Our top 10 themes for the year ahead

Inflation trends and the pace of economic growth will be key factors shaping markets in 2024. The global economy appears to be on course for a soft landing next year, with growth rates in emerging and developing economies set to overtake most advanced economies.

World economy has a soft landing

Our most likely scenario is for a soft landing for the world economy in 2024 with global growth around 2.5%-3%.

We think the US will avoid a marked recession and grow faster than most other advanced economies, as it did in 2023. Emerging and developing economies should outpace advanced economies, although China will settle into a pattern of slower growth (around 4.0% to 4.5%). The pattern of growth between different sectors will continue to shift. Spending on physical goods (working from home equipment, for example), which soared in the pandemic, gave way to greater spending on services (leisure, transport and entertainment) as economies re-opened. A shift back towards goods production (notably in the electronics industry, helped by the rapid development of AI) will be a feature of 2024. A soft landing is by no means certain, however. There is a risk that prior aggressive increases in interest rates will cause a larger hit to economic growth and inflation than we expect in our baseline scenario. There is a smaller probability of a more benign alternative: that growth carries on with little turbulence. That could be supported by our second main theme: productivity gains.

Productivity gains

Economist Robert Solow famously said in 1987 that the computer age was everywhere except for the productivity statistics. It may finally have arrived.

US productivity (output per hour in the non-farm business sector) grew at a rate of just 1.2% p.a. in the ten-years prepandemic. Its surge to an annualised rate of 5.2% in the third quarter of 2023 rekindled hopes of a technology-driven productivity renaissance. That, however, exaggerates the potential improvement. McKinsey estimates generative AI could boost labour productivity by 0.1% to 0.6% p.a. up to 2040.1 That suggests a modest improvement, to around 1.5% p.a., is feasible. With continued population growth, the US would then be set to maintain GDP growth of around 2% p.a.

The effects of generative AI in improving productivity are already seen in certain sectors. Its use in the consulting sector has been widely reported. Legal services, the creative industries and (after some hesitation) the education sector are also likely to benefit from it. AI cannot replace all jobs, of course, despite some claims to the contrary, although it represents an exciting prospect that has the potential to bring about meaningful change.2

Fiscal fragility

Governments around the world are burdened with high budget deficits and debt levels. It is especially problematic in the US where there is a structural imbalance between revenues and spending.

US fiscal conservatives stress the need to cut government spending or raise taxes. To be sure, they are the only credible solutions. But reversing the tax cuts of recent years (technically, allowing them to expire on 31 December 2025) will be politically difficult. There are also multiple pressures on government spending: the (well-known for years) upward trend in health and social security spending in an ageing population are compounded by upward pressure on defence and infrastructure spending and, now, higher interest payments on government debt.

‘Inflating away the debt’ is sometimes suggested as a way out of the problem. That is, tolerating a higher level of inflation which would reduce the real value of outstanding debt while raising nominal GDP. However, that would provide only temporary relief as higher inflation would elicit Federal Reserve tightening and higher rates in the future. Another option - default - must surely be unconscionable.

The bond market vigilantes will continue to put pressure on governments running irresponsible fiscal positions in 2024. It would be naïve to think the US could be immune from such pressures. Notably, the appetite for US bonds from foreign investors cannot be relied on. Expect fiscal fragility and the bond market's nervousness about it to remain a theme. Increased concern about the risk of holding longer-maturity bonds is a structural argument for an upwardsloping yield curve.

Political turbulence

More than half of the world’s population live in countries in which there will be national elections in 2024. The US elections – with the possibility of Mr Trump’s return to the White House – will attract the most attention and are potentially the most consequential.

