- Date:

- Read time:

- 10 mins

Welcome to the March edition of InView: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

Following a strong start to the year, equity markets lost ground in the second half of February. The MSCI ACWI index posted a negative monthly performance of -0.6%, consistent with normal February seasonality for stock markets.

However, the performance of a diversified portfolio benefited from the bond market rally: the 10-year US Treasury bond yield fell by a bit more than 30 basis points over the month. The gold price marked a new all-time high near USD 3,000 per ounce before consolidating at around that level. While the dollar has lost some ground in recent months, it remains at relatively high levels.

With President Trump’s return to the White House, there has been an avalanche of executive orders, a constant threat of tariffs, and pressure to reduce the public sector workforce. These factors have raised concerns that US economic growth will be negatively impacted, increasing uncertainty and helping explain investors' cautious attitude.

However, there have also been some positive developments. These include the possibility of a ceasefire in Ukraine, the outcome of the German elections, and further supportive measures for the stock market in China. This is reflected in the fact that Europe - including Switzerland - and Hong Kong were the best performing equity markets.

The outlook for European growth has improved somewhat after the German elections. The next coalition government will aim for more growth-friendly fiscal policy and intends to carry out structural reforms necessary for the country to regain competitiveness. A key priority, not only in Germany but across Europe, is to increase defence spending, reflecting the likelihood that Trump will reduce US support for European defence in coming years.

In this context of elevated uncertainty, we believe the asset allocation of a diversified portfolio should remain close to the strategic benchmark. Our equity market preference continues to be for Europe and emerging Asia, while among fixed income securities we believe that high-quality corporate bonds strike the best balance between yield-seeking and risk control

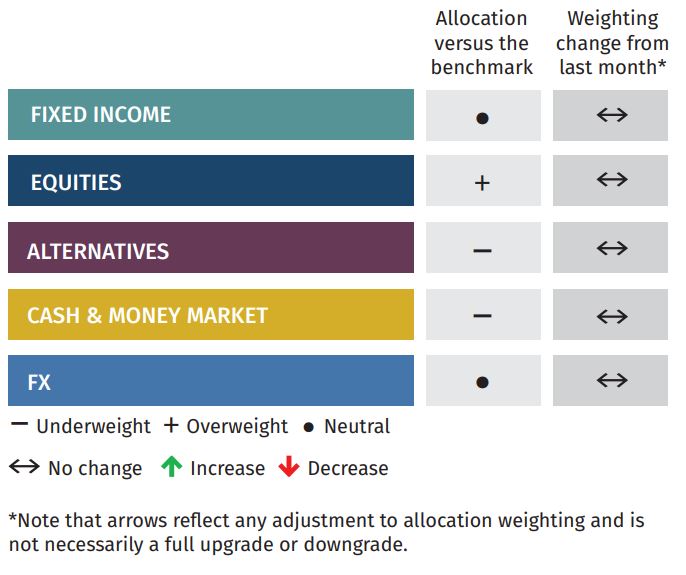

Asset Allocation

Global Allocation

After reducing our equity allocation last month, we are maintaining a very modest overweight position. Caution persists due to ongoing geopolitical tensions and signs of an escalating trade war. While no changes are being made to our fixed income allocation, we are closely monitoring movements in the US Treasury market. Recently, there has been a rally in 10-year Treasuries, with the potential for yields to fall further in the short term. If this trend continues, there may be a case for reducing our fixed income allocation to an underweight position. Should that occur, the allocation would likely shift to alternatives or cash, both of which are currently underweight.

