz

10 https://tinyurl.com/542dzaeh

11 Baily, Brynjolfsson and Korinek (2023), Machines of mind: The case for an AI-powered productivity boom. Available at http://tiny.cc/xy9tzz

12 http://tiny.cc/zy9tzz

13 http://tiny.cc/1z9tzz

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.