More than 4 billion people live in the 76 countries that will hold national elections in 2024.3 The extent to which these are truly democratic and can be expected to lead to change varies. Vladimir Putin is almost certain to be re-elected for a third consecutive term and ‘strong men’ will remain in charge elsewhere. Bucking that trend, Mexico will likely elect a woman as president. In India’s elections, expected in April-May, Narendra Modi’s BJP party is widely expected to be re-elected. In the UK, the governing Conservative Party faces a stiff challenge from the opposition Labour Party. Elections to the European parliament are held in the 27 member states. But it is America’s presidential election that will be the most significant. Donald Trump has pledged an end to the Russia-Ukraine war “in 24 hours” if he returns to the White House. An easier regulatory environment for big tech and banking and the maintenance of low corporate and personal taxes are also likely on his agenda. A big increase in customs duties (to 10% on all imports) is also proposed: it might be politically popular but it would do little to help reduce the US budget deficit.

2023 was the third year of the presidential election cycle in the US. Such third years have seen an average drawdown (from peak to trough) in the S&P 500 index of 11.7%.4 The two drawdowns in 2023 were 7.8% (2 February to 3 March) and 10.3% (31 July to 27 October). The recovery from 27 October is currently 10.6%. The pattern seems to align quite well with previous third year experience. Looking ahead to 2024, previous fourth year experience is for a larger drawdown (13.7%) but a larger recovery (23.9%) than in third years. In short, higher volatility but with potentially larger upside.

