- Date:

- Read time:

- 3 minutes

- Author:

- Camila Astaburuaga

Senior Portfolio Manager

Netflix tested if love is blind by stripping away appearances and focusing only on personality and values…some might call them “core fundamentals”. The TV show has been successful in demonstrating that love is indeed blind; theoretically the same should apply to how debt is priced, but is it?

Too often, investors give the largest, most “developed” or simply familiar countries the benefit of the doubt. Such a superficial approach, focusing on shiny labels or benchmark weights can lead to countries trading at similar levels, even when their fundamentals tell a very different story. In fixed income, where the goal is to avoid defaults and downgrades, such a bias is dangerous.

The reality today

• Global public debt hit a record $102 trillion in 2024, up 60% in a decade.

• Debt service is eating up government revenues.

• Nearly double the number of countries now run unsustainable deficits compared to two years ago.

• Many of the riskiest balance sheets belong to “safe” developed markets.

Excessive debt has real consequences. Global sovereign debt is reaching unsustainable levels, and the risks are rising quickly. Governments worldwide have issued record amounts of debt at historically low interest rates. Now, as those bonds roll over in a “higher for longer” world, many nations face mounting refinancing costs, potential distress, and spread widening across fixed income markets.

The IMF considers debt levels above 60% of GDP unsustainable for most countries. Alarmingly, the share of global GDP of the economies in this category has surged from 28% to 80% in just 2 years, as shown in Figure 2. Sovereign stress is not just a government issue - when a country runs into fiscal trouble, its corporates suffer as well.

Fundamentals matter more than labels

Markets often remain biased toward “developed market” reputations and benchmark weights, overlooking deteriorating fundamentals. Yet indicators such as debt affordability, leverage, reserves, and net foreign assets tell the real story -a story of sharp divergence. History has repeatedly shown that bonds from countries with stronger fundamentals tend to outperform in times of stress, while those from weaker sovereigns see yields spike and their credit ratings tumble.

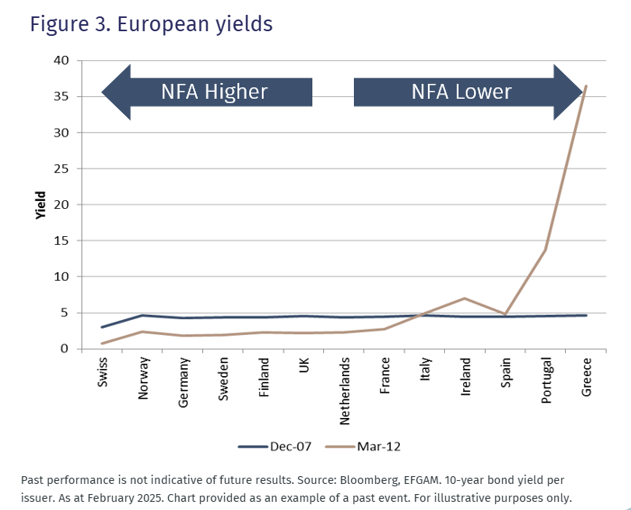

Investors heavily rely on rating agencies to accurately assess risks, but history reveals how precarious the analysis has been and how those entities can also be influenced by labels too. Europe is a good example of this situation: pre-2008, nations were rated AAA and trading at essentially the same yields. However after a period of easy borrowing, weak fundamentals meant that some countries eventually saw sharp underperformance. Those countries had been showing worse fundamentals for a long period of time, so why were rating agencies not incorporating this into their rating? Why were investors not asking for extra compensation from those countries?

A key piece of data alongside leverage, interest cost burden and reserves is Net Foreign Assets, which we believe is key to understanding the true flexibility and capacity-to-pay of countries. When comparing this metric for the different European countries, it is clear that not all the bonds should have been trading at the same level. Investors were biased towards the “developed market” label and the shiny AAA rating, whilst ignoring or being unaware that, underneath, there was true weakness coming across. This not only impacted sovereign ratings and yields, but corporates and banks of those nations.

The biases are not limited to developed markets. A recent comparison of Peru and Turkey illustrates the point. Despite starkly different fundamentals - from inflation to debt affordability - their 5-year USD bonds traded at just a 22bp spread differential in late 2024. How much extra compensation should investors demand from Turkey to reflect its the inferior fundamentals? Stress testing is key to understanding potential outcomes. In this case, the upside was similar, but the downside for Turkey was far greater. So far this year, Peru’s total returns have nearly doubled those of Turkey, proving again that fundamentals tend to come out on top when uncertainty increases.

The lesson

As refinancing pressures mount globally, investor biases risk leaving portfolios overexposed to vulnerable sovereigns that aren’t priced for their risks. This is the moment to seek differentiated strategies that focus on true creditworthiness and to not be seduced by archaic labels, ratings, or benchmark weightings.

Love may be blind but bond markets are not as blind as they should be – and this is as true today as it was in the past. Markets get complacent in good times, but when stress hits, either at a global or a local level, fundamentals reassert themselves and investors who ignored them pay the price. Higher yields don’t always mean higher returns. So in the current market environment, where spreads are tight, and risk premia is limited, focusing on fundamentals is key in our view.

Debt isn’t blind. Many investors still are. That’s our opportunity.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested. This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document. Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group. This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.