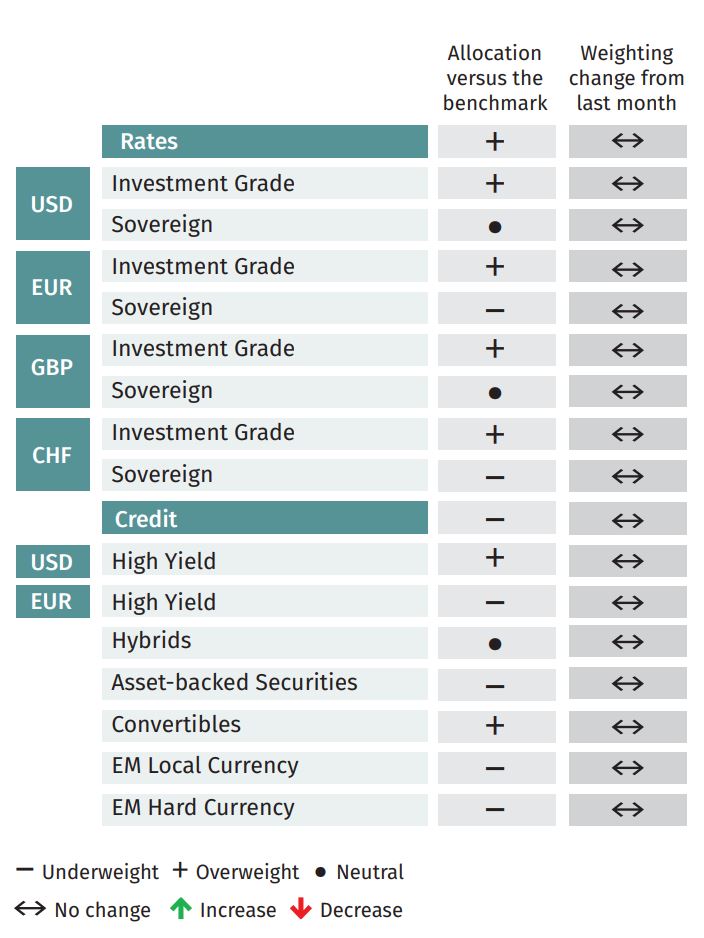

Fixed Income

No changes are being made to our fixed income allocation this month. Convertible bonds have had a positive start to 2025 and we are happy to maintain our overweight position. We note that macro factors for sovereign bonds are less favourable than before given the recent rally, although this does not warrant a change in positioning. Last month sovereign bond exposure was reduced, with EUR and CHF underweight and US sovereigns at neutral, accommodating the additional high-yield exposure. Technical factors for investment-grade bonds have improved and we remain overweight across currencies. The average duration is being held at 3.5 years, slightly below the benchmark.

Equities

US exposure was rebalanced to account for market drift but maintaining the same degree of underweight. We have downgraded our assessment of the US macro environment due to mixed economic data, although risk factors have moved to neutral. Macro risks in Europe have decreased following the results of the German election and the European Central Bank's continued rate cuts. However, we would like to see a pick-up in Purchasing Managers’ Indexes before becoming more confident about the economic outlook there. After taking some profits last month, we continue to hold a modest overweight to Europe. Within Asia, given the change in China's weighting in the benchmark, we increased our China exposure to maintain a slight overweight. Meanwhile, we reduced our India exposure to neutral, staying cautious for the time being. A Trump trade deal may serve as a catalyst for better performance if it were to materialise.

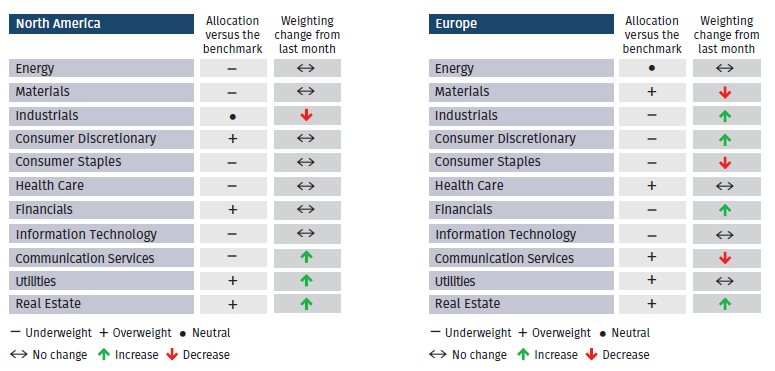

Equity Sectors

Equity Sector Views

UK

Following the outcome of the US election and an increasingly resilient macro recovery outlook, we raised our exposure to internationally focused UK industrial names.

We continue to see an opportunity for the outperformance of UK midcaps over the coming quarters, reversing a multi-year period of underperformance through high inflation and interest rates, as both of these factors normalise. Information technology has been a sector in which we have found specialist UK companies trading on attractive valuations in our view backed by strong structural growth tailwinds.

This year, we have also increased our weighting towards consumer discretionary, given our more constructive outlook for improving real incomes. Our exposure is balanced between internationally focused Hotel & Leisure businesses, as well as domestic UK recovery geared names, such as housebuilders, which will be supported by both falling rates and the new Labour government which aims to reform the planning permission system to boost economic growth.

US

With Trump’s tariffs creating uncertainty, we are reducing our overweight industrials position to neutral. This adjustment will also reduce our cyclical exposure in case the US economy slows more than expected. In response, we are adding to our communication services position due to positive earnings, although it remains an underweight. Additionally, we have increased our allocations to utilities and real estate, both to overweight positions, as they could benefit from lower interest rates.

Europe

A full review of European sector allocations was conducted, prompting several changes. Having previously added to financials, primarily European banks, we are further increasing this allocation, although it remains slightly underweight. Industrials and consumer discretionary were also increased, but remain underweight, while the overweight position in real estate has been further increased. To balance this out, we reduced our overweights in materials and communication services, while consumer staples have been downgraded to underweight.

Alternatives

No changes are being made to our alternatives allocation, with hedge funds accounting for the largest share, in line with the neutral benchmark. We expect hedge funds could be poised to exploit more opportunities in a Trump regime. Meanwhile, in our view Trump may be bearish for oil prices but could be more favourable for broader industrial and soft commodities. Our insurance positioning remains overweight versus the benchmark, with our exposure serving as a valuable portfolio component given its uncorrelated nature.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.