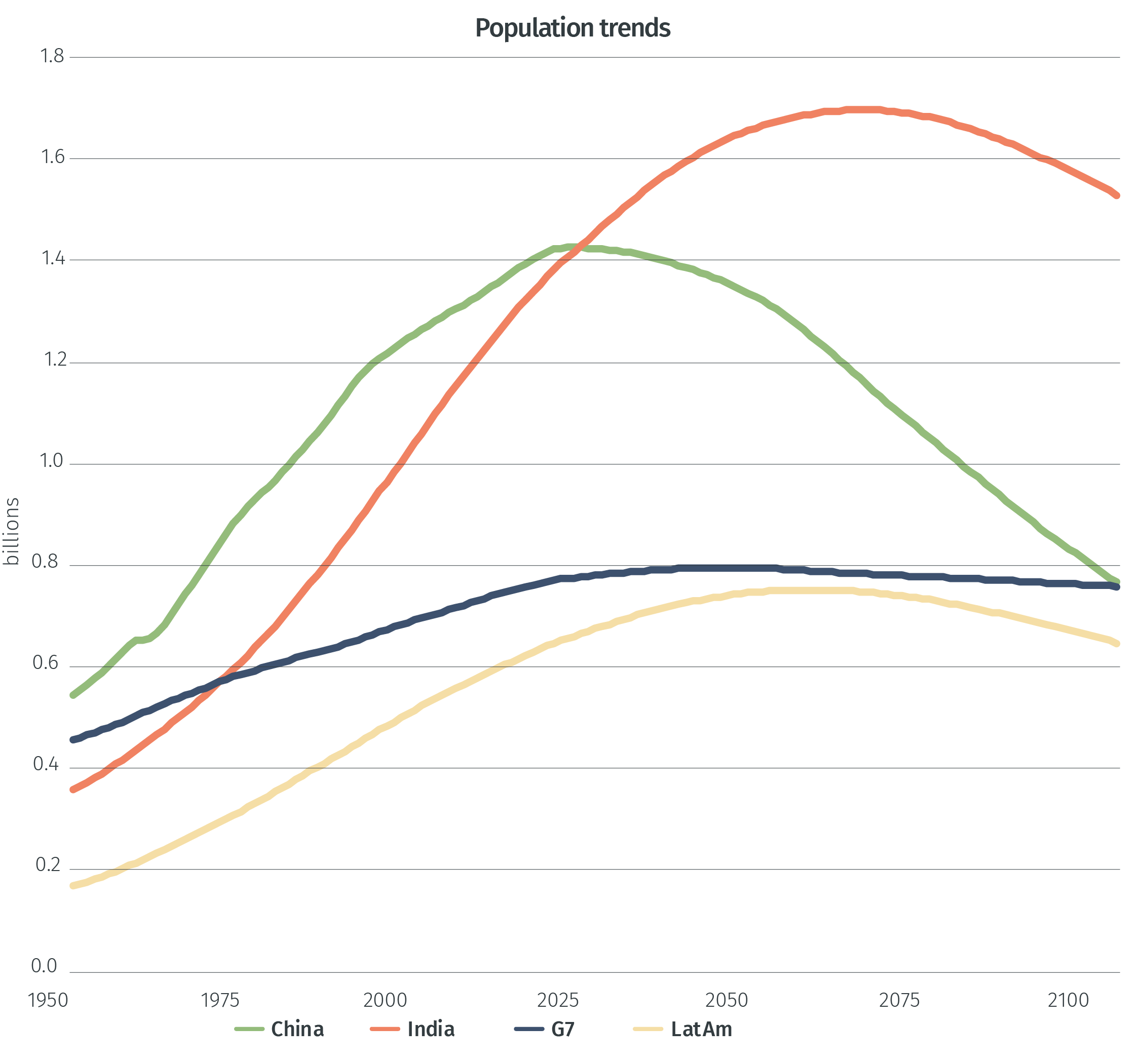

Demography is (still) destiny

It has often been said that demographics is destiny: for any economy, the size of its population, its age distribution and how many people are working are key drivers of economic progress.

Japan has seen adverse demographics undermine its growth for several decades. China is entering a similar phase. Between now and 2100, China’s population will shrink by 650m, according to UN population projections. It will lose as many people as the current population of Latin America.

The speed of the decline in China’s population in the next two decades will be similar to that seen in Japan from its peak but will then accelerate.

Countries can adapt to the challenges of a shrinking population. Participation rates (the proportion of the population working or seeking work) can increase through later retirement and a higher female participation rate, for example. Both have been seen in Japan. Measures to improve productivity can be encouraged. South Korea’s population is expected to decline markedly in the coming decades, given the extremely low fertility rate, but it has had one of the strongest increases in productivity in recent years: maintaining this will be important.

China faces the additional challenge posed by its greater recent emphasis on domestically-orientated growth. Japan and Korea have seen their economies prosper in the face of demographic challenges as a result of remaining open to international trade. China risks forgoing those gains.

In countries where populations are projected to expand rapidly, the same issues apply in reverse. Finding enough jobs for the rapidly growing young populations of Africa is an enormous challenge.

Demographics is destiny: but how different economies rise to the challenges it poses will be a key theme of 20245.

Weight loss and consumer staples

The popularity of weight loss drugs will, we think, surge in 2024. The potential market is huge. But the impact on the consumer staples sector has been exaggerated.

More than two thirds of adults in the UK and US are obese or overweight. The potential for the use of weight loss drugs is huge. The growth of the market and its influence could well be 2024’s parallel to 2023’s AI theme: an innovation that rapidly becomes adopted. Effective use of weight loss drugs can have far-reaching consequences: directly because of reduced demand for food; indirectly, due to potentially less pressure on healthcare systems. The big question is whether such drugs turn out to be just a variant of the many diets that have promised, but failed to deliver, weight loss in the past.

The potential effect of weight loss drugs in reducing food demand was a contributory factor to the performance of the consumer staples sector in 2023. Additionally, sales growth slowed for consumer staples companies (largely because of lower inflation); and higher long-term interest rates adversely affected the valuations of what is a traditionally defensive sector.

The global consumer staples sector is, as a result, undervalued on the basis of our proprietary assessment. We think valuations adequately reflect the risks involved. This is our main contrarian sectoral investment theme for 2024.

Clean energy transition

The transition from fossil fuels to clean energy remains of utmost importance but progress stalled in 2023. We see it regaining momentum in 2024.

The International Energy Agency's latest projections see investment in clean energy rising from USD1.8 tr in 2023 to over USD4 tr per year in the 2030s. The demise of the ICE (internal combustion engine) age and the rise of electric vehicles is already clearly underway. That will need to be accompanied by clean energy power generation, new supply lines and improved energy efficiency. Yet, 2023 saw a marked setback in some of these projects, including the failure of the UK’s auction of the next generation of offshore wind generation rights. 2024 will see, we think, such projects get back on track. Wind, solar and battery storage projects were adversely affected by higher financing costs as interest rates rose in 2023 and, in some cases, the setting of unrealistically low future price guarantees. We see a much more positive outlook for 2024. Valuations of companies in those sectors price in little prospect of future growth, which seems highly unrealistic. Globally, there is a strong policy incentive to meet renewable energy capacity additions. Moreover, financing of this seems readily available, not least because of the number of investors increasing their allocations to ESG investment in general and decarbonisation technologies in particular.

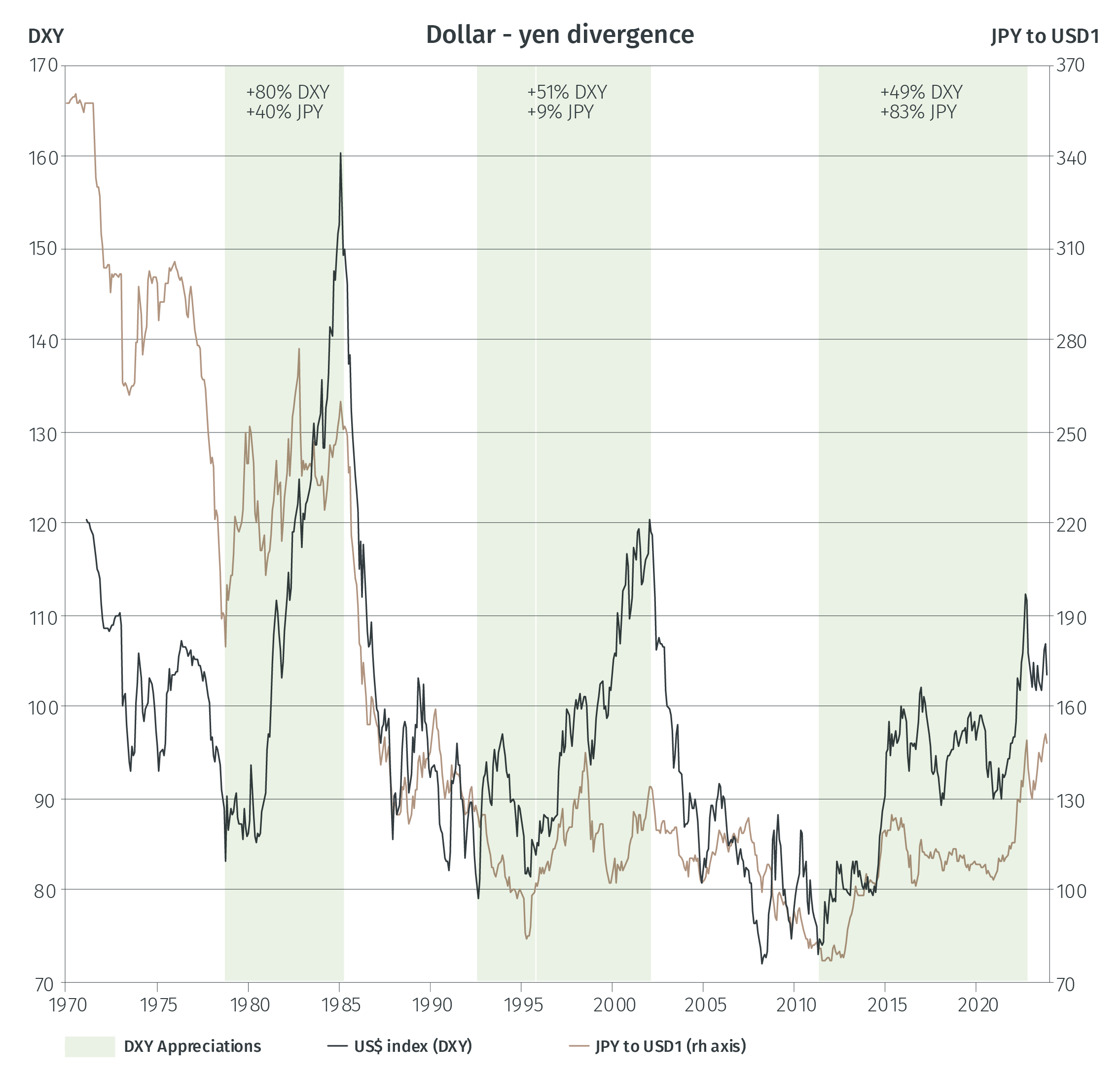

Undervalued currencies recover

The long upward trend in the US dollar’s valuation on its nominal and real exchange rate indices came to an end, we think in late 2022.

We expected a downward trend starting from then, which has occurred. But the pattern of dollar weakness has been uneven against different currencies. Indeed, the dollar has remained strong against the yen.

The result is that the Japanese yen appears to be undervalued on almost all measures of purchasing power parity and equilibrium exchange rates. 2024 will be a year when that undervaluation of the yen is, we think, corrected. The move away from Japan’s zero interest rate policy, a continued recovery in the Japanese economy and renaissance in Japan’s corporate sector will drive the appreciation.

Undervalued currencies recover

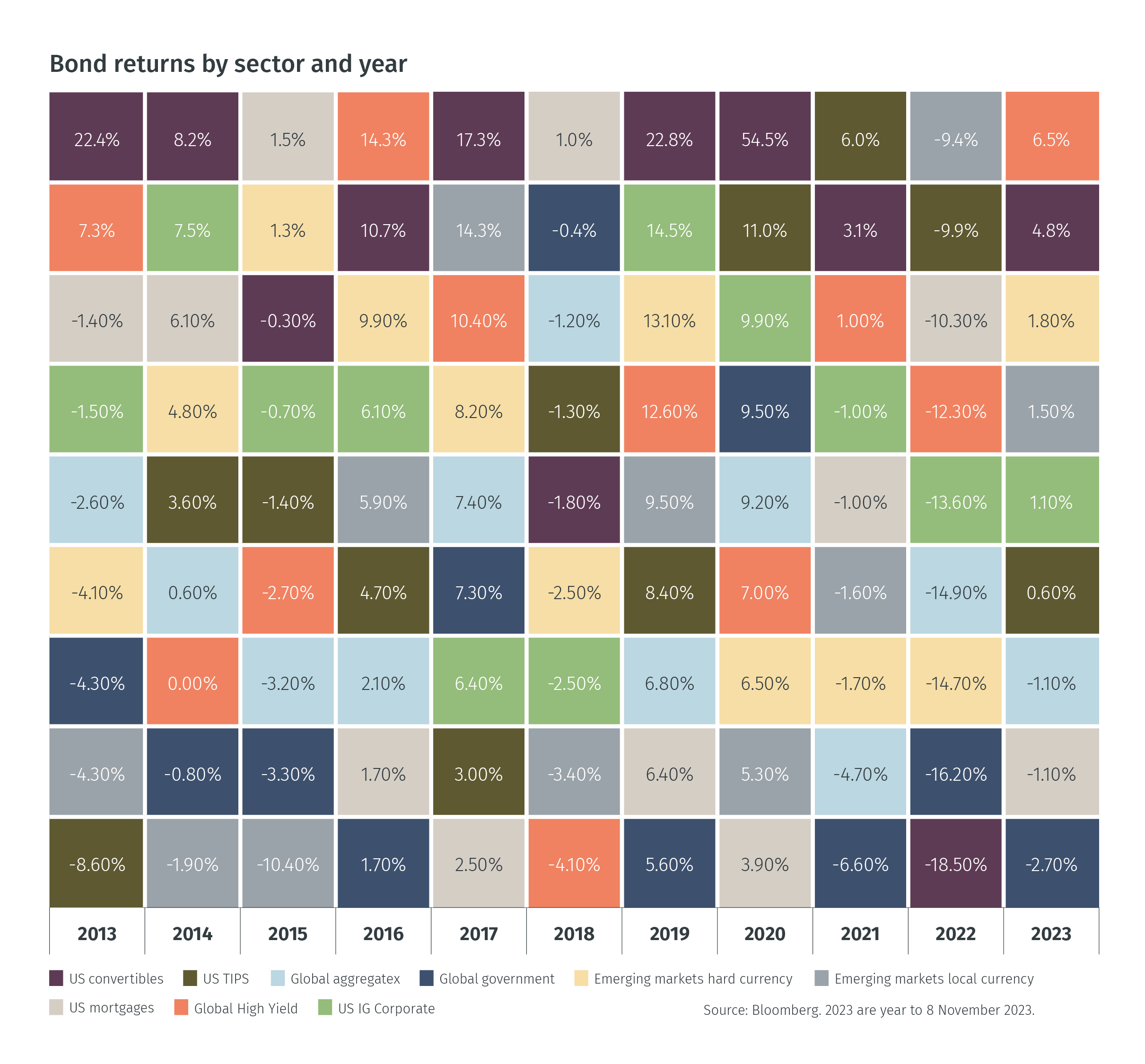

Bond opportunities

We see three interesting opportunities in bond markets for 2024.

First, shorter-dated maturities have historically offered protection against the reinvestment risk associated with declining short-term interest rates. We favour three to five year maturities in government and investment grade corporate debt. Second, inflation-linked bonds appear attractive because of the high real yield which they now offer and the fact that they do not already price in too high an inflation outlook. They have historically offered a good opportunity for bond investors while also providing protection from an inflation surprise. Third, selected convertible bonds provide the security associated with fixed income exposure and the upside potential from (especially small cap) equities.

Bond opportunities

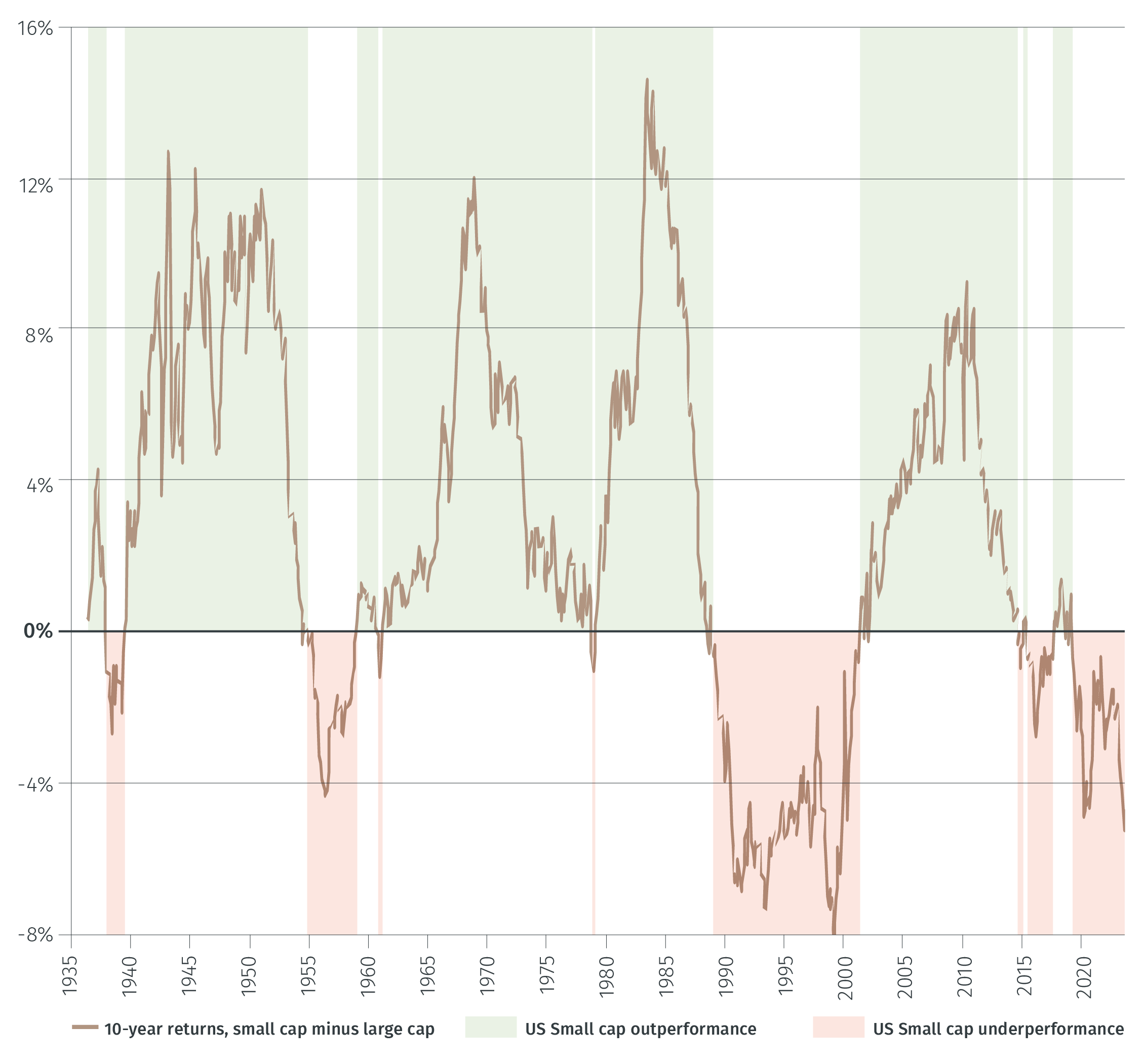

Favour small cap stocks

A favouring of small cap stocks, one of our themes for 2023, did not work out too well, but we maintain that theme for 2024.

The small cap sector is a broad universe and active sector where stock selection is important. In 2023, for example, the US small cap bank sector was particularly weak; and small cap ‘zombie companies’ – those with insufficient earnings to cover interest expenses – were a drag on the overall market.

Small cap stocks have historically produce higher returns than large cap stocks over time: the so-called small cap effect.

69% of the calender months since the 1930s small caps have produced higher returns.

Small cap stocks’ share of overall US market capitalisation has fallen to just under 2%, from a peak of over 9% in the 1980s. One of the main reasons is that the trend towards passive investing has tended to favour large cap stocks, while small cap stocks have less representation in widely-tracked passive indices.

An alternative to outright small cap selection is to favour an equally-weighted broader index which gives less weight to the very large cap tech stocks (which drove the US equity market appreciation in 2023) and more weight to smaller cap stocks.

Source: Kenneth French database and EFGAM calculations. Period over which returns are assessed: August 1926 to September 2023.

Past performance is not indicative of future results.

Review of outlook 2023

How did we do in 2023?

We expected that inflation rates would, finally, fall in the main advanced economies, with the US rate dropping to close to 3% by year-end. Inflation rates have declined broadly as we expected, with the latest readings showing US, eurozone, UK and Japanese CPI inflation at 3.1%,2.4%,4.6% and 3.3%, respectively. We expected inflation rates in emerging economies to be much less of a concern. That was the case. Notably, China re-entered deflation, with the CPI falling 0.5% year-on-year in November.

We expected geopolitical tensions to ease. They did, up until 7 October, but then spiked higher after the Hamas attack on Israel and the Israel-Gaza war. The Russia-Ukraine war continued but did not escalate. Elsewhere, however, there was an easing of tensions. Chinese relations with the west improved, with a series of bilateral meetings between China and the US, Australia and the EU. Under India’s G20 presidency a joint communique was agreed and the African Union was welcomed as a G20 member. The BRICS group also widened its membership to include five more economies.

We expected 2023 to be a year of more normal GDP growth rates. That proved to be the case. For many, the main economic surprise of 2023 was that there was no US recession. In late 2022, the chance of that was put at 70%.6 The outturn was quite different: no recession and growth of over 2%.7 We were more optimistic than the consensus, thinking that a recession, if it did occur, would be mild and only start late in the year. In the UK and the eurozone (notably Germany), we thought a recession was almost inevitable: zero growth or a mild recession seems to have been the outturn.

We expected the Japanese renaissance (defined, in particular, as a revival of corporate earnings) to continue. That proved to be the case. Corporate earnings rose by 8%, faster than nominal GDP (5% growth). The Japanese equity market, reflecting this trend, produced the highest local currency returns of the major developed markets. In US dollar terms, however, these were undermined by continued weakness of the yen.

We expected that, after years in which they had underperformed developed markets, 2023 would be a much better year for emerging markets. That was the case in bond markets (hard currency emerging market bonds produced higher returns than developed market bonds); but emerging market equities underperformed. Although China’s economic growth was weaker than many expected, growth in India and Brazil was stronger than consensus expectations at the start of the year.

We thought the US dollar had likely peaked (at overvalued levels) on both its nominal and real exchange rate indices in late 2022. Given that, and the prospective evolution of monetary policy and current account balances, we saw a weakening trend in 2023. That happened in the first half of 2023, but by early-December the dollar’s DXY index was broadly unchanged from its end-2022 level. The pattern against a range of major currencies is interesting. The dollar strengthened against the Japanese yen, Australian dollar and Chinese renminbi; but weakened against the euro, pound sterling, Swiss franc and the Brazilian real.

We expected the ‘bond vigilantes’ to be on the lookout for any country where there were concerns about inflation and excessive fiscal and monetary stimulus. That followed the vigilantes’ surprise reappearance in 2022, when the UK gilt market was hit hard in response to an unfunded, poorly-explained fiscal stimulus. The vigilantes were, indeed, out in force in 2023. 30-year yields were driven above 5% in the US and UK. Benchmark US 10-year yields touched 5% in the US. And, under pressure from financial markets, the Bank of Japan finally eased its ceiling on 10-year yields in November, allowing a rise towards 1%.

We saw investment grade corporate bonds, notably in the US and UK, offering a better return/risk profile than either government bonds or high yield debt in 2023. They did provide higher returns than government bonds. But high yield bonds were the top-performing sector in the year. Stronger-thanexpected US economic growth favoured such bonds, as did the fact that they have a lower sensitivity to rising government bond yields. The shrinking of the high yield universe (as several large companies rose to become investment grade and there was very limited high yield issuance) also helped.

We saw good opportunities in the global small cap sector. We cited three factors favouring small over large cap stocks: they are typically quicker to adapt to changing economic circumstances; they were attractively valued relative to large caps in late 2022; and they tend to outperform large cap stocks over the long-term. Additionally, we expected a move back towards active from passive investment strategies, which would tend to favour small cap stocks. At the global level, that strategy did not work out well although there were regional variations: small cap Asian stocks did well.

Our contrarian sector view was to favour consumer discretionary stocks. There were three main reasons: we expected consumers to be prepared to run down further the savings accumulated during the pandemic; we thought that wage growth would remain resilient; and with high mortgage costs inhibiting home moving, we expected more spending on home improvements. Broadly, those factors did play out. Total returns from that sector were over 20%, well ahead of the returns from the MSCI World index.